Rolf Englund

2001-02-04

P.M.

Realräntepapper

Peter Norman, VD för Sjunde AP- fonden

DN Debatt

2000-10-28

Den produkt som ligger närmast till för pensionssparande är realränteobligationer. En obligation som ger en garanterad avkastning utöver inflationen. För närvarande är räntan 3,5 procent plus den nuvarande inflationen på 1,5 procent. En totalavkastning på nominellt fem procent som kan uppnås med säkerhet. Ett realt sparande borde erbjudas alla pensionssparare och vara bottenplattan i varje portfölj som syftar till ett långsiktigt sparande.

Thomas Franzén, chef för Riksgäldskontoret, varnar

för att inflation och valutakursförändringar riskerar att

tära på avkastningen i de drygt 450 privata fonderna.

DI

2000-10-06

"Det allvarligaste är att man inte tar upp inflationsrisker och inflationsproblematik i ett så långsiktigt sparande som pensionssparandet är".

Historiskt har inflationen varit den vanlige spararens stora fiende, skriver han i Post- och Inrikes tidningar. "Ingen vet vad inflationen blir. Det finns en poäng att gardera sig mot den", säger Thomas Franzén.

Ett sätt att göra det är att investera i realränteobligationer, ett instrument som Riksgälden själv saluför. Det tillgångsslaget placerar bara två PPM-fonder i: Statens Premievalsfond och Premiesparfond. De går under namnet Sjunde AP-fonden.

Ett annat problem med de privata PPM-fonderna är enligt Riksgäldschefen att få, om ens några, valutasäkrar sina placeringar. Valutakursförändringar tär ibland allvarigt på fondavkastningen. Det har de till exempel gjort under det senaste året i Europafonder.

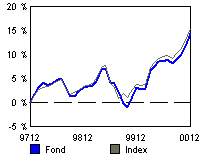

Skandias Realräntefond

Gå till https://secure.skandia.se/cgi-bin/g5/linkfond/kurser_aktuella

Klicka på ”realränte” långt ner på sidan

Aktuella räntor för RiksgäldsSpar

http://www.rgk.se/scripts/cgiip.exe/rgk/pub/showDoc?DocId=75

Riksgäldskontoret

Senaste realränteemissionerna

http://www.rgk.se/scripts/cgiip.exe/rgk/emission/listinflationbonds?Year=2001

JAMES GRANT, Financial Times; Oct 30, 2000

The writer is

chairman of Grantsinvestor.com

The market expects no untoward events - its implied long-term inflation forecast is pure sunshine. Over the next seven to 10 years, it can be inferred, the CPI will rise by an average of no more than 1.8 per cent a year - never mind that over the past 12 months it has climbed by 3.5 per cent.

(This is the forecast embedded in the respective prices of inflation-indexed and non-indexed government bonds; at an annual average rise in the CPI of 1.8 per cent, indexed and non-indexed securities would perform identically.)

Bonds do not go up like stocks but they do crash like them.

Are Real Interest Rates Too High?

William Poole

President, Federal Reserve Bank of St. Louis

Money Marketeers of New

York University New York City September 21, 1999

Viewed historically, nominal interest rates in the United States are high today compared with the trend rate of inflation—in other words, the real rate of interest is high. For example, the interest rate on 1-year U.S. Treasury securities is currently roughly 5 percent. If we take the recent inflation trend of around 2 percent to be a good indicator of the outlook for future inflation, then the real rate on 1-year T-bills is about 3 percent. This real rate compares with an average inflation-adjusted return on 1-year T-bills of less than 2 percent over the past 50 years. Similarly, the real yield on long Treasuries is about 4 percent today, which is about 1 percentage point higher than typical for the U.S. economy.

How Real Is the Real Rate?

In some sense, the convention in economics of referring to an inflation-adjusted interest rate as a "real interest rate" is misleading. The real rate of interest is not real in the sense that we can go out and easily observe it the economy. Certainly, we can measure the inflation-adjusted return that an investor receives after a debt contract has matured, but this ex post measure tells us only how inflation has eroded the return on an investment over some past period.

When it comes to analyzing current economic conditions and evaluating the outlook for the future, a more relevant measure of the real interest rate is a forward-looking measure. Since the decisions of savers and investors in an economy are predicated on their expectations about the future, it is the level of current market interest rates adjusted for expected future inflation-the ex ante real rate of interest-that matters.

Measuring expectations, of course, is an inherently difficult matter. We can conduct surveys, estimate statistical models, draw inferences from economic theory, but we can never measure precisely the public's attitude about the outlook for inflation. In fact, it is precisely this prospect of disentangling inflation expectations from observed market interest rates that makes the evaluation of real interest rates so challenging

http://www.stls.frb.org/general/speeches/990921.html

Throwing Cold Water On Dow 36,000 View

Wall Street Journal,

September 21, 1999

Why care what Mr. Siegel thinks? For starters, he wrote a far better book, "Stocks for the Long Run," first published in 1994. Like "Dow 36,000," Mr. Siegel's book prodded investors to buy stocks, but without making outlandish forecasts about future returns.

Faced with that possibility, the author of "Stocks for the Long Run" thinks it might be smart to keep some money in inflation-indexed bonds, which provide a guaranteed return above inflation.

"You can lock in 4% real returns in inflation-indexed bonds today," Mr. Siegel notes. "There will come a time when people will look around and say, 'That's a deal.' "

Stocks for the Long Run. Irwin Professional Publishing, 1994.; 2nd ed., McGraw Hill, 1998.

Inflation-Linked Bonds

An inflation-linked bond is a bond that provides protection against inflation. Most inflation-linked bonds, the Canadian "Real Return Bond "(RRB), the British "Inflation-linked Gilt" (ILG) and the new U.S. Treasury "inflation-protected security" (IPS) are principal indexed. This means their principal is increased by the change in inflation over a period.

In most countries, the Consumer Price Index (CPI) or its equivalent is used as an inflation proxy. As the principal amount increases with inflation, the interest rate is applied to this increased amount. This causes the interest payment to increase over time. At maturity, the principal is repaid at the inflated amount.

In this fashion, an investor has complete inflation protection, as long as the investor's inflation rate equals the CPI.

http://www.finpipe.com/infbonds.htm

Nouriel Roubini and David Backus Lectures in Macroeconomics

Chapter 5. Output and Real Interest Rates

Application: Real Interest Rates

in the 90s

One of the many things that was different about the 1980s is that the real rate of interest was higher than we've seen before in the postwar period (in fact, I doubt there's another period in history like this). In the 1950s the average real interest rate (nominal rate minus inflation rate) on one-year treasuries was 0.12, in the 1960s 1.97, 1970s 0.28, and 1980s 4.37. We could document similar rates in most of the OECD countries. There's clearly something different about the 1980s. But what?

http://equity.stern.nyu.edu/~nroubini/NOTES/CHAP5.HTM

U.S. Treasury Inflation-Protected Securities (TIPS)

A new age dawned in the U.S. capital markets on Wednesday, January 29, 1997. The United States Treasury made its first issue of an inflation-linked bond, the 3.375% of 2007.

This bond increases its principal by the changes in the Consumer Price Index (CPI). Its interest payment is calculated on the inflated principal, which is eventually repaid at maturity. This gives an investor the ability to protect against inflation while providing a certain "real" return over an investment horizon.

Despite critics and uncertainty over the "great inflation debate", the auction went extremely well with interest five times the size of the $7.0 billion issue. The "real yield" of the TIP reached more than 3.5% in the "when issue" trading before the auction but fell dramatically to 3.3% in the aftermarket trading.

http://www.finpipe.com/tips.htm

The Real Interest Rate–No Longer A Mystery

On January 29, the U.S. Treasury issued its first inflation indexed bonds, known as Treasury Inflation Protection Securities (TIPS). These securities sold to yield a real rate of interest of 3.44%. Since the issue was greatly oversubscribed (demand was five times supply), the rate of interest in the future will likely be somewhat higher. Also, the real rate reflected in this issue is based more on the way the CPI will be measured in the future than it is today (remember that securities pricing is forward looking).

The bottom line of all of this is that the real rate of interest is probably about 4% and the real rate of wage growth about 1%, when inflation is measured by the "new" methods that will be announced sometime this year. This yields a net discount rate in the neighborhood of 3% and debunks completely the total offset argument.

These new issues are also not true ten year instruments. Since they index every six months, they can be sold at virtually anytime with no loss of principal. In other words, they are 180 day T-bills that roll not traditional ten year bonds.

The issuance of these new securities presents many new ways of demonstrating the ridiculous, uneconomic nature of the calculations made by most plaintiff’s economists. It should now be much easier to cut through the babble.

http://www.spectrumeconomics.com/realinterest.html

Adjusting Interest for Inflation

http://william-king.www.drexel.edu/top/prin/txt/complete/int6.html

Real Interest Rates and Investment and Borrowing Strategy

By Peter S. Spiro Quorum Books. Westport, Conn. 1989.

238 pages LC 89-3864. ISBN 0-89930-453-2. SIJ/ $62.95

http://info.greenwood.com/books/0899304/0899304532.html

Mer om realräntor - More about real interest rates