The Inflation Solution to the Housing Mess

John Makin,

Wall Street Journal April 14, 2008

News Home

Home - Index - News - Krisen 1992 - EMU - Economics - Cataclysm - Wall Street Bubbles - US Dollar - Houseprices

Many pundits suggest the decline in savings is a non-issue, while others, more on the extreme, believe that it

one of the primary economic issues currently facing the United States.

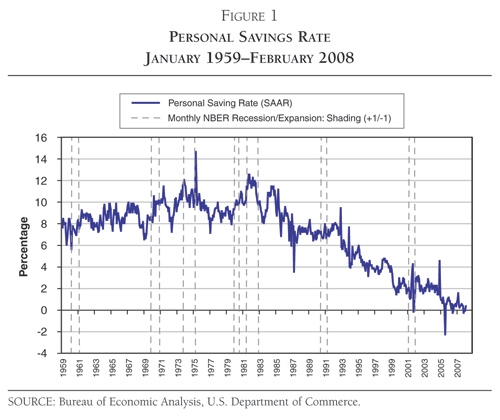

In the 1970s and 1980s savings were in the 5 - 7% range.

In the decades since, personal savings have declined to the 1 - 3% range.

CNN June 30, 2010

The measured savings rate out of disposable income fell to 2 percent

from its long-run average of 8 percent.

Just 2 percent of U.S. disposable income is $200 billion.

John H. Makin, April 30, 2008

That unusually rapid pace of wealth accumulation was accompanied by a substantial drop in savings rates by American households as well as by rapid innovation in American financial markets (see figure 1). From 1990 to 2000--the period of most rapid American wealth accumulation--the measured savings rate out of disposable income fell to 2 percent from its long-run average of 8 percent.

Between late 2000 and late 2002, the broad stock market, measured by the S&P 500 Index, fell by nearly 50 percent. Still, the savings rate remained low and subsequently fell to zero after 2004 as the housing boom took hold.

It may be that the search for an alternative vehicle for wealth accumulation, coupled with the remarkably easy credit conditions that emerged in the wake of the stock market crash, pushed American households into investments in housing as an alternative vehicle of wealth accumulation.

There was plenty of help from the American tax code, which favors housing with full deductibility of interest on mortgages and favorable tax treatment of capital gains on residential real estate.

Beyond that, the innovative mortgage sector had, by 2003, begun to expand radically the amount of leverage available for households wishing to purchase real estate.

Even a modest effort by U.S. households to increase savings could cut U.S. growth substantially.

Just 2 percent of U.S. disposable income is $200 billion.

If U.S. households attempt to boost the savings rate from the current zero level to 2 percent, the drag on GDP would be about 1.5 percentage points.

The day that American consumers stop spending and start saving again could bring serious problems for US growth.

Gerard Baker December 14 1998

Gerard Baker is United States Editor and an Assistant Editor of The Times. He joined in 2004 from the Financial Times, where he had spent over ten years as Tokyo correspondent and Washington Bureau Chief. His weekly oped column appears on Fridays

http://www.timesonline.co.uk/tol/comment/columnists/gerard_baker/