News Home

Home - Index - News - Krisen 1992 - EMU - Economics - Cataclysm - Wall Street Bubbles - US Dollar - Houseprices

Homeowners - the root of all evil?

Villaägarna - Roten till allt ont?

Rolf Englund blog 13 augusti 2013

One in four people between the ages of 18 and 24 defined the American Dream as being debt-free.

Once upon a time, the American Dream was a Technicolor affair, replete with two and a half thriving, college-bound kids,

a dog or cat and not one, but two cars in the garage that were owned outright, or would be before they were ready for the crusher.

For generations of Americans the American Dream was about owning a home.

ABC News, 8 September 2013

"The value of homeownership is deeply ingrained in American public culture," write William M. Rohe and Harry L. Watson in the introduction to their book,

Chasing the American Dream: New Perspectives on Affordable Homeownership.

The Great Recession affected all of us. The irrational exuberance of the mortgage boom and investment portfolios yielding 10 percent growth year after year led to a burst bubble, downsizing and various kinds of over-corrections.

Oseriösa bedömare förutspår spruckna bostadsbubblor och totalkrasch för Sveriges ekonomi om några år.

Men mera vederhäftiga beräkningar från Konjunkturinstitutet och Riksbanken kan inte bekräfta att det finns stora risker för en krasch.

Danne Nordling, 6 september 2013

The cult of home ownership is dangerous and damaging

You would think that the residential property bubble and subsequent crisis of the past decade

would make people leery of widespread home ownership, and governments reluctant to pump it up.

Yet, here we are again

Adam Posen, Financial Times, July 26, 2013

The real issue is the harm done by efforts in the UK and US to maintain and increase that rate. Start with the distortion to savings behaviour that mortgage subsidies and high loan-to-value ratios encourage.

For many American and British households, their home equity is their primary financial asset. In other words, we incentivise middle-class households to leverage the bulk of their savings into a highly volatile, difficult to price asset, which is subject to disaster risk both idiosyncratic (fire, tree falling on the roof) and general (flood, local industry closure), and which – based on the economic fundamentals – should return at best the average rate of local wage and population

An American economist on the Bank of England’s monetary policy committee,

Mr. Posen is no academic scribbler or lonely blogger

New York Times 17 Sept 2011

In Britain there is no government backstop for flood insurance. If you build a house in a vulnerable spot, you bear the cost yourself.

However, America has a scheme known as the National Flood Insurance Program, which was created in 1968

“in response to a widespread belief that flood hazard was uninsurable by the private sector alone”.

Gillian Tett, Financial Times

NFIP does insure $527bn worth of assets, or more than 5.5 million houses, and since 1978 it has paid out some $37bn of claims (excluding Hurricane Sandy).

States like Florida subsidise hurricane insurance too.

Uncle Sam's Flood Machine

The Government Should Get Out of the Flood Insurance Business

JANUARY 01, 2006 by JAMES BOVARD

Read more: http://www.fee.org/the_freeman/detail/uncle-sams-flood-machine#ixzz2ZZY3LoE0

Thanks Wayne for the link

The people of the US, UK, Spain and Ireland became feverish speculators in land.

Today, the toxic waste poisons the entire world economy.

Martin Wolf, FT July 8 2010

genom att renovera och byta begagnade bostadsrätter och villor med varandra till allt högre priser.

Dick Klang och Barbro Engman, SvD Brännpunkt 16/9 2009

Some 5.6m US home loans are at least three months in arrears on payments

FT January 23 2011

The post-election deadlock in Italy is an uncomfortable reminder that

the developed world’s sovereign debt problem ultimately boils down

not just to bad economics but to a failure of democracy.

John Plender, Finncial Times 26 February 2013

"The preservation of a sense of national identity"

What is the long-term justification for putting taxpayers on the line to subsidize homeownership?

Is this nothing more than a sacred cow in American society — a political necessity because so many voters own homes and are mindful of their resale value?

Robert J. Shiller, New York Times March 5, 2010

Conservatives and the cult of home-ownership

Promoting house-buying is a form of stimulus that does not overtly add to the fiscal deficit

Samuel Brittan, FT, November 28, 2013

It is better that governments stimulate housebuilding than do nothing at all, or leave everything to monetary policy.

But the main emphasis of government support is still on house purchases. My preferred solution is that when demand flags, cash should be put into the hands of residents to spend as they think fit.

Frequently they will not spend it well. But do we really think that politicians and civil servants, jockeying for position, will spend it better?

The biggest obstacle to this kind of even-handed approach is the balanced-budget dogma.

The Homeownership Obsession

As a society, we overinvest in real estate.

We build (and buy) too many extra-big homes and strive to make almost everyone into a buyer.

Robert J. Samuelson, July 26 2008

Barney Frank (THE CHAIRMAN OF THE HOUSE FINANCIAL SERVICES COMMITTEE)

Here is Frank saying he didn’t push for housing just last week:

And here is Frank in 2005 saying there is no bubble in the housing market and that subsidizing home ownership is a good plan

Pragmatic Capitalism 22 May 2010

President Obama's plan to limit two popular deductions for wealthy taxpayers will hit a wall of resistance from entrenched special interests.

The president once again proposed in his budget to curtail high-income earners' tax deduction for mortgage interest payments and charitable contributions.

CNNMoney February 15, 2011

The real estate industry is a powerful advocate for the mortgage interest deduction. And they are a major lobbying force on Capitol Hill.

"We will oppose any limit," said Jerry Howard, chief executive of the National Association of Home Builders. "This is an attack on the middle class."

Statskassan väntas bidra med 33 miljarder kronor 2011 till räntesubventioner för att de svenska hushållen ska kunna fortsätta jaga sitt drömboende.

Hushållens ränteavdrag väntas explodera mellan 2010 och 2011 till 124 miljarder kronor,

enligt Ekonomistyrningsverket ESV:s prognos

DI 25 maj 2011

Men Sverige är långt ifrån ensamt om att ha ränteavdrag. Enligt statliga Bostadskreditnämndens genomgång av reglerna i tio OECD-länder är Sverige ett lagomland i sammanhanget.

”Vi ligger någonstans i mitten. Avdraget är allra mest generöst i Holland. Där kan du dra av direkt mot din marginalskatt. Det är ganska generöst också i USA och även Danmark är mer generöst än i Sverige”, säger Bengt Hansson.

Det finns en berättigad oro för att en prisbubbla på fastigheter nu håller på att utvecklas.

En begränsad minskning av ränteavdraget är en effektiv och träffsäker åtgärd

Carl B Hamilton, ekonomisk-politisk talesperson och riksdagsledamot (fp), DN Debatt 5/1 2011

Många unga, högutbildade medelinkomsttagare i Stockholm är lånemiljonärer.

Fortsätter prisrallyt uppåt kan de fortsätta att använda sina villor och innerstadsbostadsrätter som bankomater för att plocka ut ännu mer pengar och åka till Bahamas på semester eller köpa en teppanyakihäll.

Sofia Nerbrand, Kolumn SvD 17/1 2011

Folkpartiets förslag skulle slå mot högt belånade bostadsrätts- och villaägare utan några större kapitalinkomster, menar Villaägarnas riksförbund.

”Man straffar fattiga för att gynna rika”, säger vice förbundsdirektör Joacim Olsson.

DI 5/1 2011

”De stora förlorarna skulle vara de högt belånade barnfamiljerna i storstadsregionerna, alltså de med minst marginaler”, säger Villaägarnas vice förbundsdirektör Joacim Olsson.

”En försämring av ränteavdraget från 30 till 25 procent skulle kosta ett hushåll med 3 miljoner i lån och med en ränta runt 6 procent, 9.000 kronor årligen”, fortsätter han.

Alla undantag till trots ställde förmögenhetsskatten till det för småföretagare som låtit vinstmedel ligga kvar i sina bolag. Det kom att betraktas som en sorts skatteflykt och ledde till beskattning enligt Lex Uggla. Men framför allt slog den mot hyggligt framgångsrik medelklass med sparkapital och ett hus eller sommarstuga, som ökat i värde i takt med att grannarna sålt.

PJ Anders Linder 15 november 2009

Trots att arbetslösheten stiger och svensk ekonomi krymper med fem procent – det största fallet på flera decennier – så växer hushållens bolån med över åtta procent i årstakt.

En rekordstor andel av hushållen väljer också att ta lån med rörlig ränta.

Finansinspektionens generaldirektör Martin Andersson och chefsekonomen Lars Frisell

DN Debatt 10/11 2009

Anledningen är naturligtvis dagens extremt låga ränteläge. Med rörligt lån har räntekostnaden för genomsnittsvillan i riket sjunkit med 3500 kronor i månaden på ett år.

I framtiden kommer krediter att bli dyrare igen, inte bara på grund av att inflationen återvänder. Nya regleringar på bankmarknaden kommer också att höja kreditkostnaderna.

Det är egentligen inte konstigt att bolånen har tagit en sådan fart. För skuldsatta hushåll som inte har drabbats av lågkonjunkturen har finanskrisen inneburit en rejäl ökning av den disponibla inkomsten. Det här gäller i synnerhet i städer med dominerande tjänstesektor och där arbetslösheten inte har slagit särskilt hårt.

Att välja rörliga lån är också naturligt – bundna räntor lönar sig sällan i det långa loppet.

Det är svårt att vara olyckskorp när allt går som smort

På frågan om hur han ser på exempelvis sänkta ränteavdrag och ändrad fastighetsbeskattning sade Anders Borg att

det gäller att titta brett på olika åtgärder.

"Vi ska inte stänga dörren, vi behöver en bred diskussion", sade han.

Dagens Industri 17/1 2011

Bostadspriserna är en av de mer allvarliga riskerna mot svensk ekonomi i ett medelfristigt perspektiv.

Men att vidta åtgärder för att dämpa stigande bostadspriser ligger inte i närtid för regeringen.

Anders Borg, 2009-11-04

Anders Borg: "Bopriserna måste bromsas"

Rolf Englund blog 7/12 2010

Om hushållens upplåning fortsätter att öka med 8 procent är det inte riktigt hållbart", säger SEB:s chefsekonom Robert Bergqvist.

Det är Statistiska centralbyråns, SCB:s, senaste finansmarknadsstatistik som ser ut som om Riksbanken misslyckats totalt i sin räntepolitik.

Tanken var ju att garantera företagen billiga lån för att få igång investeringarna och skapa nya jobb.

DI 27/10 2009

With the exception of temporary bubbles caused by reckless monetary policy, rising home prices are merely a symptom of a vibrant economy, not a cause.

The true cause of economic growth and higher living standards is rising productivity, which occurs when societies wisely invest in many things, such as new technologies and new ways of doing business.

Housing is just one of those things.

Setting as a goal the maintenance of high levels of investment in housing has obvious political appeal, but

it's junk economics for a nation that wants to innovate and grow.

Wall Street Journal 25/8 2010

My conclusion, then, is that the advanced countries remain highly short of demand.

In this environment, rapid cuts in fiscal support make sense if, and only if, monetary policy can be effective on its own and expanding the interest-elastic parts of the economy is the best way to climb out of the hole. There is reason to doubt both ideas.

Martin Wolf, July 6 2010

Most new borrowing during America’s housing boom was for spending

Almost all of the $1.45 trillion the authors estimate was borrowed against rising home equity was used for spending.

The Economist print, September 3rd 2009

Nästan alla väljer rörlig ränta

DI 2009-09-02

Fortsatt stor skillnad mellan den bundna tremånadersräntan och de längre bundna boräntorna bidrog till att 91 procent av låntagarna valde den kortaste bindningstiden i augusti. Det är den högsta andelen sedan mätningarna startade år 2000.

Det visar SBAB:s månadsstatistik över nyutlåningen till privatkunder.

Hushållens totala skulder hos bankerna ökade med 14 miljarder under juli,

nästan hela ökningen är bostadslån. Den årliga ökningstakten var i juli 7,9 procent.

Finansinspektionen 2009-08-31

"The preservation of a sense of national identity"

What is the long-term justification for putting taxpayers on the line to subsidize homeownership?

Is this nothing more than a sacred cow in American society — a political necessity because so many voters own homes and are mindful of their resale value?

Robert J. Shiller, New York Times March 5, 2010

Basic economics tells us that when Americans, over all, spend more on housing, they must ultimately spend less on something else. Why should housing consumption be better than other consumption, or investments that people might choose?

This time, the best answer isn’t found in traditional economics but rather in American culture: a long-standing feeling that owning homes in healthy communities is connected to individual liberties that embody our national identity. Historically, homeownership has been associated with freedom, while renting — often in tenements or mill villages — has been linked to the oppression of a landlord.

Financial bubbles are like epidemics

Robert J. Shiller, July/August 2008 Atlantic Monthly

An Englishman doesn't have to own his castle

We should all learn our lesson from the house-price bubble

Government must reshape the tax system so that it does not favour home ownership

Edmund Conway, 24 June 2009

Once the property market reacquainted itself with the law of gravity, after more than a decade of ever more improbable increases, house prices fell faster than in any post-war property slump. Your home is now worth around a quarter less than in the summer of 2007; as a result, negative equity is fast approaching the heights seen in the early 1990s.

The problem is that we have not yet absorbed the more fundamental message.

Housing bubbles are bad news – yes, even when prices rise rather than fall.

In bad times, there are families that suffer the pain and indignity of losing their homes, and households that see their finances crippled, perhaps permanently, by the whims of the market.

Also, bubbles distribute wealth (or at least perceived wealth) at random. Someone buying their first home in 2002 would have seen its value leap by more than 40 per cent over the next two years; anyone doing so in 2007 would have seen the price drop by around 25 per cent in the same period.

Government must reshape the tax system so that it does not favour home ownership. This may mean experimenting with a land tax, whereby families pay annual taxes based on the value of their home and land; it may mean imposing capital gains tax on first homes.

Owner occupation was artificially pushed higher by a series of lucrative tax breaks in the post-war era.

Before the financial crash, global demand was horribly skewed. It was far too reliant on spending from increasingly indebted American consumers:

There are other ways to reduce the deficit, including getting rid of the mortgage-interest deduction

The Economist print July 23rd 2009

"tro inte att det värsta är över"

Tongångarna från männen som förutspådde finanskrisen,

Nouriel Roubini, Marc Faber och Peter Schiff,

har inte blivit muntrare.

E24 2009-09-30

Peter Schiff:

Market-Crushing Treasury Collapse To Hit Around 2013

expects the coming crisis to blow the 2008-9 financial crisis out of the water

Forbes 27 ;March 2012

Everybody who bought real estate did it with somebody else's money

These guys actually believed that if they bought that house they would make $3 million over the next ten years.

Peter Schiff 16/6 2009

When people bought stocks they pretty much bought it with their own money. And if they got a margin account, maybe they had to put 50 percent down. And many of the brokerage firms were requiring higher margins on Internet stocks. So, when the bubble burst, the losses were pretty much confined to the people that made the bad bets. And at least when the losses happened, nobody tried to bail anybody out. If you lost money, you lost money. There was no one looking to the government to get their money back because they bought a dot-com stock that went to zero. None of the brokerage firms failed. Nobody failed because they had loaned money to people to buy stocks.

This time around, of course, everybody who bought real estate did it with somebody else's money. Very few people were paying 100 percent. Many people were buying real estate with none of their own money; people were buying real estate with nothing down. Is it any surprise that people gambled when they had nothing to lose?

And especially when they had so much to gain. Real-estate prices were rising. At one point, in California they took a survey ? I think back in 2005 ? and the average home buyer believed that his house was going to appreciate by 20 percent a year for the next ten years.

That was what was expected.

Now, you think about it. At the time, the average California home was selling for about $500,000, which was about ten times what the average household actually earned.

So, but these guys actually believed that if they bought that house they would make $3 million over the next ten years. That's what they believed.

How to Profit From the Coming Economic Collapse (Lynn Sonberg Books) (Hardcover)

by Peter D. Schiff

Kudlow On The Trade Deficit

Mr. Kudlow's rhetoric typifies an ongoing Wall Street, government, and media propaganda effort

that would even amaze George Orwell.

Peter Schiff 11/3 2005

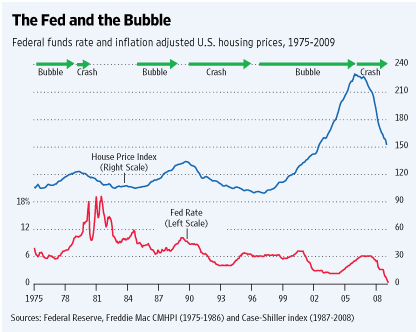

How owners' equivalent rent duped the Fed

In 2003 and 2004 the average fed-funds rates were lower than in any year since 1955 when the rate series began.

Monetary policy, mortgage finance, relaxed lending standards, and tax-free capital gains provided

astonishing economic stimulus: Mortgage loan originations increased an average of 56% per year for three years

-- from $1.05 trillion in 2000 to $3.95 trillion in 2003

Tim Iacono 6/4 2009

No, a wave of house repossessions will not necessarily teach the virtue of living within one’s means,

when the government is around to force lenders to stay their hands,

and create moral hazard on a huge scale

Irwin Stelzer The Sunday Times April 12, 2009

Can't pay or won't pay?

The write-downs, whether voluntary or court-ordered, could destroy the lenders’ capital.

Aggregate negative housing equity is thought to top $500 billion.

The Economist print Feb 19th 2009

"This risk has the potential to cause a global financial crisis"

“jingle mail”

What lessons, I wonder, will the great downturn of 2008 teach our children?

David Ignatius, Washington Post, January 1, 2009

En bonusdriven finansbransch har sålt stora mängder obskyra värdepapper

– samtidigt som man i Washington har sänkt skatter och fattat beslut om nya jätteprojekt utan att våga be folket om pengar.

PJ Anders Linder, SvD 25/1 2009

Det var inte bara Wall Streets finansföretag som byggde ekonomiska korthus med hjälp av högbelåning under de år då likviditeten flödade och räntorna var låga.

Även de amerikanska hushållen konsumerade som om det inte fanns någon morgondag genom att låna på villan och med ständigt kontokortskrediter trots att reallönerna knappast ökade alls.

Det var då, det.

Lars-Georg Bergkvist, SvD 9/11 2008

Varken den borgerliga alliansen eller socialdemokraterna mäktade med att försvara fastighetsskatten

mot de välorganiserade särintressen som satt dess existens i fråga.

Det är beklagligt att särintressen på detta sätt styrt den demokratiska agendan i en riktning som inte gagnar det allmänna intresset.

Jonas Agell m fl på SvD Brännpunkt 22/9 2006

Givetvis ska alla betala skatt på reavinster, men ...

Regeringen har således infört ett system som motverkar rörligheten på bostadsmarknaden och dessutom kommer att driva ett antal hushåll till konkurs.

Carl-Johan Jargenius, SvD Synpunkt 28 oktober 2008

Federal support of homeownership greatly overvalues its meaning in American life.

Through tax breaks and guarantees, the government boosted homeownership to its peak in 2004, when 69 percent of American households owned homes.

Subsidies for homeownership, including the mortgage interest deduction, reached $230 billion in 2009, according to the Congressional Budget Office.

Michael F. Ford, Washington Post, 6 January 2012

Meanwhile, only $60 billion in tax breaks and spending programs aided renters.

The result of this real estate spending spree? According to the Federal Reserve, American real estate lost more than $6 trillion in value, or almost 30 percent, between 2006 and 2010. One in five American homeowners is underwater, owing more on a mortgage than what the home is worth.

Those who profit most from homeownership are far and away the largest source of political campaign contributions. Insurance companies, securities and investment firms, real estate interests, and commercial banks gave more than $100 million to federal candidates and parties in 2011, according to the Center for Responsive Politics. The National Association of Realtors alone gave more than $950,000 — more than Morgan Stanley, Citigroup or Ernst & Young.

The Homeownership Obsession

As a society, we overinvest in real estate.

We build (and buy) too many extra-big homes and strive to make almost everyone into a buyer.

Robert J. Samuelson, July 26 2008

From the Newsweek magazine issue dated Aug 4 2008

Our infatuation with homeownership, embedded in dozens of government policies, has turned housing — once a justifiable symbol of the American Dream — into something of a National Nightmare.

/Infatuation is the state of being completely carried away by unreasoned passion or love; addictive love. Infatuation usually occurs at the beginning of a relationship. It is characterized by urgency, intensity, desire, and/or anxiety, in which there is an extreme absorption in another. It is traditionally associated with youth./

As a society, we're overinvesting in real estate. We build (and buy) too many extra-large homes. McMansions, if you will. They use too much energy, and their carrying costs, including mortgage payments, absorb too much of Americans' incomes, limiting the ability to save for retirement and other needs.

The avid pursuit of a few more percentage points on the homeownership rate (it rose from 64 percent of households in 1994 to 69 percent in 2005) has condoned enormously damaging policies.

When you subsidize something, you get more of it than you otherwise would.

Let's count the conspicuous subsidies.

The biggest of these favor the upper middle class.

Homeowners can deduct interest on mortgages of up to $1 million on their taxes; they can deduct local property taxes, and profits (capital gains) from home sales are mostly shielded from taxes.

In 2008, these tax breaks are worth about $145 billion.

Next, government funnels cheap credit into housing through congressionally chartered Fannie Mae and Freddie Mac.

Finally, the Federal Housing Administration (FHA) insures mortgages for low- and moderate-income families that typically require only a 3 percent down payment from buyers.

The theory of the new legislation is that more subsidies will stabilize the housing market and stimulate a recovery.

It's also true, as economist Mark Zandi shows in his new book, "Financial Shock," that today's housing collapse had multiple causes

Still, the government's pro-housing policies contributed in two crucial ways.

First, they raised demand for now suspect "subprime" mortgages.

Second, government's housing bias created a permissive climate for lax lending. Both the Clinton and present Bush administrations bragged about boosting homeownership. Regulators who resisted the agenda risked being "roundly criticized," notes Zandi.

Beginning in 1992, Congress pushed Fannie Mae and Freddie Mac to increase their purchases of mortgages going to low and moderate income borrowers.

Russel Roberts, Wall Street Journal 3/10 2008

Mr. Roberts is a professor of economics at George Mason University and a scholar at the Mercatus Center.

His latest book is a novel on how markets work,

The Price of Everything: A Parable of Possibility and Prosperity

Princeton University Press, 2008

For 1996, the Department of Housing and Urban Development (HUD) gave Fannie and Freddie an explicit target -- 42% of their mortgage financing had to go to borrowers with income below the median in their area.

The target increased to 50% in 2000 and 52% in 2005.

Congress designed Fannie and Freddie to serve both their investors and the political class. Demanding that Fannie and Freddie do more to increase home ownership among poor people allowed Congress and the White House to subsidize low-income housing outside of the budget, at least in the short run. It was a political free lunch.

The Community Reinvestment Act (CRA) did the same thing with traditional banks. It encouraged banks to serve two masters -- their bottom line and the so-called common good. First passed in 1977, the CRA was "strengthened" in 1995, causing an increase of 80% in the number of bank loans going to low- and moderate-income families.

The Fed did its part, too. In 2003, the federal-funds rate hit 40-year lows of 1.25%.

That pushed the rates on adjustable loans to historic lows as well, helping to fuel the housing boom.

The Taxpayer Relief Act of 1997 and low interest rates -- along with the regulatory push for more low-income homeowners -- dramatically increased the demand for housing.

Between 1997 and 2005, the average price of a house in the U.S. more than doubled.

Bankers, like gangs, just get carried away

“So long as the music is playing, you’ve got to keep dancing. We’re still dancing.”

Chuck Prince, former chairman and chief executive of Citigroup

John Kay, FT February 12 2008

Givetvis ska alla betala skatt på reavinster, men ...

Regeringen har således infört ett system som motverkar rörligheten på bostadsmarknaden och dessutom kommer att driva ett antal hushåll till konkurs.

Carl-Johan Jargenius, SvD Synpunkt 28 oktober 2008

Alla som under 2008 sålt sitt hus eller bostadsrätt och flyttat till ett annat hus eller en annan bostadsrätt måste i början av 2009 betala betydande belopp till staten för att de bytt bostad under 2008.

Det innebär att ett stort antal hushåll i Stockholms- och Uppsalaregionen, där bostadspriserna ofta ligger i spannet 3–6 miljoner kronor och där reavinsterna därmed uppgår till flera miljoner, i början av 2009 måste punga ut med åtskilliga miljoner till statskassan, för att de bytt bostad. Dessutom tvingas berörda hushåll betala 0,5 procent på alla tidigare beviljade uppskov.

(lenders have no recourse to the house's owner beyond the value of the house),

individuals with negative equity have an incentive to default.

Martin Feldstein, FT May 7 2008

America's house price time bomb

Some American home-owners are taking radical action;

they are choosing to walk away from homes and their mortgages.

Michael Robinson, BBC, 29 July 2008

Highly Recommended

In May 2006, at the height of the housing boom, Karen Trainer bought a $500,000 apartment in California - with money borrowed from her bank.

By this year, Karen still owed $500,000 on her mortgage, but her apartment was worth $200,000 less.

As a successful professional, Karen could comfortably have managed the higher mortgage payments her bank demanded.

Instead, she decided to stop her mortgage payments altogether and let her bank repossess her apartment.

Her credit record will be badly damaged by the decision, but Ms Trainer expects this to recover soon.

"Generally speaking, within 5 years you are about back where you were, so my husband and I decided we'll take the hit and live with it."

By walking away from her apartment, Ms Trainer has also walked away from the loss on her property.

Her bank gets stuck with that.

Professor Nouriel Roubini of New York University, one of the first economists to warn of the dangers of the American house price boom, believes the number of people positively choosing to walk away is growing rapidly.

"This is becoming a tsunami of voluntary defaults," Professor Roubini says.

"The losses for the financial system from people walking away could be of the order of one trillion dollars when the entire capital of the US banking system is only $1.3 trillion.

"You could have most of the US banking system wiped out, so this is a total disaster."

"jingle mail"

More people will post the keys to their lender and walk away.

The Economist print - Searching for Plan B - 28/2 2008

These days, home buyers almost always have to make a substantial down payment,

at least 5%, according to Rich Wordman, president of the Florida Association of Mortgage Brokers. The days of no-down loans are over.

In deeply declining markets, lenders are reluctant to issue loans unless borrowers put at least 10% down, he said.

CNNMoney July 18, 2008

Comment by Rolf Englund:

For the combination of greed by by the homeowners and irresponsibilty of the

politicians see Public Choice

Household debt now totals about $10 trillion, or roughly 115 percent of personal disposable income.

In 1945, debt was about 20 percent of disposable income.

Robert J. Samuelsson Washington Post 29/12 2004