The Myth Of the Rational Market

Martin Wolf about The End Game

Finanskrisen -

The Great Recession

Home - Index - News - Krisen 1992 - EMU - Deflation.com - Economics - Cataclysm - Rebalancing - US Dollar - Houseprices - Contact

Stabiliseringspolitik

Ernst Wigforss ”Har vi råd att arbeta?”

Grundbultsfrågan: Hur blir S = I ???

Savings and investment, being different activities carried on by different people

Man återkommer ständigt till Keynes och Hayek. Har den ekonomiska "vetenskapen" inte kommit längre?

Rolf Englund blog 8 juli 2014

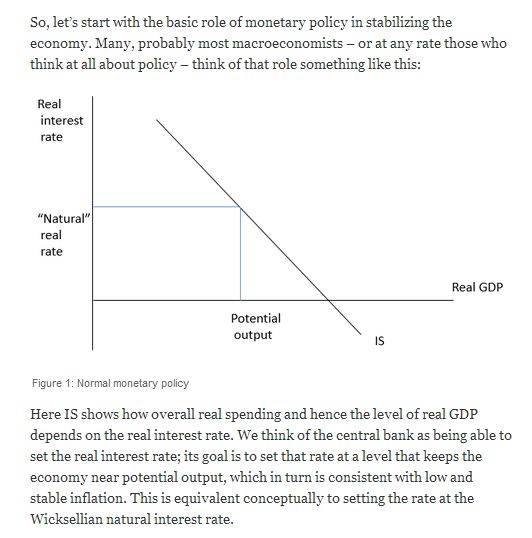

Varoufakis: A balanced capitalist economy requires a magic number, in the form of the prevailing real (inflation-adjusted) interest rate.

How do free marketeers convince themselves that there exists a single real interest rate (say, 2%)

that would inspire investors to funnel all existing savings into productive investments

and spur employers to hire everyone who wishes to work at the prevailing wage?

Yanis Varoufakis Project Syndicate 19 March 2019

The idea of secular stagnation is that the private economy — unless stimulated by extraordinary public actions especially monetary and fiscal policies

and, or, unsustainable private sector borrowing — will be prone to sluggish growth caused by insufficient demand.

Lawrence H. Summers, FT 6 May 2018

Själv brukar jag med en dåres envishet upprepa följande ord, första gången den 5 december 2009

Jag tycker det är skriande uppenbart att räntan världen över är för låg och att en större del av stimulanserna borde ske via finanspolitiken.

Men väljarna och därmed deras medlöpande politiker är rädda för budgetunderskott och vill hellre att villaägarna skall låna än att staten skall göra det.

Why is macroeconomics so hard to teach?

That requires an intuitive feel for the subject. It is not enough to crank through the equations.

The Economist 9 August 2018

China has avoided a recession for a quarter-century

Macroeconomists should think about credit policy as an important supplement

to the traditional fiscal and monetary tools of recession-fighting.

Noah Smith 19 July 2018

Rethinking macroeconomics

In January 2018, a group of economists convened by Oxford published

their reply to Queen Elizabeth’s question of why nobody in the profession saw the 2008 crisis coming

FT Collections

The Phillips Curve is right at the centre of the most important economic debate of the moment

John Authers FT 16 March 2018

Markets are back in fairyland again.

For many investors, the regret of missing out on what may well be a once-in-a-generation bull market

overshadows any anxiety about the next crash. Animal spirits are all too evident.

Amin Rajan FT 16 March 2018

---

What Robert Shiller, a Nobel economics laureate at Yale University, calls “narrative economics”

Neither central bankers nor Wall Street ever see these new style recessions coming because, in fact,

they can't be detected from even an astute reading of the macro-economic tea-leaves.

David Stockman 9 March 2018

Self-evidently, that's because the triggers for recession are embedded in the interstitial bubbles of the financial markets;

and while the latter may be obvious to the outsider or even a visiting Martian,

they are adamantly denied by the Wall Street stock peddling apparatus and are invisible to the Fed's financially clueless Keynesian academics and policy apparatchiks

who remain glued to their macroeconomic dashboards.

---

What Event Will Sink the Stock Market? Yields? Tariffs? Trump?

The catalyst is "sentiment" not an event.

Mike Mish Shedlock 15 March 2018

When the economy’s human and capital resources are fully utilized (meaning actual GDP is equal to potential GDP), fiscal stimulus just generates inflation and higher interest rates. Even if the extra demand might create some wage pressure, it will be met with higher inflation, so real wages – the paycheck’s actual buying power – won’t change at all.

The problem is that those making that argument are implicitly asserting that they know that the “natural rate of unemployment” – the lowest rate consistent with stable inflation – is roughly equal to the current unemployment rate. That is, they believe we’re at full employment. But the truth is they have no way of knowing that, and one key indicator – inflation – suggests they may be wrong.

Jared Bernstein, chief economist for Vice President Joe Biden, at John Mauldin 18 February 2018

NAIRU: not just bad economics, now also bad politics

Janet Yellen has long believed it’s possible for “too many” Americans to have jobs. In her view,

shared by many of her generation in the economics profession,

consumer prices will rise too fast unless millions of people remain unemployed.

Matthew C Klein, FT Alphaville 24 January 2018

What macroeconomists actually do

Problems can be traced back to two intellectual revolutions

Martin Sandbu 16 January 2018

Rethinking macroeconomics

The deepest effort to date to account for how economics failed us in the crisis

Martin Sandbu 15 January 2018

The very toxin that sparked the crisis is relied on to reboot economies in the Americas and Europe.

Pascal Blanque and Amin Rajan, FT 4 January 2017

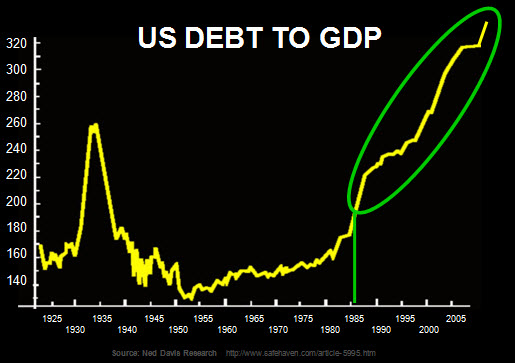

Global debt is like the sword of Damocles — an ever-present danger. It stands at about 330 per cent of annual economic output, up from 225 per cent in 2008

Central banks need to reverse their policies, since continuing low rates and excessive leverage may well result in an explosive cocktail of multiple asset price bubbles.

Reversal, however, means that central banks will be unable to control volatility and keep a floor under asset values — something they have relied on to promote excessive risk-taking.

Olivier Blanchard and Lawrence H. Summers

Rethinking Macroeconomic Policy

“We’ve learned over the past 10 years that fiscal policy can have pretty powerful effects

in deep recessions when central banks have hit very low policy interest rates,”

Gemma Tetlow, FT 13 November 2017

There was broad agreement in 2008 and into 2009 that borrowing should be allowed to rise to cushion the impact of the financial crisis. But by 2010, with growth returning, policymakers were keen that it should be scaled back to reassure markets that government debt would not get out of hand, and so head off a sharp rise in borrowing costs.

Many economists agreed, but their views have since shifted.

“We’ve learned over the past 10 years that fiscal policy can have pretty powerful effects in deep recessions when central banks have hit very low policy interest rates,” says Alan Auerbach, professor of economics at Berkeley. “We’ve also learnt, at least from the experience in the UK and the US, that we would have benefited from... turning less immediately to measures aimed at deficit reduction.”

Under these circumstances, there is a strong case for loosening fiscal policy and borrowing more. This is especially true for policies that put money directly into the hands of people who will spend it quickly and counteract sluggish demand, and for investments that have long-term benefits.

“Economies do not self-stabilise,” said Olivier Blanchard, at a conference on macroeconomic policy, on lessons of the

financial crisis for monetary and fiscal policy.

Rethinking Macroeconomic Policy, Conference Coordinators: Olivier Blanchard and Lawrence H. Summers.

Central banking is hard. But the Federal Reserve Bank of San Francisco makes it look easy.

Matthew C Klein, FT Alphaville 30/10 2017

They have a game called “Chair the Fed” where you get to set the level of short-term interest rates once every three months.

(The European Central Bank has its own game, which we once wrote about, that was similarly limited but also more fun thanks to the colourful characters.)

Basil Fawlty’s “Don’t mention the war!” has given way to something nasty:

non-German macroeconomists over the euro and global reflation — with epithets like “ordo-liberal” and worse flying around.

Former IMF staffer Peter Doyle, FT Alphaville 17 October 2017

Central bankers have one job and they don’t know how to do it

Matthew C Klein, FT Alphaville 18 Octobr 2017

World’s top economists worry about tools to fight economic downturn

The question is whether there are enough weapons to fight the next crisis when it comes

FT 13 October 2017

With interest rate cuts unlikely to be sufficiently effective in another downturn because they will not start high enough, Mr Blanchard and Lawrence Summers, the former treasury secretary, advocated much more effective and planned use of fiscal policy.

In a joint presentation, they called for governments to put in place plans for aggressive fiscal stimulus in the event of a downturn.

Central bankers face a crisis of confidence as models fail

inflation is not behaving in the way economic models predicted

FT 11 October 2017

Fed has no reliable theory of inflation, says Former Fed governor Tarullo

FT 4 October 2017

Politicians are kept from taking full responsibility for battling recessions by the intellectual baggage of past decades.

Some cling to the notion that stimulus is unhelpful, risky and hard. Such views need updating.

The Economist, 7 September 2017

Economists of all stripes argued that the “multiplier” on stimulus—the amount by which a dollar of borrowing raises GDP—is usually low. Households save their higher incomes in expectation of offsetting future tax rises

But studies since the Great Recession tend to find that multipliers are substantially higher than once thought, particularly when monetary policy is constrained. Multipliers in such cases are often closer to two, ie, GDP increases by nearly twice the size of the stimulus.

This article appeared in the Finance and economics section of the print edition of under the headline "The borrowers"

About The Multiplier at my blog

One of the inescapable truths of the past 10 years is that

the central bank policies introduced to mitigate the crisis may be sowing the seeds of another one.

As in the run-up to 2007, ultra-low interest rates have been distorting the world’s finances.

Patrick Jenkins, FT’s financial editor, 31 August 2017

Western capitalism has few sacred cows left.

It is time to question one of them: the independence of central banks from elected governments.

Yanis Varoufakis, Project Syndicate 29 August 2017

Perhaps the macro question – is why low unemployment isn’t sparking higher inflation

as the fabled Phillips curve says it should.

John Mauldin, 2 September 2017

Real interest rates aren’t particularly low

FT Alphaville 17 August 2017

Why there was no New Deal after the Great Recession

Since the financial crisis there has been a lack of boldness in thought, as well as action

Martin Sandbu, FT 24 July 2017

Tillväxten steg och arbetslösheten föll. Men det kom även bakslag, som 1937

när Roosevelt tvingade skära i bidragen för att minska statsskulden som ökat kraftigt och

man lyckades aldrig riktigt ta sig ur depressionen.

Det var egentligen Hitler som lyckades få fart på den amerikanska ekonomin igen.

Therese Larsson Hultin, SvD 6 juli 2017

Yet today, I have come around to the idea that the debt problem is so pervasive, there is only way one forward - inflate.

We are going to end up there anyway, so let’s just inflate away the burden and restart with a system that prevents this from ever happening again.

Kevin Muir via The Macro Tourist blog, zerohedge, 7 April 2017

The US president signed an executive order on Friday 2017-03-31

calling for a 90-day country-by-country and product-by-product

study of the US’s $500bn annual trade deficit.

FT 31 March 2017

But anyway, in macro, most models use Rational Expectations,

so let's think of "behavioral" as just meaning "non-RE".

I'm seeing macro people taking behavioral ideas more seriously.

Noahpinion 15 January 2017

The orthodox view is that the US can always achieve full employment by active use of fiscal and monetary policy tools.

Experience since 2000 and especially since the financial crisis suggests this may be difficult.

As I have argued elsewhere, huge current account surpluses in some countries forced deficit countries into financial excesses

as an (ultimately unsustainable) way to maintain demand in line with potential output.

Martin Wolf, FT 31 January 2017

The new defense of DSGE

It's so silly that I almost suspect Christiano et al. of staging a false-flag operation to get more people to hate DSGE modelers.

Noah Smith 15 November 2017

The burden of proof is on the DSGE-makers, not on the critics. Christiano et al. should look around and realize that people outside their small circle of the world aren't buying it.

Dynamic stochastic general equilibrium modeling (abbreviated DSGE or sometimes SDGE or DGE) is a branch of applied general equilibrium theory that is influential in contemporary macroeconomics.

Wikipedia

The Need for Different Classes of Macroeconomic Models

This is is my third piece on dynamic stochastic general equilibrium models (DSGEs)

Olivier Blanchard (PIIE) January 12, 2017

The first, a PIIE Policy Brief, was triggered by a project, led by David Vines, to assess how DSGEs had performed during the financial crisis (namely, badly) and how they could be improved.

That brief went nearly viral (by the standards of blogs on DSGEs).

Robert Shiller presidential address to the American Economic Association

It was something out of the usual — as we should expect from as fertile, contrarian and original thinker as Shiller

— namely a plea for economists to take seriously the importance of “narrative epidemics”.

Martin Sandbbu, FT 12 January 2017

Although lots of jobs were created in the impressive recovery from the dark days of the global financial crisis,

other elements of the labor market did not respond as would be expected based on historical experience.

Mohamed A. El-Erian, Bloomberg 4 January 2017

Wage growth has remained rather anemic, even in the context of indicators of labor shortages.

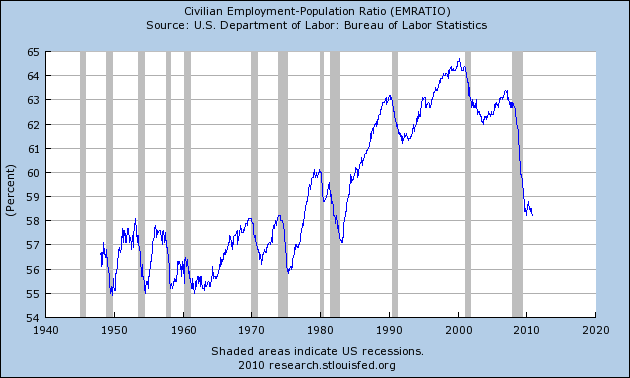

In addition, the labor participation rate, at 62.7 percent in November 2016, has failed to bounce back from multidecade lows,

while the employment-to-population rate seems stuck at a rather low level of 59.7 percent.

Cyclical factors, including an unbalanced macroeconomic policy stance that has relied excessively and for too long on unconventional monetary measures and made insufficient use of fiscal policy, have played a role.

The inability of the world’s major central banks to create either inflation or stronger demand growth

has sustained a needed debate over whether the way monetary policy is conducted in most rich countries is ripe for reform.

Martin Sandbu, FT 4 January 2017

The main argument for a higher inflation target was put forward by Olivier Blanchard and his colleagues in 2010:

a higher inflation target makes it easier to cut real (inflation-adjusted) rates deeper still should the economy require it.

Since then, a higher inflation target has won steadily more adherents.

Under inflation targeting, a central bank is only committed to bring inflation back to the 2-per cent rate.

Under level targeting, it is committed to bringing the level of prices or NGDP back to the desired trend

The Case For Higher Inflation

Olivier Blanchard, currently the chief economist at the IMF,

conclusion, central banks have been setting their inflation targets too low

I’m not that surprised that Olivier should think that;

I am, however, somewhat surprised that the IMF is letting him say that under its auspices. In any case, I very much agree.

Paul Krugman, Febr 13 2010

An Extraordinary Time: The End of the Postwar Boom and the Return of the Ordinary Economy

Book by Marc Levinson, formerly finance and economics editor of The Economist

The fiscal theory of the price level (FTPL), a macroeconomic doctrine that has lately been receiving considerable attention.

In August, at the annual conference of central bankers in Jackson Hole, Wyoming, Princeton’s Christopher Sims provided a lucid explanation of the theory.

Koichi Hamada, Special Economic Adviser to Japanese Prime Minister Shinzo Abe, Project Syndicate, 28 December 2016

Sims explained, contrary to popular belief, aggregate demand and the price level (inflation) are not dictated only – or even primarily – by monetary policy.

kansascityfed.org/~/media/files/publicat/sympos/2016/econsymposium-sims-paper.pdf?la=en

The most far reaching speech at the Federal Reserve’s Jackson Hole meeting

was the contribution on the fiscal theory of the price level (FTPL) by Professor Christopher Sims

Gavyn Davies, FT 29 Auggust 2016

The low-for-long era is over.

This summer, the BoJ and then the ECB both changed their mantra

from whatever it takes to less is more targeting steeper yield curves

and the transmission mechanism of stimulus to the real economy, moving away from unlimited asset purchases.

Alberto Gallo, FT 27 December 2016

Today’s young Wall Street hotshots have never seen anything like that.

To them the jump from 0.5% to 0.75% must seem like a big deal.

It’s really not.

I would start with a fundamental reappraisal of modern macroeconomic governance

— from independent central banks and inflation targeting to deregulated financial markets and fiscal policy targets.

Put simply, if we, the liberal establishment, fail to do this, the populists will do it for us.

Wolfgang Münchau, FT 18 December 2016

Much of what we today think of as normal was established quite recently.

Central banks were not always independent. Direct inflation targeting is common today, but was unknown before the 1990s.

These observations are mild compared with those of Paul Romer, chief economist of the World Bank,

who has written a devastating critique of his profession, comparing it with string theory in physics.

The latter was once criticised by well-known physicists as “not even wrong”.

Mr Romer portrays modern macroeconomics as a racket held together by people who protect their influence

The state of Economics as a science

Era of quantitative easing is drawing to a close

arguably the greatest monetary policy experiment since John Law began dabbling with fiat paper money in France

Robin Wigglesworth, FT 8 December 2016

...

Not a credit crunch yet, but the ground is shifting

Short-term interest rates are the tectonic plates of financial markets.

They move slowly but have a nasty tendency to reveal buildings built on flimsy foundations.

Robin Wigglesworth 8 August 2018

Mr Mnuchin plans that would restore the status of the Treasury department as the vital driver of economic policy.

For those who can remember the pre-crisis era, it felt like a throwback to heavyweight predecessors such as

Robert Rubin, Lawrence Summers and James Baker III.

FT 1 December 2016

Robert Rubin, Lawrence Summers and James Baker III

Treasury Secretary Henry Paulson

John Connally, Nixon’s secretary of the Treasury, famously told the Europeans that

the dollar “is our currency, but your problem”.

On November 22, 1963, he was seriously wounded while riding in President Kennedy's car in Dallas, when the president was assassinated. Connally does not endorse the conclusions of the Warren Commission. When asked if he believed the Warren Commission's findings he said: "Absolutely not.

I do not, for one second, believe the conclusions of the Warren Commission."

Martin Sandbu/Brad DeLong four serious diagnoses of the ills of the Global North.

FT 4 November 2016

They are: A Bernanke global savings-glut.

A Krugman-Blanchard return to ‘depression economics’.

A Rogoffian-Minskyite crisis of overleverage and debt overhang.

A Summers secular-stagnation chronic crisis.

DeLong points out that each leads to different policy recommendations

Monetary policy in a low-rate world

Martin Wolf, FT 13 Sepptember 2016

Some of the greatest cheerleaders for fiscal tightening a few years back are undergoing a Damascene conversion

that is something to behold.

Martin Sandbu FT 30 November 2016

In its latest Economic Outlook, the OECD gives a thumbs-up to Donald Trump’s plans(if that is what they are)

to enact a large fiscal stimulus and increase infrastructure spending

When the dust settled, I was left with a profound sense of sadness over

our global economic leadership’s obvious lack of understanding of the real world.

John Mauldin, 4 September 2016

The rich world’s central banks need a new target

Advantages in targeting the level of nominal GDP

The Economist 27 August 2016

Quantitative easing's failure to quash the threat of deflation

is finance's equivalent of the bump in the data that alerted physicists

to the possibility of a new boson.

Mark Gilbert Bloomberg 18 August 2016

John Williams, the president of the Federal Reserve Bank of San Francisco:

Central banks need to consider aiming for a higher inflation target

FT 15 August 2016

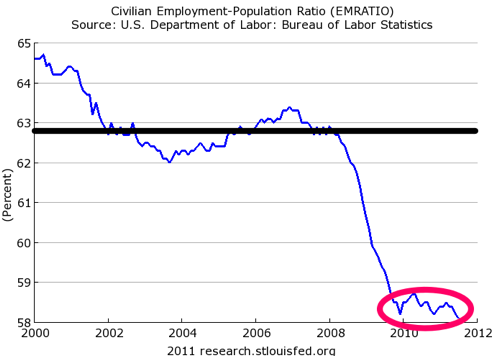

Even if unemployment — the share of workers who say they want a job but can’t find one — is low,

the share of the prime-age (25-54-year-old) population in work is only 78 per cent.

That is two percentage points below the 2007 rate, and four percentage points

— some 5m missing jobs — below the 2000 peak.

Martin Sandbu 8 August 2016

In 2013 economists at the IMF rendered their verdict on these austerity programmes:

they had done far more economic damage than had been initially predicted, including by the fund itself.

What had the IMF got wrong when it made its earlier, more sanguine forecasts?

It had dramatically underestimated the fiscal multiplier.

The Economist print 13 August 2016

Highly Recommended

We are all Keynesians now, so let's get fiscal

Monetary policy is close to the limits.

Ambrose Evans-Pritchard 4 August 2016

In his latest just released monthly letter, Bill Gross lays out the global economy as an analogy to Monopoly

where the narrative only works if everyone gets $200 in cash on every rotation around the board.

It’s the $200 of cash (which in the economic scheme of things represents new “credit”) that is responsible for the ongoing health of our finance-based economy.

Without new credit, economic growth moves in reverse and individual player “bankruptcies” become more probable.

And without banks creating new loans and injecting money into the broader economy, economic activity grinds to a halt.

The Brave New Uncertainty of Mervyn King

Paul Krugman, The New York Review of Books, Issue 14 July 2016

As a biographer and aficionado of John Maynard Keynes, I am sometimes asked:

“What would Keynes think about negative interest rates?”

Robert Skidelsky, Project Syndicate 24 May 2016

Monetary policy is not exhausted, and active use of it is essential.

But undue reliance on monetary policy is problematic.

Martin Wolf, FT 25 May 2016

Atlanta Fed's gauge of "sticky-price" inflation in the US

soared to a post-Lehman peak of 3 pc

Ambrose 2016-03-16

The subprime crisis, the euro crisis, the China slowdown, the oil bust.

But surely these events are connected.

Justin Fox, Bloomberg View 10 March 2016

I’m confident we would see improvement on all fronts

if we got GDP growth back up to 4% for a few years.

John Mauldin, March 7, 2016

Keynes’s General Theory at 80

First, Keynes invented macroeconomics – the theory of output as a whole.

Keynes’s second major legacy is the notion that governments can and should prevent depressions.

Milton Friedman reasserted the pre-Keynesian view of how market economies work.

Inflation, Friedman said, resulted from attempts by Keynesian governments to force down unemployment below its “natural” rate.

Robert Skidelsky, Project Syndicate 23 Febr 2016

The global financial crisis of 2008 bears this out.

The collapse discredited the more extreme version of the optimally self-adjusting economy;

but it did not restore the prestige of the Keynesian approach.

An even bigger shock to the pre-2008 orthodoxy than the collapse itself was the revelation of the corrupt power of the financial system

and the extent to which post-crash governments had allowed their policies to be scripted by the bankers.

To control financial markets in the interests of full employment and social justice lies squarely in the Keynesian tradition.

Students of economics eager to escape from the skeletal world of optimizing agents into one of fully-rounded humans,

set in their histories, cultures, and institutions will find Keynes’s economics inherently sympathetic.

Keynes’s magnum opus, The General Theory of Employment, Interest and Money, published in February 1936

Robert Skidelsky, Professor Emeritus of Political Economy at Warwick University and a fellow of the British Academy in history and economics, is a member of the British House of Lords

Martin Wolf: Helicopter drops might not be far away

FT 23 Febr 2016

Faced with the most severe economic downturn since the Great Depression, the U.S. Federal Reserve did the only thing it could: flood the financial system with liquidity.

The move to so-called easy money arguably saved the world from a worse fate and radically changed the economic backdrop as well as the landscape for financial markets.

Bloomberg via englundmacro.blogspot.se/2016/02/these-are-things-that-correlate

Today’s politicians and central bankers are fixated with fiscal targets and debt reduction.

As in the early 1930s, policy orthodoxy has pathological qualities.

Whenever they run out of things to say, today’s central bankers refer to “structural reforms”,

although they never say what precisely such reforms would achieve.

Wolfgang Münchau, FT 7 February 2016

- Visst beror dagens problem i ekonomin i någon mån på missgrepp i slutet av 80-talet och början av 90-talet.

Men i grunden har Sverige inte hamnat i en stabiliseringspolitisk kris.

Underskottet i statsbudgeten beror djupare sett på att vi försöker överbrygga en konjunkturnedgång

när det i själva verket handlar om en grundläggande strukturell förändring.

Mats Svegfors, Sv D 1994-09-10

Caruana and Greenspan about stocks and shocks

Rolf Englund blog 6 Febr 2016

Martin Wolf:

What might central banks do if the next recession hit while interest rates were still far below pre-2008 levels?

FT February 2016

Since we commonly understand why lowering interest rates stimulates debt and economic growth,

and less commonly understand how QE works, I’d like to explain it.

Ray Dalio, founder and head of hedge fund group Bridgewater, FT 25 January 2015

David Stockman On CNBC:

This Is A Dead Cat Bounce—-We’re At Peak Debt Headed For Recession

via Rolf Englund blog 2016-01-23

ZIRP and QE were terrible mistakes

Rolf Englund blog 4 January 2016

Solid growth is harder than blowing bubbles

The world economy has lost its last significant credit-fuelled engine of demand - China.

The result is almost certain to be a further boost to the global “savings glut” or, as Lawrence Summers calls it, “secular stagnation” — the tendency for demand to be weak relative to potential supply.

Martin Wolf, FT October 13, 2015

The Return of the Original Phillips curve?

Why Lars E O Svensson’s Critiq ue of the Riksbank’s Inflation Targeting is Misleading

Fredrik Andersson and Lars Jonung, June 2015

Some people never learn. They follow the same path that destroyed their finances in the past.

Wall Street is desperately packaging the increasing amounts of subprime slime in new derivatives of mass destruction and peddling them to clients, while shorting those same derivatives.

It’s called the Goldman Sachs method. When home prices begin to tumble, these derivatives will self-destruct again.

What is happening today is nothing more than rearranging the deck chairs on the Titanic.

zerohedge 25 September 2015

Why the Fed Buried Monetarism

Friedman’s “natural” rate was replaced with the less value-laden and more erudite-sounding “non-accelerating inflation rate of unemployment” (NAIRU).

Central bankers now seem to be implicitly (and perhaps even unconsciously) returning to pre-monetarist views:

tradeoffs between inflation and unemployment are real and can last for many years.

Anatole Kaletsky; Project Syndicate, 22 September 2015

The case for keeping US interest rates low

After nearly seven years of zero interest rates, the inflation of which critics warned is invisible

Martin Wolf, FT September 8, 2015

Arguably the most consequential question about today’s economic situation

— though one not asked with anywhere near enough urgency —

is why capital investment is not responding more forcefully to interest rates that in some places are at their lowest level in recorded history.

Martin Sandbu, FT Free Lunch, 26 August 2015

Noah Smith has picked up on the curious pattern as has Brad DeLong before him.

In short: companies can borrow at very low rates and that is also true for real (inflation-adjusted) borrowing costs.

But the return on invested capital — how much a new factory, equipment or business building boost profit relative to the amount it cost to build them — suggests business investment is as profitable as it has always been

Unpredictable does not mean unexplainable

Free Lunch is sceptical of anyone’s ability to “explain” financial market reversals.

Martin Sandbu, FT 24 August 2015

Andreas Cervenka om Stephen Williamson

Världsekonomins medicin sedan 2008 fungerar inte

Augusti 2015

Stephen Williamson, ekonom och chef på den amerikanska centralbanken Federal Reserves filial i St Louis, har gjort en genomgång av de åtgärder som Fed bedrivit sedan finanskrisen bröt ut på allvar 2008: nollränta och massiva stödköp av olika tillgångar med hjälp av nytryckta pengar.

Stephen Williamsons slutsats är att politiken misslyckats: den har inte fått upp inflationen och bevisen för att stödköpen blåst liv i ekonomin är i bästa fall svaga.

Eftersom vi talar om den strategi som dominerat hela världsekonomin sedan finanskrisen är det här lite tråkiga nyheter.

Stephen Williamson: New Monetarist Economics

http://newmonetarism.blogspot.se/

https://research.stlouisfed.org/econ/williamson/sel/

Stephen Williamson’s “New Monetarism” = F. A. Hayek’s Monetary Economics in a New Bottle with a New Label

- See more at: http://hayekcenter.org/?p=5262#sthash.8hHgMTjx.dpuf

What Hayek Can Teach Us About the Nature of Science, Argument, Economics and Knowledge -

See more at: http://hayekcenter.org/#sthash.opMeNi3F.dpuf

Debt Is Good

Paul Krugman, 21 August 2015

Rand Paul said something funny the other day. No, really — although of course it wasn’t intentional.

On his Twitter account he decried the irresponsibility of American fiscal policy, declaring, “The last time the United States was debt free was 1835.”

Wags quickly noted that the U.S. economy has, on the whole, done pretty well these past 180 years,

suggesting that having the government owe the private sector money might not be all that bad a thing.

The British government, by the way, has been in debt for more than three centuries,

an era spanning the Industrial Revolution, victory over Napoleon, and more.

I know that may sound crazy. After all, we’ve spent much of the past five or six years in a state of fiscal panic, with all the Very Serious People declaring that we must slash deficits and reduce debt now now now or we’ll turn into Greece, Greece I tell you.

Syntesen av Hayek, Friedman och Keynes,

mitt storhetsvansinniga och föga framgångsrika projekt

Rolf Englund 7 augusti 2015

Syntesen av Hayek, Friedman och Keynes,

mitt storhetsvansinniga och föga framgångsrika projekt

Rolf Englund 7 augusti 2015

IMF admits: we failed to realise the damage austerity would do to Greece

Guardian, 5 June 2015

Greece needs €60bn in new aid, says IMF

Financaial Times 2 Juky 2015

Monetary policymakers have run out of room to fight the next crisis

with interest rates unable to go lower, the BIS warns

Telegraph 28 June 2015

behavioral economics

The threat was that of a paradigm shift. This term, coined by philosopher Thomas Kuhn, refers to the dread moment

when scientists learn that up is down, black is white and everything they thought they understood about the world is wrong.

Noah Smith Bloomberg 1 June 2015

Simply put, we live in a world in which there is too much supply and too little demand.

The result is persistent disinflationary, if not deflationary, pressure, despite aggressive monetary easing.

Nouirel Roubini, MarketWatch Feb 2, 2015

Alex Stubb, the current prime minister, will be finance minister

in the three-party coalition that is seeking €6bn of additional cuts by 2021.

Finland is mired in a recession that has lasted for much of the past three years.

FT 27 May 2015

Knepet är att trycka nya centralbankspengar som sedan används för att köpa statspapper.

Räntorna pressas, och en viktig effekt är att valutan tappar i värde.

Men åtgärderna är kriminellt senkomna och beslutet tas långt efter både Storbritannien och USA.

OECD understryker att ECB:s sedelpress inte kommer att räcka för att lyfta Europas ekonomier.

DN-ledare 23 januari 2015

Financial Times, 22 January 2015

If investors perceived that the central bank of Italy, for example, were taking on unaffordable risks when buying Italian government bonds,

at that point the price of those bonds would fall, the implicit interest rate paid by the Italian government would rise,

and the whole point of QE would be blown up.

Robert Peston, BBC economics editor, 22 January 2015

Former Federal Reserve Chairman Ben Bernanke believes

history has already vindicated the novel efforts of the U.S. central bank to revive the economy after the financial crisis of 2008.

MarkerWatch 29 December 2014

Federal Reserve is headed down a familiar – and highly dangerous – path.

Steeped in denial of its past mistakes, the Fed is pursuing the same incremental approach

that helped set the stage for the financial crisis of 2008-2009.

The consequences could be similarly catastrophic.

Stephen S. Roach, Project Syndicate,23 December 2014

Why Paul Krugman is wrong

Central banks can always create inflation if they try hard enough

Ambrose Evans-Pritchard, 15 December 2014

Professor Paul Krugman is the world’s most influential commentator on economic issues by a wide margin.

It is a well-deserved ascendancy. He is brilliant, wide-ranging, readable, and the point of his rapier is very sharp.

He correctly predicted and described the Long Slump; though whether he did so entirely for the right reasons is an interesting question.

He demolished claims by hard-money totemists that zero rates and quantitative easing would lead to spiralling inflation in a global liquidity trap, as he calls it – or in a China-led world of excess supply and deficient demand, as others would put it.

So it is disconcerting to find myself on the wrong side of his biting critique.

----

Krugman:

Ambrose Evans-Pritchard, in an otherwise coherent description of Europe’s deflation risk, approvingly quotes Tim Congdon blithely

declaring that monetary reflation in a liquidity trap is no problem:

The interest rate is totally irrelevant. What matters is the quantity of money. Large scale money creation is a very powerful weapon and can always create inflation.

Sure. Just look, in the accompanying chart, at the rate of M1 growth in the US versus the Fed’s preferred measure of inflation

---

Ambrose:

Former Fed chair Ben Bernanke – no fool he – spelled out the powers of a central bank in his prophetic speech on deflation in 2002.

"Sufficient injections of money will ultimately always reverse a deflation.

Under a fiat money system, a government should always be able to generate increased nominal spending and inflation,

even when the short-term nominal interest rate is at zero."

Conundrum

Alan Greenspan couldn’t control long-term interest rates a decade ago,

and bond investors are betting Janet Yellen’s luck will be no better.

Bloomberg, 19 November 2014

Ultimately, economic progress depends on creativity.

That is why fear of “secular stagnation” in today’s advanced economies has many wondering how creativity can be spurred.

One prominent argument lately has been that what is needed most is Keynesian economic stimulus – for example, deficit spending.

After all, people are most creative when they are active, not when they are unemployed.

Robert J. Shiller, a 2013 Nobel laureate in economics, Professor of Economics at Yale University, Project Syndicate 18 november 2014

Germany’s policymakers deny the eurozone’s crisis-ridden countries a more active fiscal policy;

refuse to support a European investment agenda to generate demand and growth;

have declared a fiscal surplus, rather than faster potential growth, as their primary domestic goal;

and have begun turning against the European Central Bank (ECB) in the struggle against deflation and a credit crunch.

On all four counts, Germany is wrong.

Marcel Fratzscher, Project Syndicate 21 November 2014

The Germans have a name for their unique economic framework: ordoliberalism.

Wolfgang Münchau FT 16 November 2014

Finanskriskommittén

Riksgäldens garantiprogram för bankerna infördes 2008.

Sammanlagt ställdes bankgarantier för 354 miljarder kronor.

SvD Näringsliv 18 november 2014

Today’s most important economic illness: chronic demand deficiency syndrome.

David Cameron “red warning lights are once again flashing on the dashboard of the global economy”.

Martin Wolf, Financial Times 18 november 2014

The lights are again flashing red on the dashboard of the world economy, David Cameron warned yesterday.

Just to extend the metaphor, the plane is flying on empty, having pretty much exhausted its fiscal and monetary reserves,

and there is no sign of a safe landing strip in sight.

Jeremy Warner, Telegraph, 18 Nov 2014

The only things that seem to keep us going at all, raising us somewhat above the economic disaster zone of much of the rest of Europe,

are continued very high levels of deficit spending and the parallel stimulus of ultra accommodative monetary policy.

These are the things that truly mark the UK, and the much larger US economy, out from the pack – willingness to mortgage our futures in pursuit of short-term growth,

in the hope that this eventually provides the wherewithal to meet the payments on our growing debt obligations.

If everyone proceeded along these lines together, then perhaps a virtuous circle of growth – and thus declining indebtedness – might be generated.

But to do it alone while all around are engaged in a process of what might be called “competitive deflation” is in the long term completely unsustainable.

It is the economics of the Thirties we seem to be returning to

The US Federal Reserve and other western central banks have failed to anticipate this deflation environment,

persistently undershoot their inflation targets and appear powerless to reverse the trend.

At some point, we will probably wonder if it is time for the anti-deflation baton to pass to governments.

George Magnus, FT December 24, 2014

The writer is a senior independent economic adviser to UBS

Skriande uppenbart - Quantitative Easing

Ordinarily, the role of tax and spending in smoothing economic cycles is to stand back and let monetary policy do the job.

But these are not ordinary times. In the advanced world, weak growth and the threat of deflation have driven monetary policy towards its limit.

In such circumstances, fiscal policy has an important counter-cyclical role.

Financial Times editorial 7 November 2014

Within the rich world, the US recently exited QE3, its third bout of quantitative easing.

It might not have had to go so far had fiscal policy, expansionary immediately after the crisis, not encountered severe congressional dysfunction with fights over the debt ceiling and the fiscal cliff.

Normal times will not resume across the world economy for a while to come. Governments need to grasp the fact that fiscal policies matter for growth and inflation in the short as well as the long run.

Jag tycker det är skriande uppenbart att räntan världen över är för låg och att en större del av stimulanserna borde ske via finanspolitiken.

Det skrev jag på min blogg första gången

Gunnar Hökmark var en gång vänlig mot mig när jag på Timbro beklagade mig över att jag kände mig så ensam.

Är man först är man alltid ensam tröstade han mig med.

Ett annat lika klokt men kanske inte lika vänligt Hökmarskt bon mot var också träffsäkert

"Bara för att man själv förstår något är det inte säkert att andra inte förstår det".

John Maynard Keynes Is the Economist the World Needs Now

Politicians ignored Keynes in 1937. Doing so again could tank the economy

Peter Coy, Businessweek's economics editor, October 30, 2014

Quantitative easing may sown the seeds of the next great markets disaster

those who prophesied that these trillions of dollars of debt purchases would spark uncontrollable inflation have been proved wrong.

But QE could still prove toxic.

Robert Peston, BBC Economics editor, 29 October 2014

If there has been inflation, it has been in asset prices, rather than in items of everyday consumer expenditure.

The market price of the purchased bonds has been increased. And investors who received all those hundreds of billions of dollars from the Fed,

pumped that money into shares and property and even the bonds of other countries, from India to Canada.

QE probably helped prevent the Great Recession being deeper and longer.

But by inflating the price of assets beyond what could be justified by the underlying strength of the economy,

it may sown the seeds of the next great markets disaster.

Should there be another round of QE/helicopters, we must surely find a better way to inject the money.

Today’s method is enriching the uber-elites, with a painfully slow trickledown.

The better alternative is to stick the needle straight into the veins of the economy

- building roads, railways or nuclear power stations.

Ambrose 29 May 2013 with nice pic of Fed

Greenspan said that the Fed’s quantitative easing has failed in one of its goals, to spur demand.

Inflation is “dead in the water” because effective demand is “dead in the water,”

But quantitative easing has been a “terrific success” in getting the real rate of return on long-term assets down,

boosting all income-earning assets.

MarketWatch 29 October 2014

Det är oklart varför målet är just 2 procents inflation, med hur mycket Sverige har missat målet,

och hur stor skada detta eventuellt gjort för sysselsättningen.

Även om samtliga dessa frågetecken skulle rätas ut är det alltjämt tveksamt om riksbanken med sin styrränta kan göra något åt inflationen.

Andreas Bergh, kolumn SvD 3 november 2014

Riksbanken har sänkt räntan till noll.

Jag tycker det är skriande uppenbart att räntan världen över är för låg och

att en större del av stimulanserna borde ske via finanspolitiken.

Rolf Engund blog 28 oktober 2014

Carl-Johan Westholm och Jeffrey D. Sachs: alla investeringar are not equal

Rolf Englund blog 27 oktober 2014

The Greater Depression

First it was the 2007 financial crisis. Then it became the 2008 financial crisis.

Next it was the downturn of 2008-2009. Finally, in mid-2009, it was dubbed the “Great Recession.”

Late 2009, the world breathed a collective a sigh of relief. We would not, it was believed, have to move on to the next label,

which would inevitably contain the dreaded D-word. But...

J. Bradford DeLong, Project Syndicate, 28 august 2014

“secular stagnation”

Why inflation remains best way to avoid stagnation

Tim Harford, FT, August 21, 2014

The talk is of “secular stagnation” – a phrase which could mean two things, neither of them good.

High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. Normally, when an economy slips into recession, the standard response is to cut interest rates. This encourages us to spend, rather than save, giving the economy an immediate boost. Things become more difficult if nominal interest rates are already low.

Lagarde och Englund om deflation och inflation

Prof Sims, who won the Nobel Prize in 2011 for studying "cause and effect in the macroeconomy",

says monetary policy cannot do the trick either once interest rates have dropped to zero.

He dismisses the monetary effects of quantitative easing as trivial.

At best, he says, QE is a bluff intended to show resolve and change psychology.

Ambrose Evans-Pritchard, August 21st, 2014

Christopher Sims – a monetary expert, who now thinks money indicators have been rendered "essentially obsolete" by modern finance – says it may be impossible to reverse deflation in the Western economies by any normal means,

in which case we are in trouble.

Thomas Sargent and Christopher Sims win Nobel prize for economics

Centralbankerna i golfbunkern utan Keynes och ränta

Draghi is running out of legal ways to fix the euro

The ECB should starting buying equities and junk bonds. It should subsidise mortgages and consumer credit....

All these measures would be effective. Most would be illegal.

Wolfgang Münchau, FT 17 August 2014

Mr Draghi’s promise to buy eurozone government debt in the secondary markets,

known by the official name of outright monetary transactions.

This surely helped the bond market to recover, and took the heat out of the eurozone crisis.

But it was at best a partial victory because it made everybody, including the ECB itself, complacent. OMT ended all crisis resolution.

The ECB should starting buying equities and junk bonds. It should subsidise mortgages and consumer credit.

It could fund an investment programme in transport infrastructure, energy networks and scientific research, by buying debt to fund such projects at zero interest rates.

All these measures would be effective. Most would be illegal.

The one thing the central bank can do without any legal problems would be to drop the silly macroeconomic model – known as the Smets-Wouters model, after its authors – on which it has been relying for too long.

“Not without treaty change.”

It’s hard to believe, but almost six years have passed since the fall of Lehman Brothers

The crisis is by no means over. Recovery is far from complete,

and the wrong policies could still turn economic weakness into a more or less permanent depression.

In fact, that’s what seems to be happening in Europe as we speak.

Paul Krugman, New York Times 14 August 2014

European officials eagerly embraced now-discredited doctrines that allegedly justified fiscal austerity even in depressed economies (

And the European Central Bank, or E.C.B., not only failed to match the Fed’s asset purchases,

it actually raised interest rates back in 2011 to head off the imaginary risk of inflation.

Mr. Draghi & Co. need to do whatever they can to try to turn things around,

but given the political and institutional constraints they face,

Europe will arguably be lucky if all it experiences is one lost decade.

Ms Merkel does not say “no” to eurozone bonds. She says: “Not without treaty change.”

The German constitutional court in Karlsruhe would never allow Germany’s sovereign guarantee to be given to its eurozone partners

without them submitting to effective and centrally budgeted discipline.

Europe’s banking union is set to face a challenge in Germany’s constitutional court,

a development that threatens to generate renewed uncertainty over one of the main responses to the eurozone’s financial crisis.

EU’s banking union is illegal under German law because it was created without the necessary treaty changes.

Click

We academic economists knew what to do do deal with the financial crisis that started in 2007 and

to quickly restore normal levels of output relative to potential and of potential output growth.

But even though we knew what to do, we were not allowed to speak with one voice.

Brad DeLong, July 28, 2014

It was (a) not to do what Japan did in the 1990s, and

(b) take the advice of a long line of policy-oriented economists starting from the Say-Malthus debate of the 1810s and 1820s (which Malthus won) and

continuing through Mill, Bagehot, Wicksell, Keynes, Minsky, Kindleberger, Tobin, and many many others

But even though we knew what to do, we were not allowed to speak with one voice.

Other academic economists – including many whom I formerly counted as of note and reputation – elbowed their way into the debate.

They had either never bothered to learn the literature from Malthus to Tobin, had forgotten it, or were blinded by ideology.

They reached for simplistic models and methods that were clearly wrong

"Battle raging between the world’s leading macroeconomists"

The European Central Bank has found itself caught in the crossfire

The Bank for International Settlements’ call last month has reignited the debate over how to explain – and tackle –

the financial and economic turmoil that has persisted over the past six years.

The debate is so fierce, the viewpoints so distinct, that two of the world’s leading multilateral organisations,

the BIS and the International Monetary Fund, have completely different ideas on what the ECB’s next step should be

FT Money Supply blog 14 July 2014

Infrastrukturinvesteringar har blivit det fikonlöv bakom vilket åtstramningens kolportörer

gömmer det faktum att nu även de vill stimulera ekonomin genom ökad efterfrågan.

Rolf Englund blog 15 juli 2014

BIS

Investment by businesses is the key ingredient to cut our reliance on debt-fuelled current expenditure by consumers or the state

But there is a deeper issue to be tackled:

why does the economy have to be stimulated in artificial ways through the boosting of lending

Roger Bootle, Telegraph 6 July 2014

Leonid Bershinksy weeps over the cruel world that for some reason isn’t listening to Jaime Caruana of the BIS,

who warns that we must raise interest rates now now now.

Why is this prophet so lonely? And where are the bond vigilantes?

Paul Krugman, JULY 5, 2014

For decades, economic growth in America was driven by a powerful and sustainable force: increased consumption paid for by the rising incomes for middle-class and working-class Americans. But somewhere around 1980, that model broke down.

And now, with the economy only partially healed, it seems we’re going back to the lend-and-spend economy that failed us before.

Rex Nutting, MarketWatch 27 juni 2014

I admire the Bank for International Settlements.

It takes courage to accuse its owners – the world’s main central banks – of incompetence.

Yet this is what it has done, most recently in its latest annual report.

Martin Wolf, Financial Times 1 July 2014</p>

"All in all, the report is not good news"

BIS annual report suggests that “monetary policy is testing its outer limits,” and

that advanced economies, including the U.S., need “balance sheet repair and structural reform.”

Investors should take note, as the run-up in U.S. stocks has been driven by central bank accommodation using low interest rates.

MarketWatch 1 July 2014

We must end this addiction to debt as the engine of growth

There has been no serious attempt to get to grips with the financial cycle,

which requires moving away from debt as the engine of growth

Jeremy Warner Telegraph 30 June 2014

The venerable Basel-based Bank for International Settlements

“As history reminds us, there is little appetite for taking the long-term view”, the BIS thunders in its latest annual report.

“Few are ready to curb financial booms that make everyone feel illusively richer.

Or to hold back on quick fixes for output slowdowns, even if such measures threaten to add fuel to unsustainable financial booms.

Or to address balance sheet problems head-on during a bust when seemingly easier policies are on offer.

The temptation to go for shortcuts is simply too strong, even if these shortcuts lead nowhere in the end”.

In its annual report, Bank for International Settlements (BIS) spelled out

the risks of relying too heavily on monetary policy to stimulate the economy.

BIS warned that central banks including the Bank of England and US Federal Reserve could keep monetary policy loose for too long,

with potentially damaging consequences.

Szu Ping Chan, Telegraph 29 June 2014

Conventional wisdom has it natural interest rates have fallen

With debt in the developed world standing at higher levels than before the financial crisis,

one of the more disturbing threats to financial stability is an unexpectedly sharp rise in global interest rates.

John Plender, Financial Times June 24, 2014

The International Monetary Fund pointed out this month that housing can do a lot of damage.

An increase in prices provides an initial spur to the wider economy: construction activity is boosted and homeowners grow richer.

But as a boom continues, leverage grows and price rises become unsustainable.

The bursting of a bubble devastates bank balance sheets and leaves behind an economy that must painfully reallocate productive resources from a bloated construction industry to other sectors.

Mark Schieritz, economics correspondent of Die Zeit, Financial Times June 22, 2014

Jag är inte ensam

- I argued in 2003 that the housing market was becoming dangerously over-valued and that

at some point average prices would fall by about 20pc.

I made my prediction too early.

Roger Bootle, 15 June 2014

One of the more important insights about the state of the European economy

In their magnificent book House of Debt, Atif Mian and Amir Sufi find that

what is outwardly disguised as a credit crunch is in reality a fall in demand for loans.

Their analysis lends credence to the idea of a balance sheet recession

Wolfgang Münchau, FT 15 June 2014

När Carl Bildt och Göran Persson styrde Sverige

Diagram på RE blog juni 2014

Claudio Borio, the BIS's chief economist,

says this refusal to let the business cycle run its course and to purge bad debts is corrosive.

leads to "time inconsistency". It steals growth and prosperity from the future,

and pulls the interest rate structure far below its (Wicksellian) natural rate.

"The risk is that the global economy may be in a deceptively stable disequilibrium," he said.

Ambrose Evans-Pritchard 4 June 2014

US vs UK median real wage growth since 1988

FT Alphavillle, 29 April 2014

Accelratorn - Varför är den bortglömd? Det var Basics, vill jag minnas.

To have more or less full employment, we need sufficient spending to make use of the economy’s potential.

But one important component of spending, investment, is subject to the accelerator effect:

the demand for new capital depends on the economy’s rate of growth, rather than the current level of output.

Paul Krugman via Rolf Englund blog 21 maj 2014

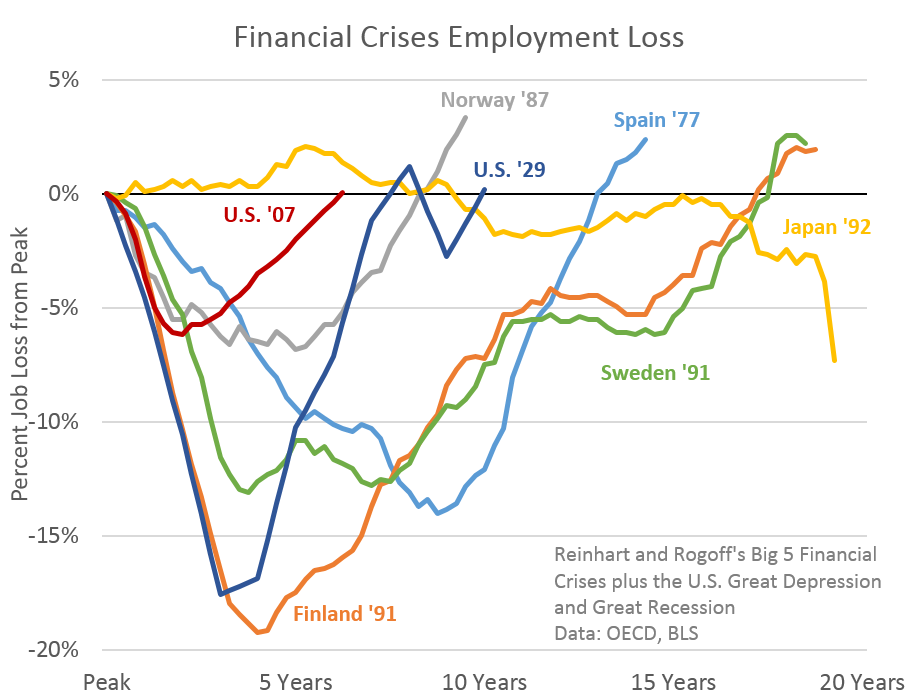

“The Great Recession: Causes and Consequences.”

We were suffering from inadequate demand.

Why, at the moment it was most needed and could have done the most good, did economics fail?

Paul Krugman, NYT 1 May 2014

Only the ignorant live in fear of hyperinflation

Failure to understand the monetary system has made it more difficult for central banks to act

Martin Wolf, FT April 10, 2014

Fortunately the Bank of England is providing much needed education.

In its most recent Quarterly Bulletin, its staff explain the monetary system.

So here are seven fundamental points about how it really works as opposed to how people think it does.

The act of saving does not increase deposits in banks. If your employer pays you, the deposit merely shifts from its account to yours.

This does not affect the quantity of money; additional money is instead a byproduct of lending.

What makes banks special is that their liabilities are money – a universally acceptable IOU. In the UK, 97 per cent of broad money consists of bank deposits mostly created by such bank lending.

Banks really do “print” money. But when customers repay, it is torn up.

Understanding the monetary system is essential. One reason is that it would eliminate unjustified fears of hyperinflation. That might occur if the central bank created too much money.

But in recent years the growth of money held by the public has been too slow not too fast.

Asset price bubbles and Central Bank Policy

“secular stagnation”

What the world must do to kickstart growth

The IMF in its current World Economic Outlook essentially endorses the “secular stagnation” hypothesis

Lawrence Summers, FT April 6, 2014

The IMF in its current World Economic Outlook essentially endorses the “secular stagnation” hypothesis, noting that the real interest rate necessary to bring about enough demand for full employment is likely to remain depressed for a substantial period. This is made manifest by the fact that inflation is well below target throughout the developed world and is likely to decline further this year

I’m pretty annoyed with Larry Summers right now.

His presentation at the IMF Research Conference is, justifiably, getting a lot of attention. And here’s the thing: I’ve been thinking along the same lines, and have, I think, hinted at this analysis in various writings.

But Larry’s formulation is much clearer and more forceful, and altogether better, than anything I’ve done

Paul Krugman, November 16, 2013

Yellen said recovery still feels like a recession to many Americans,

which is why the central bank will keep its “extraordinary” support for the economy for “some time to come.”

MarketWatch, 31 March 2014

I’ll eat my hat. The St Louis Federal Reserve – the last bastion of monetary orthodoxy in the Fed family –

has just published a paper that basically deems quantitative easing to be useless.

John Maynard Keynes was right all along.

The working paper by Yi Wen and Jing Wu cites China as the world’s resounding success story post-Lehman

Ambrose Evans-Pritchard, March 28th, 2014

A depressingly familiar reality lies behind the UK’s economic miracle

Growth is predicted to depend entirely on rising household spending, a recovering housing market,

and the questionable assumption of a bounce in business investment

Jeremy Warner, 24 March 2014

One of the abiding truisms of economics is that growth doesn’t happen without credit expansion.

This is well explained in a recent paper by the Bank of England,

which points out that money in the modern economy is largely created by commercial banks making loans.

It is a common misconception to think that banks only lend what they can borrow from depositors.

Jeremy Warner, 24 March 2014

Money creation in the modern economy

Bank of England pdf, QB 2014 Q1

Consumer credit and falling savings are indeed driving Britain’s unhealthy boomlet

Ambrose Evans-Pritchard, March 21st, 2014

The Bank of England will never unwind QE, nor should it

Governor Mark Carney more or less acknowledged this morning that the Bank of England will never reverse its £375bn of Gilts purchases.

Quite right too.

Ambrose Evans-Pritchard, 11 March 2014

Britain has just carried out one of the greatest victimless crimes in modern financial history. It is in effect wiping out public debt worth 20pc to 25pc of GDP – on the sly – without inflicting serious macroeconomic damage or frightening global bond markets.

How to make a graceful exit

Central banks’ forward guidance is a forgivable sin

Financial Times editorial, March 10, 2014

Why does everyone

— or, to be more accurate, everyone except those who have seriously studied the issue —

believe that the stimulus was a failure?

Because the U.S. economy continued to perform poorly — not disastrously, but poorly — after the stimulus went into effect.

There’s no mystery about why

Paul Krugman, NYT 20 February 2014

America was coping with the legacy of a giant housing bubble.

Even now, housing has only partly recovered, while consumers are still held back by the huge debts they ran up during the bubble years.

And the stimulus was both too small and too short-lived to overcome that dire legacy.

Even more importan, is the huge natural experiment Europe has provided on the effects of sharp changes in government spending.

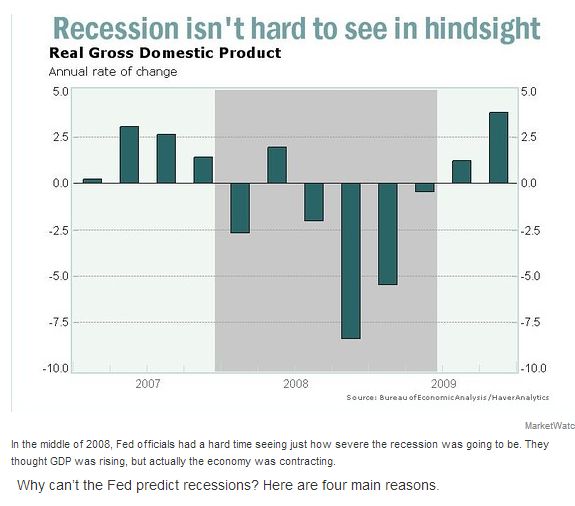

Recession - The R-word - Transcripts

Policy makers at the Federal Reserve tell us not to worry,

that it’s mostly just bad weather and the normal ups and downs of the economic data.

But what if they’re wrong? Would they tell us if they thought we were heading for a new recession?

Rex Nutting, MarketWatch, Feb. 27, 2014

The experience of the last recession, which started at the beginning of 2008, is telling.

Although the Fed began cutting interest rates months before the recession began and continued to cut rates aggressively throughout 2008,

policy makers were reluctant to use the “R” word, even in private, according to

the recently released

transcripts of the meetings of the Federal Open Market Committee.

While most policy makers had recognized by March that the economy was in a recession, they didn’t grasp the magnitude of the disaster until it was too late. Most of them thought the recession would be shallow and brief. Most of them thought the Fed would begin raising interest rates very quickly once the storm passed. They were wrong.

Laughing all the way to an economic crash

How the central bank coped with a crisis

DAVID WEIDNER'S WRITING ON THE WALL, MarketWatch, Feb. 25, 2014

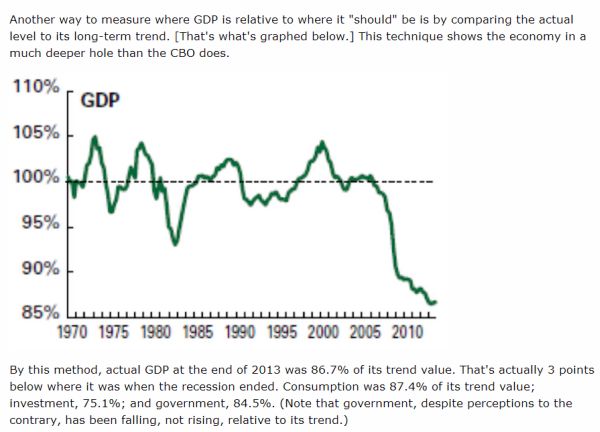

US GDP at the end of 2013 was 86.7% of its trend value.

That's actually 3 points below where it was when the recession ended.

John Mauldin, 10 February 2014

What was radical, if you like, was my style, not my content

On macroeconomics, there’s not a lot of air between my views and those of, say,

staff economists at the Fed Board of Governors, the New York Fed, the IMF, and even (say it quietly) the ECB.

Paul Krugman, New York Times 4 February 2014

They’re very much at odds both with freshwater macro and with austerian views; but no more so than those of many other economists — and austerian notions, like that of expansionary austerity, are far more radical than holding to old-fashioned concepts like the multiplier.

The impression that I’m some kind of far-out thinker largely comes from my willingness to go with what mainstream macroeconomics actually says, rather than shading my views and language to appease the Very Serious People.

Mainstream macro said that once you’re in a liquidity trap, deficits don’t drive up interest rates; money-printing doesn’t cause inflation; contractionary fiscal policy is very contractionary.

I said that, without hedging, and ridiculed the fashionable case for austerity.

But what was radical, if you like, was my style, not my content.

Consider what happened in 1936. F.D.R. had just won a smashing re-election victory

It’s very hard to communicate even the most basic truths of macroeconomics,

like the need to run deficits to support employment in bad times.

You can argue that Mr. Obama should have tried harder to get these ideas across;

many economists cringed when he began echoing Republican rhetoric about the need for the federal government to tighten its belt along with America’s families.

Paul Krugman, New York Times 23 January 2014

Cash

Global companies sitting on $7 trillion cash, double 2003

When the corporate cash dam bursts, everything will be ok, right? Well, maybe.

Investors have long assumed that a corporate spending revival will nurture a building economic recovery.

CNBC, 22 January 2014

Davos

One of the big stories here is that despite returning growth, business investment of the type that drives innovation, productivity gain and income growth is still as dead as a dodo.

They’ve got trillions of dollars in cash lying around on their balance sheets, but business leaders are still too cautious to loosen the purse strings.

So there is definitely something of a problem.

Jeremy Warner, Telegraph, 23 Jan 2014

The issue really comes down to whether you think it a supply-side issue, or simply one of absent demand.

“secular stagnation”

In a fascinating discussion with other leading international economists, Professor Summers argued that the only compelling solution to low growth was public investment.

Unconventional monetary policy, he argued, was no match for the problem, and in any case ran the risk of creating asset bubbles and renewed financial instability.

He also expressed grave concerns about the distributional consequences of sustained periods of negative real interest rates.

Jeremy Warner, Telegraph, 23 Jan 2014

For at least a decade and a half, cash has progressively increased its share of the American corporate balance sheet

According to research by the Federal Reserve Bank of St Louis,

their cash hoard had reached almost $5tn by the end of 2011.

John Plender, FT December 29, 2013

Rolf Englund blog 5 december 2009:

- Jag tycker det är skriande uppenbart att räntan världen över är för låg och att en större del av stimulanserna borde ske via finanspolitiken. Men väljarna och därmed deras medlöpande politiker är rädda för budgetunderskott och vill hellre att villaägarna skall låna än att staten skall göra det.

Strategin synes vara att det gäller att stabilisera, helst höja, villapriserna så att konsumenterna främst i USA skall återgå till att konsumera med lånta pengar, dvs just det som ledde fram till katastrofen.

Detta kan inte vara klokt.

Many are convinced that the US is a victim of secular economic stagnation and that its power and influence are waning inexorably as a result.

It is politically dysfunctional, its political class has been bought by Wall Street bankers with an efficiency and cynicism not seen since Cosimo de Medici bought up the 15th century papacy.

But... One of the important consequences of the financial crisis has been that it reinforced the role of the dollar as the world’s most sought after store of value in a storm.

John Plender, Financial Times 7 January 2014

Can Policy Boost Growth?

Some economic experts have suggested that US may be in a period of secular stagnation,

or protracted slow growth, similar to what followe Depression.

They propose further monetary and fiscal stimulus, but those have proven to provide only a temporary boost for short-term growth.

John H. Makin, American Enterprise Institute, 6 January 2014

Traditional macro policy also will not boost long-term growht.

While improving long-term growth is difficult, the best places to begin are with advances in a tax reform, deregulation, and freer trade. These structural measures, along with efforts to re high levels of policy uncertainty, might help boost sustainable, long-term economic growth.

Vi tackar P för länken

Secular stagnation

Since the start of this century, annual US gross domestic product growth has averaged less than 1.8 per cent.

The economy is now operating nearly 10 per cent – or more than $1.6tn – below what was judged to be its potential as recently as 2007.

And all this is in the face of negative real interest rates for terms of more than five years and extraordinarily easy monetary policy.

Lawrence Summers, Financial Times, January 5, 2014

A long time ago, the debate between monetarists and Keynesians was the debate in macro.

But it was a rather limited debate: both sides generally used the same model (IS-LM), and so it was all about parameter values.

More recently, but before the recession, that debate had largely gone away, but since then it seems to have come back.

This post asks why that is.

Simon Wren-Lewis, an economics professor at Oxford University, and a fellow of Merton College, 6 January 2014

Om bostadspriserna i Sverige börjar falla leder det till att konsumtionen går ner. Det slår också mot sysselsättningen.

Detta mardrömscenario har inträffat i andra länder och då fört med sig en långvarig recession med hög arbetslöshet.

Sverige tillhör de relativt fåtaliga som hittills har klarat sig, trots att skuldsättningen är högt uppdriven även här.

Enligt riksbankschefen ger detta dock inget skydd mot kommande bakslag, som i värsta fall också kan leda till en ny finanskris.

Stefan Ingves, DN 3 januari 2014

De svenska bankerna har tillgångar som motsvarar fyra gånger Sveriges hela BNP.

– Schweiz, Cypern och Nederländerna ligger högre. De har haft sina problem. Och under oss har vi Storbritannien, Danmark och Spanien och de har haft sina problem

– Samtidigt vet vi att mer än hälften av bankernas finansiering sker utomlands och det betyder att man där kan ha synpunkter på vår bolånemarknad.

I slutändan är det de utländska placerarnas syn på oss som är avgörande.

Den svenska bolånemarknaden har därmed blivit systemviktig

Stefan Ingves, DN 3 januari 2014

In 2010, most of the world’s wealthy nations, although still deeply depressed in the wake of the financial crisis,

turned to fiscal austerity: slashing spending and, in some cases, raising taxes in an effort to reduce

budget deficits that had surged as their economies collapsed.

Basic economics said that austerity in an already depressed economy would deepen the depression. But the “austerians,” as many of us began calling them, insisted that spending cuts would lead to economic expansion, because they would improve business confidence.

The result came as close to a controlled experiment as one ever gets in macroeconomics

Paul Krugman, New York Times 19 December 2013

I’m well aware that the austerians may win political points all the same. Political scientists tell us that voters are myopic (närsynta), that they judge leaders based on economic growth in the year or so before an election, not on overall performance in office.

So a government can preside over years of depression, yet win re-election if it can engineer an uptick late in the game.

Paul Krugman's Blind Spot

Sorry, but the New York Times' star columnist just doesn’t understand Europe.

Anders Åslund, Foreign Policy 8 November 2013

Interndevalvering (Ådals-metoden)

If the /UK/ economy was not massively overheated in 2007 and fiscal policy had not been hugely irresponsible,

what caused the post-crisis losses of output and consequent fiscal deterioration?

The answer to the first question is the global financial crisis.

Martin Wolf, Financial Times 19 December 2013

The panic led to sharp declines in financial sector profits, financial intermediation and economic activity.

The fiscal deterioration was then the result of these declines.

The present value of lost output would be close to five times annual GDP.

The Hubble bubble theory of the continuous expansion of the financial universe

All of which is a whimsical way of suggesting that perhaps Larry Summers has a point.

Perhaps inflating asset bubbles one after the other isn’t such a bad idea. Perhaps it’s even necessary?

Izabella Kaminska, FT Alphaville 6 December 2013

Conservatives and the cult of home-ownership

Promoting house-buying is a form of stimulus that does not overtly add to the fiscal deficit

Samuel Brittan, FT, November 28, 2013

The U.S. Treasury yield curve has lost its forecasting power

An ideal leading indicator would exclude components such as the yield curve that behave perversely during times of financial stress, said Morgan Stanley economist Ellen Zentner.

She suggested investors look at the Duncan Leading Indicator,

devised in 1977 by Wallace Duncan, then of the Federal Reserve Bank of Dallas.

Bloomberg, Simon Kennedy, Nov 27, 2013

Secular stagnation

Since the start of this century, annual US gross domestic product growth has averaged less than 1.8 per cent.

The economy is now operating nearly 10 per cent – or more than $1.6tn – below what was judged to be its potential as recently as 2007.

And all this is in the face of negative real interest rates for terms of more than five years and extraordinarily easy monetary policy.

Lawrence Summers, Financial Times, January 5, 2014

We may, as I argued last month in the Financial Times, be in a period of “secular stagnation” in which sluggish growth and output, and employment levels well below potential, might coincide for some time to come with problematically low real interest rates.

Larry Summers has argued that the short-term real interest rate consistent with full employment

fell to minus 2 or 3 per cent sometime in the middle of the last decade. This was due to an ex-ante global saving glut,

possibly reinforced by a weakening in ex-ante investment demand.

Because currency has a riskless zero nominal interest rate, nominal interest rates on other financial instruments cannot fall much below zero.

Willem Buiter, Financial Times 23 December 2013

With output significantly below potential since the start of 2008, the expected inflation required to achieve a significantly negative real interest rate with the nominal rate at zero has not been forthcoming, despite aggressive policy easing by the world’s leading central banks. The resulting unemployment is self-perpetuating. Human capital formation suffers: today’s high actual unemployment rate becomes tomorrow’s high natural unemployment rate.

Why stagnation might prove to be the new normal

In the past decade, before the crisis, bubbles and loose credit were only sufficient to drive moderate growth

Lawrence Summers, December 15, 2013

Is it possible that the US and other major global economies might not return to full employment and strong growth without the help of unconventional policy support? I raised that notion – the old idea of “secular stagnation” – recently in a talk hosted by the International Monetary Fund.

The implication of these thoughts is that the presumption that normal economic and policy conditions will return at some point cannot be maintained.

Even if the economy accelerates next year, this provides no assurance that it is capable of sustained growth at normal real interest rates.

"We should not dismiss the possibility, raised by Larry Summers

that we may need negative real rates for a long time"

I interpret this as IMF chief economist Olivier Blanchard saying,

as clearly and straightforwardly as his office allows him to,

that in his judgment the 2% per year inflation target is past its sell-by date and rotted,

and that the North Atlantic economies need to move to a 4% per year inflation target

in order to reduce the risk of another 1932, or another 2010.

Brad DeLong, November 20, 2013

Harvard economist Larry Summers created a stir earlier this month when he suggested that

the world economy may be entering a period of “secular stagnation,”

where aggregate demand fails to recover and sustain growth on anything like the pre-crisis trajectory.

Darrell Delamaide, MarketWatch, 20 November 2013

The hallmarks of this situation are deflation and underinvestment, which means monetary authorities will be forced to keep interest rates at zero.

“Imagine a situation where natural and equilibrium interest rates have fallen significantly below zero,” Summers said at an International Monetary Fund forum in Washington. “Then conventional macroeconomic thinking leaves us in a very serious problem because we all seem to agree that, whereas you can keep the federal funds rate at a low level forever, it’s much harder to do extraordinary measures beyond that forever, but the underlying problem may be there forever.”

Summers on bubbles and secular stagnation forever

Larry Summers’ speech to the IMF Research Conference on November 8, the video of which started circulating at old fashioned money multiplier rates this Sunday.