Ben Bernanke

European banks still have post-crisis repairs to do

Former US policymakers say their counterparts did not do enough to stop the rot

Gillian Tett FT 19 July 2018

David Stockman's Conspiracy Theory

Along with Goldman’s plenipotentiary at the US Treasury, Hank Paulson,

Bernanke stampeded the entirety of Washington into tossing out the window the whole rule book of

sound money, fiscal rectitude and free market discipline.

In fact, there was no extraordinary crisis.

The Lehman failure essentially triggered a self-contained leverage and liquidity bust in the canyons of Wall Street

13 April 2016

Faced with the most severe economic downturn since the Great Depression, the U.S. Federal Reserve did the only thing it could: flood the financial system with liquidity.

The move to so-called easy money arguably saved the world from a worse fate and radically changed the economic backdrop as well as the landscape for financial markets.

Bloomberg via englundmacro.blogspot.se/2016/02/these-are-things-that-correlate

– It is difficult to read former US Federal Reserve Chair Ben Bernanke’s new memoir, The Courage to Act, as anything other than a tragedy.

It is the story of a man who may have been the best-prepared person in the world for the job he was given, but who soon found himself outmatched by its challenges, quickly falling behind the curve and never quite managing to catch up.

It is to Bernanke’s great credit that the shock of 2007-2008 did not trigger another Great Depression. But...

J. Bradford DeLong, Project Syndicate, 29 October 2015

Full text

Top of page

News

davidstockmanscontracorner.com/professor-bernankes-bogus-contra-factual-part-1-the-myth-of-great-depression-2-0/

davidstockmanscontracorner.com/professor-bernankes-bogus-contra-factual-part-2-why-the-friedmanbernanke-thesis-about-the-great-depression-was-dead-wrong/

1929

Lunch with Ben Bernanke

I turn, finally, to perhaps the biggest question about the crisis. Could they have avoided the failure of Lehman in September 2008?

“No,” he responds firmly. “It was completely unavoidable. Without a buyer, there was no one to guarantee their liabilities. So no one would lend to them. There was a complete run of all the creditors, all of the counterparties, all of the customers.

And if we had lent them the money and somehow conjured up some fake collateral, in violation of the law, we would have ended up owning the firm, and it would have been a non-viable firm.”

Martin Wolf, FT 23 October 2015

In his new memoir, The Courage to Act, Bernanke sets out an exhaustive account of his actions during his eight years as chairman,

essentially arguing that, had it not been for the interventions the Fed eventually championed, America’s fate would have been incalculably worse.

Financial Times, 11 October 2015

The unanswered question today is why, after trillions of dollars of stimulus from Bernanke and his colleagues, the US is still struggling with only a pedestrian recovery.

Part of the answer undoubtedly lies on Capitol Hill, which fecklessly reined in fiscal stimulus too abruptly amid the crisis.

Full text

Amazon

Top of page

News

Bernanke Isn’t Serious

His latest on Greece and the euro suggests that the deeper problems lie not in Greek fecklessness

but in the refusal of the core — basically Germany — to allow either monetary or fiscal policies that would offset the downdraft from austerity in the periphery.

He even questions the sacred status of “structural reform”

Paul Krugman 17 July 2015

As I’ve tried to point out for a long time, in this policy debate the supposedly radical types are the ones doing standard, more or less textbook economics,

while the respectable voices have subscribed to fantasies ungrounded in either history or theory.

Full text

Top of page

Ben Bernanke – a distinguished scholar, he brought to the Fed a brilliant and well-informed mind.

His knowledge of economic history helped him halt a terrifying panic.

But he also made mistakes.

History will probably judge him kindly. But there is much to be learnt from his time at the Fed.

Martin Wolf, FT 21 January 2014

Former Federal Reserve Chairman Ben Bernanke believes

history has already vindicated the novel efforts of the U.S. central bank to revive the economy after the financial crisis of 2008.

MarkerWatch 29 December 2014

The Fed and the Bank of England offered financial aid to beleaguered banks and deployed tools such as quantitative easing — creating new money — on a massive scale to help heal badly damaged economies.

The result has been that the U.S. and Britain have grown much faster than the European Union, whose response has been less aggressive.

Full test

Top of page

David Wessels bok om finanskrisen 'In Fed we Trust' Ben Bernanke's War on the Great Panic

I december firade Federal Reserve 100 år.

I december var det också fem år sedan styrräntan sänktes mot noll.

Louise Andrén Meiton, SvD 28 mars 2014

Ben Bernanke – a distinguished scholar, he brought to the Fed a brilliant and well-informed mind.

His knowledge of economic history helped him halt a terrifying panic.

But he also made mistakes.

History will probably judge him kindly. But there is much to be learnt from his time at the Fed.

Martin Wolf, FT 21 January 2014

First, in his 2004 praise for the great moderation, the vainglorious label given to the performance of the US economy before the largest financial and economic crisis for 80 years,

Mr Bernanke claimed that “better monetary policy may have been a major contributor to increased economic stability”.

As the disregarded economist Hyman Minsky tried to tell us, stability destabilises.

An active and enterprising financial system creates risk, often by raising leverage dramatically in good times.

Second, he missed the implications of subprime mortgages.

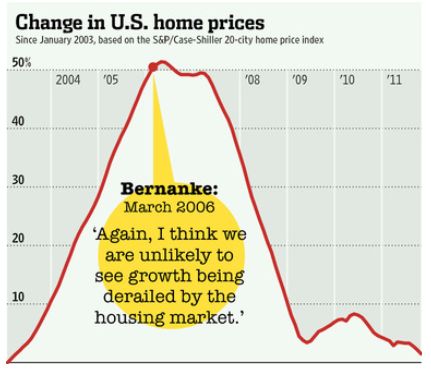

Thus, in May 2007, he remarked that “we believe the effect of the troubles in the subprime sector on the broader housing market will probably be limited,

and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system”.

Fortunately, when it became evident that this judgment was in gross error, the Bernanke Fed acted decisively and effectively, slashing interest rates and sustaining credit. As panic-fighter Mr Bernanke followed the guidance of the great Victorian economic journalist Walter Bagehot, who urged unrestricted lending by central banks to solvent institutions in times of crisis. This is a world of manias and panics. Happily, Mr Bernanke knew this.

Full text

Martin Wolf at IntCom

Bernanke has been a great Fed chairman who helped to avert financial meltdown

His emergency policies aided recovery

but now Yellen must engineer a successful escape

Roger Bootle, 2 Feb 2014

Top of page

The inevitability of instability

Buttonwood Jan 25th 2014, The Economist print edition

That is the shared conclusion of two thoughtful analyses:

a paper* by Marcelo Prates of the Brazilian central bank

and a speech** in New Delhi by Adair Turner, a former head of Britain’s Financial Services Authority.

A fundamental instability results from the mismatch between the assets banks hold (long-term loans)

and their liabilities, in the form of short-term deposits

Individuals may use credit as a means of financing consumption in excess of their income, as was the case with American homeowners in the past decade. This process is self-reinforcing: easier credit drives up asset prices, which makes banks confident and leads them to lend more.

These credit cycles lead to greater volumes in the financial markets, as assets are traded back and forth. Banks end up with an awful lot of claims on each other, a development which added to the panic in 2008. It is hard to see how this extra trading benefits the economy; it certainly does not ensure that asset prices stay in line with economic fundamentals.

Full text

Ben Bernanke about what caused the financial crash

So what was the reason, according to the man who was easily the most powerful person in the world for nearly a decade?

Ready?

"Overconfidence."

Tyler Durden, zerohedge, 4 March 2014

Top of page

– Om vi ser att de ekonomiska förbättringarna håller i sig kan centralbanken vara redo

att trappa ner på sina stimulansköp under de nästa mötena.

Ungefär så lät det från centralbankschefen Ben Bernanke den 22 maj

Enligt uppgifter från Bank of America Merrill Lynch har de globala börserna

förlorat 3000 miljarder dollar, cirka 20 000 miljarder kronor, i värde sedan den 22 maj.

Daniel Kedersted, SvD Wall Street blog, 14 juni 2013

Fed History Shows Punch Bowl Goes as Jobs Rise

An improving labor market rather than accelerating inflation

made the Federal Reserve decide to end its last three episodes of easy monetary policy.

Simon Kennedy Bloomberg May 24, 2013

An improving labor market rather than accelerating inflation made the Federal Reserve decide to end its last three episodes of easy monetary policy.

It may be about to happen again, says Barclays Plc strategist Barry Knapp.

He looked back to May 1983, February 1994 and the February-to-August period of 2004 to see what prompted the U.S. central bank to tighten policy,

which former Fed chief William McChesney Martin likened to taking away the punch bowl just as the party gets going.

In all three cases, inflation measures were generally falling.

It was employment, the other part of the Fed’s dual mandate, that spurred a policy shift,

wrote Knapp, head of U.S. equity strategy at Barclays in New York.

Full text

Stabiliseringspolitik

Top of page

Monetarists from across the world can mostly agree on one thing.

The US Federal Reserve caused the Great Recession.

The "Bernanke Depression" if you want, a term gaining traction in elite circles.

Ambrose Evans-Pritchard, 23 September 2012

That is a demonstration of the fact that the world has a huge “savings glut”, an idea famously proposed by Ben Bernanke in 2005“

The Global Saving Glut and the U.S, Current Account Deficit”, March 10 2005,

What is the real rate of interest telling us?

The real interest rate on US and UK government debt is currently near to zero

Martin Wolf, 19 March 19 2012

Chairman Ben S. Bernanke

At the Federal Reserve Bank of Kansas City Economic Symposium, Jackson Hole, Wyoming

August 31, 2012

Bernanke:

Low Rates Didn’t Cause the Housing Bubble

I suppose if I were the head of the Federal Reserve and I had lowered short-term interest rates to freakishly low levels a few years ago and I had promised to keep them there for another few years that I too would probably continue to argue that freakishly low interest rates did not contribute to the massive credit and housing bubble and the financial crisis that followed

Tim Iacono 23 March 2012

I thought everyone stopped calling the Greenspan years “The Great Moderation” since it ended in such a bust under Bernanke.

Full text

Top of page

Come on Bernanke, fire up the helicopter engines

Samuel Brittan, Financial Times, August 30, 2012

As Ben Bernanke, chairman of the Federal Reserve, explained in an important speech on April 13,

central banks have expanded their balance sheets because those of the private financial sector collapsed.

That is what a lender of last resort is supposed to do during a severe panic. We have known this since the 19th century

Martin Wolf, Financial Times, 1 May 2012

The Near- and Longer-Term Prospects for the U.S. Economy

Chairman Ben S. Bernanke, Jackson Hole, Wyoming, August 26, 2011

Full text here

As a Princeton economics professor from 1985 to 2002 and a Fed governor from 2002 to 2005,

Bernanke -- a student of the Great Depression and Japan’s lost decade --

faulted central bankers for failing to act aggressively in both cases to provide credit

and weed out sickly financial institutions as they tried to rescue their economies and combat deflation.

Bloomberg 26 August 2011

Bernanke admonished Japanese officials for their unwillingness “to experiment, to try anything that isn’t absolutely guaranteed,” in a 1999 paper on their monetary policy. “Perhaps it’s time for some Rooseveltian resolve,” he urged, referring to U.S. President Franklin Roosevelt’s sometimes unpopular efforts to push through Congress fiscal and social programs to pull America out of its worst slump.

Full text

Top of page

Federal Reserve Chairman Ben S. Bernanke said additional monetary stimulus may be warranted

because inflation is too low and unemployment is too high.

Blooomberg Oct 15, 2010 2:43 PM GMT+0200

Top of page

The Bernanke trap

Speech at the annual Federal Reserve retreat in Jackson Hole

to do whatever is necessary to keep the economy from stumbling down the Japanese path

CNN/Fortune, August 27, 2010, with good links

Top of page

I want to be very, very clear: too big to fail is one of the biggest problems we face in this country, and we must take action to eliminate too big to fail.

Ben Bernanke, Time Person of the Year, December 2009

Read more:

I want to be very, very clear

Too big to fail

The Fed and the Crisis: A Reply to Ben Bernanke

In his recent speech, the Fed chairman denied that too-low interest rates were responsible.

Does this mean we're headed for a new boom-bust cycle?

John B. Taylor WSJ JANUARY 10, 2010

Full text

John Taylor

Monetary Policy and the Housing Bubble

Chairman Ben S. Bernanke

"Some observers have assigned monetary policy a central role in the crisis. Specifically, they claim that excessively easy monetary policy by the Federal Reserve in the first half of the decade helped cause a bubble in house prices"

January 3, 2010

Om det finns något kritiskt att säga om Ben Bernanke så är det att han var blind för finanskrisen – fram till att den inträffade. Under lång tid avfärdade han varningarna om en bubbla på bostadsmarknaden.

I likhet med sin företrädare Alan Greenspan ansåg inte Bernanke att det var centralbankernas sak att bromsa bostadsrallyt.

Peter Wolodarski 2009-12-27

Inte ens efter att investmentbanken Bear Stearns gick omkull våren 2008 förstod han vilka krafter som var i rörelse. På sommaren det året varnade han i stället för ekonomisk överhettning. Ett par månader senare kollapsade Lehman Brothers, med Bernankes goda minne, och drog med sig den amerikanska ekonomin i fallet.

Först då ringde alla varningssignaler.

Full text

Bernanke was as clueless as Greenspan about the coming storm. He dismissed warnings of a housing bubble. He insisted that economic fundamentals remained strong. In March 2007, he assured Congress that "the problems in the subprime market seem likely to be contained." The day before the global crisis erupted with a run on a French bank, the Fed was still saying its primary concern was inflation.

TIME Person of the Year 2009

“Why did no one see the crisis coming?” Queen Elizabeth asked

Her Majesty’s question ("If these things were so large, how come everyone missed them?")

Chris Giles, FT, November 25 2008

In 2008, as the global financial crisis unfolded, the reputation of economics as a discipline and economists as useful policy practitioners seemed to be irredeemably sunk. Queen Elizabeth captured the mood when she asked pointedly why no one (in particular economists) had seen the crisis coming.

There was no doubt that, notwithstanding the few Cassandras who correctly prophesied gloom and doom, the profession had failed colossally.

The totemic symbols of this failure were, of course, the two most important policymakers, Alan Greenspan and his successor as chairman of the US Federal Reserve, Ben Bernanke. They, among many others, helped create a belief system that elevated markets beyond criticism.

Arvind Subramanian, FT December 27 2009

Will the Federal Reserve's actions to combat the crisis lead to higher inflation down the road?

The answer is no; the Federal Reserve is committed to keeping inflation low and will be able to do so.

Chairman Ben S. Bernanke At the Economic Club of Washington D.C., Washington D.C. December 7, 2009

That 1999 Time magazine cover is finally catching up with Lawrence Summers.

That was the year Summers was celebrated along with Alan Greenspan and Robert Rubin as “The Committee to Save the World”

for their free-market solutions to Asia’s financial crisis.

The timing always struck Asians as odd, given that they were still picking up the pieces

from a meltdown made worse by the trio’s ill-conceived and overbearing remedies.

William Pesek, a Bloomberg View columnist, Aug 5, 2013

No, the Asian central banks that hold more than $3 trillion in U.S. Treasuries won’t panic if President Barack Obama chooses Summers.

Even detractors admit Summers is a brilliant economist and thinke

Yet the prickly Summers faces some major image problems. Tens of millions of Asians - and more than a few policy makers - are still seething over his role in forcing painful austerity measures on governments in the late 1990s.

He and his boss at the time, Treasury Secretary Rubin, applied a blunt, one-size-fits-all reform approach that Indonesians, Malaysians, South Koreans and Thais haven’t gotten over - and the Time cover hardly helped.

Full text

Summers

Rubin

In 1999, Alan Greenspan, Robert Rubin and Lawrence Summers were celebrated as

“The Committee to Save the World” on the cover of Time magazine.

Committee to Save World Repudiated by Successors

Bloomberg, Ian Katz 23 March 2012

The three were hailed as the brightest economic minds of their generation, whose free-market solutions quelled the Asian financial crisis while generating economic growth of almost 5 percent in the U.S.

A year before their magazine fame, they thwarted efforts by Brooksley Born, then-chairman of the Commodity Futures Trading Commission,

to regulate the over-the-counter derivatives market,

which ballooned to include the toxic instruments that ravaged American International Group Inc. (AIG) and Lehman Brothers

Full text

Financial officials from the United States, once called “the committee to save the world” after the Asian crisis in the 1990s,

now find themselves uttering apologies for the harm caused to the world by the 2008 financial crisis and

coating their advice to European nations with the knowing nod of the battle-hardened.

New York Times 16 Sept 2011

Full text

Ben Bernanke Time Magazine "Person of the Year"

Time magazine famously named Mr. Greenspan, Robert Rubin and Lawrence Summers “The Committee to Save the World” — the “Three Marketeers” who “prevented a global meltdown.”

Tim Iacono 16/12 2009

“Three Marketeers” who “prevented a global meltdown.”

http://www.time.com/time/covers/0,16641,19990215,00.html

http://www.time.com/time/magazine/article/0,9171,990206,00.html

Full text at Tim Iacono

Greenspan, Robert Rubin and Lawrence Summers

Top of page

Bernanke, who has been studying the causes of the Depression since he was a graduate student at Massachusetts Institute of Technology, said on Nov. 16 that it’s “not obvious” that asset prices in the U.S. are out of line with underlying values. He didn’t address asset prices outside of the country. In 1989, he wrote an article with Mark Gertler, a New York University economics professor, for the American Economic Review in which they presented a detailed model that helps to explain the cascade of events that led to the collapse of markets in the years after the 1929 crash.

“It is inherently extraordinarily difficult to know whether an asset’s price is in line with its fundamental value,” Bernanke said in response to audience questions after a speech in New York. “It’s not obvious to me in any case that there’s any large misalignments currently in the U.S. financial system.”

Nov. 23 2009 Bloomberg

Federal Reserve chairman Ben Bernanke played his part Monday in foreshadowing the dollar’s grim future. He offered the hollow assurance that

the fed was “attentive to the implications of changes in the value of the dollar.”

Such benign neglect whispers the truth: impotence in the face of impending misfortune.

Charles Goyette, author of The Dollar Meltdown: Surviving the Impending Currency Crisis with Gold, Oil, and Other Unconventional Investments.

CNBC 17 Nov 2009

I can find no reports of Obama having made smooth promises to the Chinese that the dollar’s value will be maintained. This allowed his hosts to maintain a courteous decorum. It would have been unseemly for the president to provoke the outright laughter that greeted Treasury secretary Tim Geithner last summer in Beijing when he made assurances about the safety of Chinese dollar investments.

Full text

Top of page

That’s not to suggest that there is no room for coordination between the monetary and fiscal authorities. This is particularly the case when the economy is experiencing asset deflation, begetting debt deflation and deleveraging. Indeed, none other than Chairman Bernanke made this case when he was Governor,

first in November 2002 in his famous speech titled

“Deflation: Making Sure ‘It’ Doesn’t Happen Here”,

and then in May 2003, in a speech titled “Some Thoughts on Monetary Policy in Japan”.

The Paradox of Deleveraging

Paul McCulley, July 2008

Top of page

US Federal Reserve chief Ben Bernanke says the world is suffering

from the worst financial crisis since the 1930s.

Mr Bernanke argues that the roots of the current global economic downturn stem from

global imbalances in trade and flows of capital in the late 1990s.

BBC 10/3 2009

In a speech to the Council on Foreign Relations, he argues that the US and its trading partners did not do enough to redress these imbalances.

Mr Bernanke says the imbalances "reflect a chronic lack of saving relative to investment in the US and some other industrial countries, combined with an extraordinary increase in saving relative to investment in many emerging markets."

Full text

U.S. Trade Deficit:

If something cannot go on forever it will stop, Rolf Englund 2001

To put it in monetary policy terms, the Fed is boosting the supply of money to offset the decline in velocity,

which is the amount of turnover in the money stock.

Velocity has been falling like a newspaper stock amid the panic.

For our readers who recall their economic textbooks, Irving Fisher's famous equation is MV=PT.

Wall Street Journal editorial 30/10 2008

Top of page

Removal of the famous "Greenspan put"

On Monday, June 9, Bernanke gave a pathbreaking speech entitled "Outstanding Issues in the Analysis of Inflation"

In two sentences, he contributed to a sharp, fifty-basis-point rise in two-year bond yields. Bernanke said:

[T]he latest round of increases in energy prices has added to the upside risks to inflation and inflation expectations. The Federal Open Market Committee will strongly resist an erosion of longer-term inflation expectations, as an unanchoring of those expectations would be destabilizing for growth as well as for inflation.

With those two sentences, Bernanke embarked on a path that may lead to whereby the Fed avoids policy measures that could cause systemic risk in financial markets.

John H. Makin, June 26, 2008

Full text

Comment by Rolf Englund:

I have been reading John Makin for some twenty years I guess, and still become

more and mor impressed by him.

Articles and Short Publications by John H. Makin

Why Do Financial Firms Take Too Much Risk?

The principal/agent problem

- where interests of managers of financial intermediaries diverge from those of their shareholders -

has been clearly illustrated by the widely publicized cases of Merrill Lynch and Citigroup.

John H. Makin, American Enterprise Institute, November 20, 2007

Top of page

If there were a Central Bank of the World its monetary policy committee would glance at today’s inflation rates and expectations of future inflation and then raise interest rates.

There is no such bank, but there is something close: the US Federal Reserve, the monetary policy of which is mirrored by many countries in the Middle East and Asia.

low Fed interest rates are contributing to global inflation.

The Fed sets interest rates for Asian countries because, explicitly or not, they manage their exchange rates against the dollar.

If US interest rates are low, countries targeting the dollar are obliged to follow, because otherwise investors will sell dollars to buy their currency.

Financial Times editorial, June 25 2008

Don Kohn, the vice-chairman of the Federal Reserve

believes that the global economic system would function better if emerging economies had a greater degree of monetary independence, allowing them to set the interest rates appropriate for their own economies.

Chairman Ben S. Bernanke: Outstanding Issues in the Analysis of Inflation

FT June 26 2008

Barclays warns of a financial storm as Federal Reserve's credibility crumbles

US central bank accused of unleashing an inflation shock that will rock financial markets

Ambrose Evans-Pritchard, Daily Telegraph 27/6 2008

After spending nine months cutting interest rates and lending freely to financial firms in a bid to ease the pain of the credit crunch, the Federal Reserve has reversed course.

Bernanke and other Fed officials have signaled in recent weeks that

the Fed now sees fighting inflation, rather than preventing a severe economic slowdown, as its top priority.

CNN/Fortune 12/6 2008

Full text

Top of page

Helicopter Ben Bernanke stepped over the line again, taking on the role of the US Treasury Secretary, and blew HOT AIR at the dollar exchange market.

He is next in line to destroy his personal credibility.

Unfortunately for us all, as Big Ben goes so does the credibility of the central bank of the world's reserve currency - the Federal Reserve.

The Market Oracle 11/6 2008

Bernanke believes that the danger of a “substantial downturn” in the US economy has abated over the past month,

but that inflation risks are increasing.

FT June 10 2008

Bernanke, a longtime scholar of the 1929-to-1933 panic,

now has the unwelcome task of trying to keep a new financial calamity from turning into a full-blown depression.

What started as a meltdown in the market for subprime mortgages has turned into a worldwide credit and economic crisis.

Bernanke, now the Fed chairman, has responded with the most-aggressive expansion of the Fed's power in its 95-year history.

Bloomberg, April 21 2008

Full text

Bernanke speech at the International Monetary Conference laying out all the reasons

why the Federal Reserve is NOT responsible for the present crisis in the financial markets.

"It's all China's Fault!":

The Market Oracle Jun 08, 2008

Ask yourself this, dear reader; do "savings" cause massive equity bubbles or are bubbles the result of low interest rates and rotten monetary policy?

Full text

Factor-price equalization - Faktorprisutjämning

Top of page

Ben Bernanke: "We have a problem"

'We have a problem, which is that the spreads between the Treasury rates and lending rates are widening, and our policy is essentially, in some cases just offsetting the widening of the spreads, which are associated with signs of illiquidity."

Eurointelligence/calculatedrisk blog 29/2 2008

Top of page

Two weeks ago, the world financial system hung by a thread as a battle raged among corporate leaders, government officials, portfolio managers and independent traders to control its destiny.

Half wanted to pull it down and spill the globe into economic Armageddon for personal profit, while the other half fought to stave them off.

Jon Markman, CNBC 27/3 2008

Bernanke Asks Taxpayers To Bail Out Banks

Mish March 04, 2008

"Downside risks to growth remain, including the possibilities that the housing market or the labor market may deteriorate to an extent beyond that currently anticipated, or that credit conditions may tighten substantially further."

Ben Bernanke, testimony before the Senate Banking Committee, February 14, 2008

Top of page

In a dramatic change of tone Ben Bernanke indicated that the Federal Reserve is ready to cut interest rates aggressively to ward off the risk of a US recession

FT January 10 2008

The Fed chairman said “we stand ready to take substantive additional action as needed to support growth and to provide additional insurance against downside risks”.

Full text

More about recession

Top of page

There was a definite Hirohito feel to the explanation Ben Bernanke gave Krugman

When announcing Japan’s surrender in 1945, Emperor Hirohito famously explained his decision as follows: “The war situation has developed not necessarily to Japan’s advantage.”

Ben Bernanke: “Market discipline has in some cases broken down, and the incentives to follow prudent lending procedures have, at times, eroded.”

More about Hedge Funds/Subprime

Banks Gone Wild Paul Krugman NYT Nov 23 2007

This slump was both predictable and predicted.

“These days,” I wrote in August 2005, “Americans make a living selling each other houses, paid for with money borrowed from the Chinese. Somehow, that doesn’t seem like a sustainable lifestyle.”

It wasn’t.

Krugman om EMU

In the end, the Fed can always stop a deflationary spiral.

As Bernanke said to Milton Freidman on his 90th birthday,

the Fed will not repeat the monetary crunch it allowed to happen 1930-32.

"Regarding the Great Depression. You're right, we did it. We're very sorry.

But thanks to you, we won't do it again."

Ambrose Evans-Pritchard on 14 Dec 2007

Merrill says the Fed may cut rates to 2pc. (rates were 1pc in 2003 and 2004).

Let me go a step further. It would not surprise me if debt deflation in the Anglo-Saxon countries proves so serious that we reach Japanese extremes – perhaps zero rates, with a dollop of 'quantitative easing' for good measure.

The Club Med states may need the same, but they will not get it because they no longer control their monetary policy.

So Heaven help them and their democracies.

Bernanke is undoubtedly right. The Fed won’t do it again. But before the United States can embark on an economic course that radically transforms the nature of capitalism, speculative markets may have to take a beating - for appearances sake, at least.

Full text

Början på sidan - Top of page

Milton Friedman

1929

What we are witnessing is essentially the breakdown of our modern day banking system, a complex of levered lending so hard to understand

that Fed Chairman Ben Bernanke required a face-to-face refresher course from hedge fund managers in mid-August.

Bill Gross, December 2007

Should central banks take account of asset prices?

This was until recently one of the most hotly debated subjects in monetary economics.

As of this week, the issue has been effectively settled.

Everybody now believes, or rather acts as if, they should.

Eurointelligence, 19/9 2007

Highly recommended

Central banks should not rescue fools

Martin Wolf, Financial Times, August 29 2007

Fed can inject liquidity into the U.S. market and support the U.S. stock market and banks,

but it only moves the crisis of confidence from the lower lying banking level to the currency level

Charlie, September 27, 2007

The Fed claims that if inflation rises, they will raise interest rates, thereby reducing aggregate demand, slowing the economy, and eliminating the excesses that are causing capacity constraints and inflation. If the economy slows, the Fed will lower rates, which will have the opposite effect. This Fed model, however, is flawed, because what happens if there is a crisis of confidence, and people start moving money away from the dollar?

The risk the Fed is running is that if the world begins to lose faith in the dollar then the Fed is useless. The dollar, and their ability to print more dollars, is the source of the Fed's power. Without that, they will just be a bunch of useless academics.

According to the New York Times, “In July 2001, Paul McCulley, an economist at Pimco, the giant bond fund, predicted that the Federal Reserve would simply replace one bubble with another. ‘There is room,’ he wrote, ‘for the Fed to create a bubble in housing prices, if necessary, to sustain American hedonism. And I think the Fed has the will to do so, even though political correctness would demand that Mr. Greenspan deny any such thing.’

Full text

If holders of the dollar conclude it is no longer a secure store of value

they will dump both the currency and assets dependent on its future value.

If that were to happen, the Fed would confront a dreadful dilemma

– whether or not to cut rates as the dollar plunged and long-term interest rates soared.

Martin Wolf, Financial Times 26/9 2007

To critics it is now the “Bernanke put”

It would be wonderful if those responsible for this most absurd of financial crises could be punished without damaging millions of innocent bystanders.

But it is impossible. If the Fed does its job, it helps the financial sector. The latter will, no doubt, recover and then find some new, imaginative and currently unforeseen way to generate a possibly bigger crisis several years hence. Whereupon, it will expect the Fed to do its job, as Wall Street sees it: saving the economy, by saving finance.

Moral hazard matters, but only for the poor.

The resolution of each crisis lays the seeds of the next. Thus, the easing by the Fed after the east Asian and Russian crises of 1997 and 1998 contributed to the subsequent stock market bubble. The dramatic easing after its bursting in 2000 contributed to the recent housing boom. The disruption in money markets brought about by the end of that boom has led to last week’s sharp cut in rates. The question, then, is what this will lead to.

One possible answer would be a true nightmare: the return of inflation.

A huge number of highly indebted households find that their principal assets, their houses, are falling in price. A higher price level is then a far less painful way to restore equilibrium than falling nominal prices. Externally, the US is a huge net debtor. A large dollar devaluation is then a far less painful way to turn it into a net creditor than running current account surpluses, since its liabilities are denominated in dollars.

Full text

More by Martin Wolf

Top of page

The Fed can indeed be accused of being a serial bubble-blower.

But this is not because it has been managed by incompetents.

It is because it has been managed by competent people responding to exceptional circumstances.

Martin Wolf, August 22 2007

Bernanke, 53, hasn't made any public comments since July.

He'll break his silence with a speech on housing and monetary policy Aug. 31 at the Fed's annual retreat-cum-symposium in Jackson Hole, Wyoming,

before central bankers and economists from around the world.

Bloomberg 27/8 2007

Full text

At the Federal Reserve’s annual retreat in Jackson Hole, Wyoming almost eight years ago to the day, Ben Bernanke presented a paper to Alan Greenspan and other central bankers from around the world setting out how they should respond to changes in the price of stocks, bonds and other assets.

Krishna Guha, Financial Times, August 18 2007

At the time, Mr Bernanke was chairman of the economics faculty at Princeton University, one of the foremost academic economists of his generation, but unknown outside his profession.

In his 1999 Jackson Hole paper Mr Bernanke and his co-author, Mark Gertler, argued that a central bank should move rates in response to changes in asset prices, but only to the extent that they affect the outlook for the real economy.

A year later in an article in Foreign Policy magazine he put the question in layman’s language: “If Wall Street crashes does Main Street follow? Not necessarily.”

Most traders are desperate for a rate cut. Jim Cramer, hedge fund manager and rambunctious CNBC television pundit, spoke – or rather shouted – for them when he demanded the Fed wake up and cut rates.

“Bernanke is being an academic...He has no idea how bad it is out there. He has no idea!”

But many economists and central bankers believe a rate cut risks the “moral hazard” of bailing out reckless investors. Bill Poole, president of the St Louis Fed, told Bloomberg only a “calamity” would justify a rate cut now.

Mr Bernanke’s position is made harder by his predecessor’s long shadow. Investors loved Mr Greenspan, who over the years defused a string of financial crises. But some economists fault him for allowing investors to believe that if things ever got really bad, the Fed would step in to rescue the markets.

His instincts as an economic historian and theoretician who has studied the Great Depression and other financial crises that will guide him now. Larry Meyer, a former Fed governor and chairman of Macroeconomic Advisers, says Mr Bernanke knows better than most – having written extensively on it – how the credit system works and the role collateral plays in it.

Full text

Nouriel Roubini and Marc Faber Are Not Impressed

naked capitalism blog 20/8 2007

Fedstyrelsen beslutat att temporärt sänka diskontoräntan med 50 punkter till 5,75 procent,

för att minska skillnaden mellan diskontoräntan och

Feds mål för overnighträntan, Fed funds, som lämnas oförändrad på 5,25 procent.

DI/Direkt 17/8 2007

They have changed the terms: institutions can borrow money for 30 days now, rather than overnight,

at the discount rate, and cheaper than before.

The Fed is essentially saying, go out, lend, don't worry about it.

CNBC's Bob Pisani

Here is the statement in its entirety

*

The subprime-mortgage-market meltdown is a classic example of the way small fry get devoured,

but the whales of Wall Street get rescued.

Here's the deal:

Allan Sloan, Fortune senior editor-at-large, August 17 2007

Cramer Pleads for a Fed Rescue

In a truly astonishing clip, Erin Burnett interviewed Jim Cramer on Friday. It is destined to become a classic Wall Street legend. I expect it will become required viewing for market historians and technicians alike.

"Open the darn Fed window. "He has no idea what its like out there - None!"

Watch it here

Kudlow doomster???

Caveat Emptor

by Lawrence Kudlow

When in doubt, don’t cut rates

Kudlow's Money Politic$, 23/3 2007

Top of page

Anyway, our esteemed Chairman of the Federal Reserve, Ben Bernanke has written and spoken extensively on the subject of deflation, and I have included a long quote of his below, not to highlight his wit and sense of humor, but rather to show how well understood these issues are and to demonstrate the various tools the government has to overcome them:

- The Congress has given the Fed the responsibility of preserving price stability (among other objectives), which most definitely implies avoiding deflation as well as inflation.....

In my mind, deflation CANNOT occur

Charles Zentay, March 28, 2007

Top of page

Federal Reserve chairman Ben Bernanke

crisis in the US sub-prime lending market could cost up to $100bn.

BBC 20/7 2007

Can the Fed Control Prices?

Bernanke admitted that he has no control over asset prices or even key interest rates. But does he have control over any prices?

Michael Shedlock 20/7 2007

Top of page

However, sales of new homes have fallen, and continuing declines in starts have not yet led to meaningful reductions in the inventory of homes for sale.

Chairman Ben Bernanke, 28/3 2007

Recession in 2007?

Greenspan's recession comment opened the floodgates for the use of the "r word."

John H. Makin, 21/3 2007

Bernanke:

To understand and evaluate conditions in the bond market, he said,

“the Fed must take into account the various effects of foreign capital flows on US yields and asset prices, a task that can be quite challenging.”

FT 3/3 2007

Remarks by Chairman Ben S. Bernanke

Globalization and Monetary Policy

March 2, 2007

Carry Trade

Top of page

The People's Bank of China (PBOC), the nation's central bank, is capable and well-respected around the world.

However, monetary policy can work well only to the extent that financial markets are sufficiently developed to allow the monetary authorities' interest-rate decisions to affect economic activity in a reasonably predictable way.

Chairman Ben S. Bernanke, Chinese Academy of Social Sciences, 15/12 2006

Last week’s announcement that Frederic Mishkin will join the Federal Reserve Board chaired by Ben Bernanke marks a turning point in US monetary policy.

Stephen Cecchetti, FT July 10 2006

Together, Messrs Bernanke and Mishkin have provided much of the intellectual foundation for a monetary policy framework called “inflation targeting”. Begun in New Zealand nearly 20 years ago, and now used in two dozen countries, including Australia and Mexico, this bypasses intermediate targets and focuses directly on the objective of low inflation.

Full text

Stephen G. Cecchetti

Frederic Mishkin

Comment by Rolf Englund:

"bypasses intermediate targets" means abandoning for example money supply, to the horror of us remaining monetarists.

More about monetarism

Top of page

Bernanke’s Sophie's Choice:

"The housing market or stock market Mr. Bernanke.

You may only be able to try and save one..."

Bernanke’s Fed, well aware that foreign central banks are questioning US dollar hegemony at a time when precious metals are capturing some safe haven flows, needs to ensure that three things happen:

1) The US dollar declines in an orderly manner.

2) US and global asset prices decline in an orderly manner (or preferably flatline) as speculative excesses in commodities, real estate, and emerging markets are expunged.

3) US companies start spending more of their cash hoard under the misplaced notion that the economy will continue down the goldilocks path.

Brady Willett, May 18, 2006

I am not so sure that the Fed can accomplish all of these things if the US consumer seriously curtails their spending habits. In fact, I am not so sure they can accomplish any of these things if the US consumer curtails their spending habits. And here is the rub: If no major asset price is going up the US consumer will curtail their spending habits.

Full text

US Dollar

Moral Hazard

PPT

Sophie's Choice

Top of page

Bernanke told a seminar on Capitol Hill:

"On average, debt burdens appear to be at manageable levels and delinquency rates on consumer loans and home mortgages have been low"

Michael Shedlock 15/6 2006

Bernanke never checks into my blog to answer questions but I have several anyway.

Since when do asset bubbles in houses or stocks justify piling on debt?

Given that real wages are falling and debt payments are the second highest in history, on what basis do you find "U.S. households overall have been managing their personal finances well".

Which direction are bankruptcies and foreclosures headed?

Full text

Top of page

Monetary policy is decision-making under uncertainty. Central bankers do not disagree about the benefit of price stability.

They differ on how much insurance they are prepared to pay to protect themselves against failure to meet the target.

Wolfgang Munchau, Financial Times 22/5 2006

Unlike some of his European counterparts, Mr Bernanke does not believe that central banks should care about financial bubbles. And unlike his European counterparts, he does not talk publicly about the need to counter the rise in inflation at this time. The outcome of the Fed’s June policy meeting is wide open, while the ECB left no doubt that it would raise interest rates next month. Hardly a day passes without some ECB official warning about the risks of inflation. Mr Bernanke may ultimately be proved right to be cautious at this point. But relative to other central bankers in the world, he appears dovish.

So what happens if the Fed lets inflation slip a little and if the ECB does not? The most likely consequence is a further fall in the dollar against the euro. I am aware that predictions of an imminent fall in the dollar have often proved mistaken in the past. I will not make that prediction now, except to say that the dollar is still fundamentally and substantially overvalued.

The resurgence of global inflation is an important issue not because the inflationary pressures in the US and Europe themselves are extreme – in fact, they are moderate if compared with inflationary pressures of the 1970s. They are important because even moderate inflation, if combined with the wrong policy response, could cause extreme volatility and instability in financial markets and the world economy.

Full text

Top of page

Mr Bernanke belongs to a generation of economists whose schooling has cultivated a taste for rules – fixed, hence predictable, and mechanical, hence transparent.

Edmund Phelps, Financial Times, 25/4 2006

Reflections on the Yield Curve and Monetary Policy

Since June 30, 2004, the overnight interest rate has moved up 3-1/2 percentage points, but the ten-year nominal Treasury yield has only edged higher. At less than 4-3/4 percent, that yield is not much above the target federal funds rate of 4-1/2 percent

Chairman Ben S. Bernanke 20/3 2006

Top of page

Many people may not know the name Ben Bernanke.

The huge trade deficit, with its flood of cheap goods, has helped to keep inflation in check. So eventually, the adjustment to the trade gap could involve both a slowdown in consumer spending and at the same time increased pressure on prices

BBC 2/1 2006

Dollar

The market emphatically interpreted this as a signal that the Fed was opening the door to the possibility of interest rate cuts.

Within an hour of the statement, the dollar had slipped to its lowest level against the euro in two years.

The S&P 500 closed up 1.7 per cent, while the yield on two-year Treasury bonds fell 8 basis points.

Financial Times 22/3 2007

That opens the way to quick rate cuts if economic growth falters further in the face of continued housing weakness.

But such excitement relies on inflation also behaving itself. The real danger, as the Fed highlights, is that it “fails to moderate as expected”. That could leave the central bank caught between slowing growth and stubbornly high inflation.

Comment by Rolf Englund

That is what central bankers are paid for.

Dollar

Bernanke’s Sophie's Choice

Let's look at what Bernanke really said

Deflation: Making Sure "It" Doesn't Happen Here

Top of page

Will Bernanke Create Hyperinflation?

What are the lessons from the Great Depression, from stagflation in the 1970s, from deflation in Japan? The bubbles that preceded these challenging times should never have been allowed to happen.

Axel Merk, Manager of the Merk Hard Currency Fund 15/12 2005

What are the lessons from the Great Depression, from stagflation in the 1970s, from deflation in Japan? The bubbles that preceded these challenging times should never have been allowed to happen. Yet even today, the Federal Reserve Bank (Fed) is very reluctant to pop bubbles. Greenspan talked about irrational exuberance in the stock markets, but let the stock market rise to the stratosphere in the late ‘90s; he has also kept interest rates low for an extended period despite mounting consumer debt and steep home price appreciation.

Richard Koo, author of ‘The Balance Sheet Recession’, says massive government spending must take the place of corporate spending to keep an economy afloat when corporations do not invest and consumers do not spend.

He rejects the notion that such companies should be allowed to fail when the problem is systemic such that 95% of banks have a negative net worth and there would not be any buyers in the ensuing shakeout. Consequently, the economy would potentially suffer a meltdown.

Full text

Top

Greg Ip, Fed stenographer (née Wall Street Journal reporter), penned a story titled

"Long Study of Great Depression Has Shaped Bernanke's Views."

Bernanke has no comprehension of the fact that booms and busts are related.

Bill Fleckenstein, CNBC 12/12 2005

To a degree - honest people can argue how much - booms cause busts. They don't just precede them. Booms derange prices and therefore misdirect investment.

"By manipulating the funds rate, says the Maestro-designate, the Fed can fine-tune the measured rate of inflation, promote full employment and assure financial stability. For Bernanke, booms have nothing to do with busts. The common-sense theorists of the so-called Austrian School (including Friedrich Hayek and Ludwig von Mises) might as well never have been born.

Full text

"The continuous injection of additional amounts of money at points of the economic system where it creates a temporary demand, which must cease when the increase of money stops or slows down, together with the expectation of a continuing rise in prices, draws labor and other resources into employments which can last only so long as the increase of the quantity of money continues at the same rate--or perhaps even only so long as it continues to accelerate at a given rate . . . would rapidly lead to a disorganization of all economic activity."

F. A. Hayek

Top

Bernanke should rethink his monetary ‘Maginot Line’

At first glance, it is hard to see why the incoming Fed governor feels the need to install an inflation-targeting regime.

Peter Hartcher, Financial Times 22/11 2005

The writer, author of Bubble Man: Alan Greenspan and the Missing Seven Trillion Dollars (Black Inc, Australia, and from April, WW Norton in the US) is international editor of The Sydney Morning Herald

It is hard to see why Mr Bernanke is devoting all his initial political capital to this issue. Perhaps, like the Maginot Line, it is all about the last war. Inflation peaked in the US in 1982, under Paul Volcker, Mr Greenspan’s predecessor. It is today well in check and although the gold price has been rising in recent days, the yield on 10-year US Treasury bonds has been falling. This is hardly a market panicked by the prospect of inflation.

The experience of Japan in the 1980s, and the US in the 1990s until today, is that easy money no longer flows into traditional inflation, but into asset price inflation. While consumer price inflation stayed low, America blew up its economy with vast speculative asset price bubbles. After watching the US stockmarket bubble burst and drag the economy into recession, other central bankers around the world showed intellectual flexibility in trying to figure bubbles into their thinking.

The Bank for International Settlements published papers suggesting a rethink on the question and other central banks around the world – including those of Britain, Australia, Canada, New Zealand and Norway – started publicly addressing the question of how to deal appropriately with bubbles.

The US central bank, under Mr Greenspan and, shortly, Mr Bernanke, avoids focusing on it. The enemy has reformed, but the Fed’s threat perception has not. In the meantime, the US has gone from one bubble – in stock prices – to another, in house prices. Right now, the housing bubble is starting to deflate. This is because the Fed is raising short-term rates, bringing them back to a neutral position

It just so happens that this tightening to head off any inflationary threat coincides with the need to deflate a potentially dangerous bubble in house prices.

Full text