US Dollar

Euron spricker när dollarn faller

Rolf Englund, Nya Wermlands-Tidningen 8/1 2001

Which is the tail and which is the dog?

The dollar is falling, the oil price is rising, bond yields are rising

and stocks have just endured two uncharacteristically tough days after a prolonged period of exuberance.

John Authers, FT 30 January 2018

It appears to be the dollar dog that is wagging everything else.

Full text

Top of page

Only the Argentine Peso is weaker against the greenback this year

One of the more remarkable things about this selloff is how broad based it is.

The dollar is weaker in 2018 against all major currencies.

Widening the basket to the extended majors, only the Argentine Peso is weaker against the greenback this year.

Bloomberg 25 January 2018

Greenback weakness would have far-reaching consequences for financial assets in 2018

FT 2 January 2018

Russell Clark, partner at hedge fund manager Horseman Capital Management, has noted how the so-called net international investment position (NIIP) of the US, which in effect measures the net assets of a nation against the rest of the world, has been significantly deteriorating in recent years.

Mr Clark notes how such large changes in a country’s net international investment position “tend to be good signs of potential currency weakness or of potential weakness in bonds where currency cannot make the adjustment”.

Full text

Top of page

Pundits have been saying last rites for the dollar’s global dominance since the 1960s

– that is, for more than half a century now.

But the pundits may finally be right

Barry Eichengreen, Project Syndiate 11 October 2017

To the consternation of many currency traders, the value of the dollar fluctuates widely, as its rise, fall, and recovery in the course of the last year have shown

Full text

How the dollar’s weakness is the rest of the world’s problem

Forex markets pose a threat to a synchronised recovery needed to validate stock prices

Mohamed El-Erian, FT 13 September 2017

John Connally, when Treasury secretary in President Richard Nixon’s cabinet, famously told his European counterparts in 1971 that the dollar “is our currency but your problem”

Most economies now have to contend with a stronger headwind to growth and, in the case of Europe, downward pressures on an inflation rate that the central bank worries is already too low.

Full text

Top of page

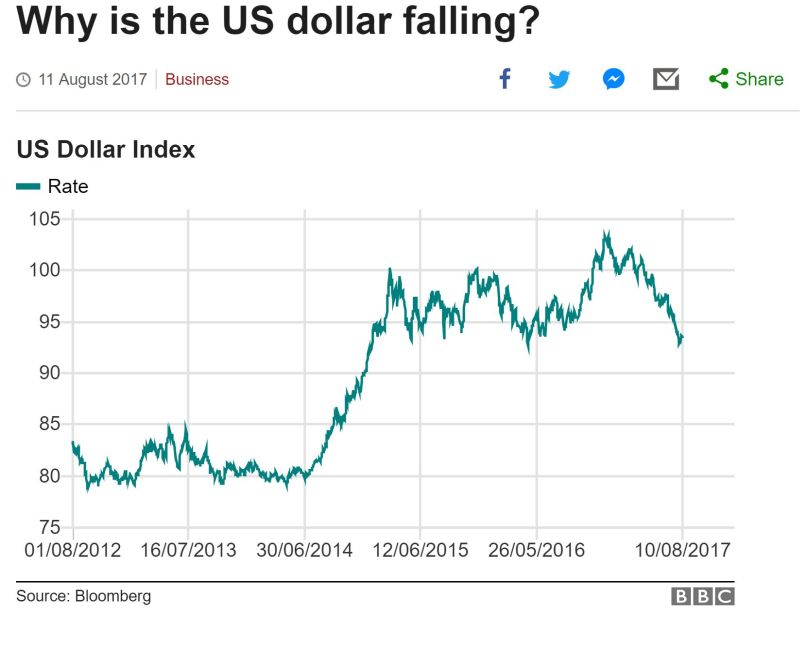

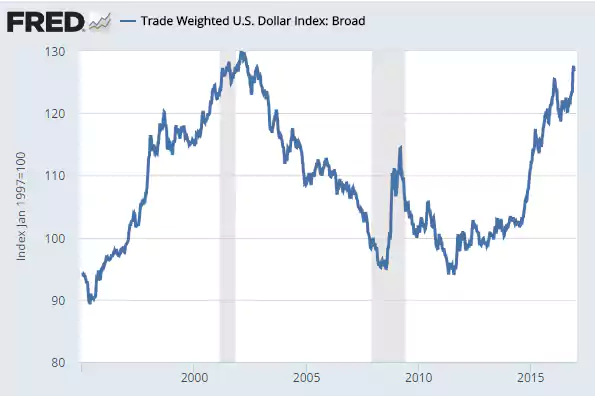

The value of the dollar index, which tracks the dollar against six major global currencies, has fallen about 10% since January.

The dollar, which surged in 2014 as the US economy gained strength, is hardly in danger territory.

The index is running just a bit lower than it was a year ago.

Full text at BBC

President Trump abandons the strong dollar policy

Gavyn Davies, 15 April 2017

President Trump’s remarks last week about the dollar and US monetary policy offer more evidence that

America’s strong dollar policy,

launched in 1995 by Treasury Secretary Robert Rubin when the dollar was near post-war lows, is now changing.

After 2002, the strong dollar policy officially remained intact under successive Administrations,

but the dollar itself refused to listen to the rhetoric, and

the real effective index fell to new all-time lows during the Fed’s programmes of quantitative easing, in 2009-13.

Full text

Top of page

President Donald Trump triggered a slide in the US dollar

as he complained the currency has risen too high

also revealed a major policy U-turn as he said that the US government would not label China a currency manipulator.

FT 12 April 2017

Full text

Soaring Trump dollar risks global trade war and China currency crisis, warns Posen

Donald Trump will succeed in ramming through radical tax cuts and fiscal stimulus, causing US federal borrowing to balloon.

The Peterson Institute thinks the current account deficit could rise to 5pc of GDP.

Ambrose Evans-Pritchard, 11 April 2017

We expect the dollar to rise by another 10pc to 15pc.

A hawkish Fed could prove painful for investors still hoping that central banks will come to the rescue whenever there is trouble,

be it the 'Yellen Put' in the US, the 'Draghi Put' in Europe, or the 'PBOC Put' in China.

Politicians from the G5 powers ultimately intervened to drive down the Reagan dollar at the Plaza Accord in 1985,

with dire side-effects. That attempt to manipulate currencies in defiance of economic fundamentals led

- by a complex chain of causality - to the Nikkei bubble in Japan, and to the 1987 stock market crash on Wall Street.

Mr Posen is a former rate-setter on Britain's Monetary Policy Committee, best known for his work with former Fed chief Ben Bernanke on Japan's Lost Decade and inflation targeting.

Full text

Top of page

A modest proposal to save the world

Charles Gave on The End of the Dollar Standard

via John Mauldin 7 February 2017

Read more here

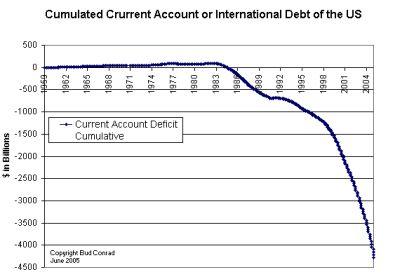

America's Unsustainable Current Account Deficit

"Never in the history of modern economics has a large industrial country run

persistent current account deficits of the magnitude posted by the U.S. since 2000."

National Bureau of Economic Research, 23 January 2017

Top of page

The dollar is no longer a cheap currency.

When the dollar set off on its nine-month 25 per cent tear in 2014,

it was starting from a position of significant undervaluation.

FT 30 January 2017

Today, the trade-weighted dollar is approximately 15 per cent overvalued on a purchasing power parity basis against other G10 currencies.

Top of page

In 1985, the United States famously gathered economic bigwigs of other major American trade partners at the famous Plaza Hotel in New York

to agree to coordinated interventions leading to a weaker US dollar and stronger yen, deutsche marks, francs, etc.

Between then and now, Donald Trump briefly owned the Plaza--hence his cameo appearance giving directions to Macaulay Culkin in Home Alone 2:

Lost in New York set in--where else--the New York Plaza.

Read more here

Why Treasury secretaries should stick with the strong dollar mantra

Lawrence Summers, FT 25 January 2018

Yes, a weaker dollar means cheaper US exports.

But it also means higher-priced imports and, therefore, less purchasing power for American incomes.

It is much better to strengthen our fundamentals than to make ourselves poorer by putting our goods on sale as we push our currency down.

Full text

That was the year Summers was celebrated along with Alan Greenspan and Robert Rubin as “The Committee to Save the World”

The End of the 'Strong Dollar' Policy (Yes, Again)

Don't believe everything Treasury secretaries say.

Daniel Moss, Bloomberg 24 januari 2018

Treasury secretaries of both political colors have dialed it up and dialed it down to suit the needs of the moment.

I remember sitting in Bloomberg's London newsroom hearing that the sky was falling when Paul O'Neill and John Snow, the first two Treasury chiefs under George W. Bush, veered from the script developed by Robert E. Rubin, who held the post under Bill Clinton and is most closely associated with the term.

Full text

Top of page

Rubin strong-dollar-policy

marketwatch 2017-01-17

Previous incoming administrations have ritualistically sworn fealty to a strong dollar,

saying this was in the interests of the US economy

— even when the currency’s value was arguably doing more harm than good at the time.

FT 17 January 2017

Full text

ECB-chefen Trichet skämtar:

"It is extremely important that the US has been saying that a strong dollar is in the interests of the US." Rolf Englund 2009-07-07

Trump said the U.S. currency, has gotten “too strong,”

Trump said the U.S. currency, which touched a more-than 14-year high about two weeks ago, has gotten “too strong,”

“Our companies can’t compete with them /China/ now because our currency is too strong. And it’s killing us,” he told WSJ.

MarketWatch 17 January 2017

Why Trump attacks China and Germany

It may have someting to do with that those countries have large trade surpluses with USA, I guess.

The United States has the world's largest trade deficit and has run one since 1975.

Rolf Englund 16 January 2017

King dollar will tighten the noose on emerging market debtors with $3.5 trillion of liabilities in US currency.

It will force banks in Europe - through complex hedging contracts - to curtail offshore lending to

the Pacific Rim, Turkey, Russia, Brazil, and South Africa.

It will lead to a credit crunch in the developing world.

Ambrose 2 January 2017

Top of page

Before 1971, US global hegemony was predicated upon America’s current-account surplus with the rest of the capitalist world,

which the US helped to stabilize by recycling part of its surplus to Europe and Japan.

This underpinned economic stability and sharply declining inequality everywhere.

But, as America slipped into a deficit position, that global system could no longer function,

giving rise to what I have called the Global Minotaur phase.

Yanis Varoufakis, Project Syndicate 28 November 2016

Lack of Chinese capital may well force the US to pay a steeper price for external financing,

through a weaker dollar, higher real interest rates, or both

Stephen S. Roach, Projet Syndicate 23 May 2016

Strong dollar took a $5 billion bite out of Apple’s results

MarketWatch 27 January 2016

Full text

Top of page

News

The U.S. dollar, at its highest level in nine years, is about to fall off its perch.

That’s the outlook, at least, of Lawrence G. McDonald, n his New York Times best-seller, “A Colossal Failure of Common Sense,” warned colleagues at Lehman Brothers

Energy companies took out $1.6 trillion worth of debt since 2009. Since 2012, emerging market governments and companies have taken out around $2 trillion worth of debt.

The catch here is that they often borrowed in dollars.

MarketWatch 7 january 2015

Energy companies took out $1.6 trillion worth of debt since 2009, much of it high-yield, McDonald estimates. Now with oil in sharp decline, a lot of that high-yield debt is starting to look questionable.

Since 2012, emerging market governments and companies have taken out around $2 trillion worth of debt.

The catch here is that they often borrowed in dollars.

- We’re having a difficult time finding any strategists who aren’t dollar bulls. When everyone is piled into one side of a trade, run, don’t walk, to the other side.

Full text

“A Colossal Failure of Common Sense,” Wikipedia

“A Colossal Failure of Common Sense,” Amazon

Lehman Brothers

Top of page

Since the debt crisis of 2008, the foreign-exchange market has been the dog that didn’t bark.

The euro has not broken up; the dollar has not imploded in the face of quantitative easing;

The yuan has not become the world’s reserve currency of choice.

USD trade-weighted index is within 2% of where it was when Lehman Brothers crumbled

Charlemagne, The Economist print 1 February 2014

Lehman Brothers

Sverige devalverade 1976-1982 och Bildt försökte hålla kursen 1992

Sverige devalverade 1976-1982 och Bildt försökte hålla kursen 1992

Dollarn steg av sig självt efter den svenska devalveringen 1982, därav den icke avsedda överhettningen

Det tramsades på sin tid mycket om att överhettningen berodde på "den misslyckade eftervården"

1992 var dollarn i botten (och kronan i topp) sedan, efter Bildts misslyckande, steg dessutom dollarn åter av sig självt,

vilket tillsammans med den flytande kronan räddade Sverige,

Det var alltså inte Göran Persson som gjrode det

What is it that people don’t understand about the trade deficit? It’s not rocket science.

The Current Account Deficit is over $800 billion a year.

Everyone agrees that the current trade imbalances are unsustainable and will probably trigger major economic disruptions that will thrust us towards a global recession.

Mike Whitney

Will the US request a bailout? Will the International Monetary Fund grant it? On what terms and conditions?

What writedown of US debt will be needed to restore sustainability to its fiscal accounts?

These are not questions being asked today but they are questions worth contemplating.

Thinking the unthinkable is one of the lessons of the eurozone saga. Another is the speed with which complacency can convert to crisis.

So although I am not predicting Armageddon, I would like to signal a series of factors that policy makers of all nationalities would do well to keep in mind.

Robert Jenkins, a former fund manager and current external member of the Financial Policy Committee of the Bank of England, Financial Times 14 November 2012

Full text

The optimists will be right until they are wrong.

Wolfgang Munchau

Top of page

Once upon a time America was able to achieve full employment without a housing bubble and with savings rates even higher, Krugman

A lower dollar means more exports, and it also means a shift from consuming imported products, Martin Feldstein

US can terminate its reliance on debt-financed consumer demand, and sustain recovery, only by a big improvement in its trade balance, Fred Bergsten

Kronan starkaste nivån sedan sommaren 1998.

Current Account Imbalances Coming Back, Joseph E. Gagnon, Peterson Institute

If you want to worry about something, I can recommend the US current account deficit,

Richard Robb, Economists' Forum, FT

Dollar Again Substantially Overvalued, Peterson Institute

Should wealth-holders come to doubt the determination of the Federal Reserve to preserve the dollar’s domestic purchasing power, FT editorial

"What happens when the dollar collapses?", dollarcollapse.com

- See also Cataclysm, Rolf Englund

"The housing market or stock market Mr. Bernanke...save one", Brady Willett

probable fall, of America’s empire, the yawning US current account deficit, Niall Ferguson

Bernanke: Fed “attentive to the implications of changes in the value of the dollar.”, Goyette, author of The Dollar Meltdown

Everyone realizes that the dollar will have to fall to enable the U.S. to export more, since American households will be consuming less, Eichengreen

Why will the dollar be the first of today’s fiat currencies to collapse? dollarcollapse.com

China May Allow Currency to Rise Against Dollar, CBC/Reuters, 11 Nov 2009

Dollarn på sin lägsta nivå mot kronan på över ett år, fallit med 28 procent, DI

"The euro at $1.50 is a disaster for the European economy and industry,", Henri Guaino, right-hand man of President Nicolas Sarkozy, Ambrose

The gap between US imports and exports grew 16 percent to $32 billion in July Bloomberg

China’s central bank: “Failure to manage the degree of easing may lead to concerns about mid- and long-term inflation and exchange-rate stability,”, Click

Rebalancing global growth, The Economist

Summers: “The global imbalances have to add up to zero, FT July 2009

ECB-chefen Trichet skämtar: "It is extremely important that the US has been saying that a strong dollar is in the interests of the US." Rolf Englund

Is this the death of the dollar?, Edmund Conway

Non-oil goods imports were down 25% y/y, Brad Setser with nice charts

Excluding petroleum, the deficit was little changed at $21.3 billion, Bloomberg

Crisis roots stem from imbalances, Bernanke

Obama believes China manipulating its currency, Timothy Geithner

The longer-term challenge is to force a rebalancing of global demand, Martin Wolf

China and America should be viewed as a single economy – or at least as a single currency area, Brad Setser

This is the endgame for the global imbalances, Martin Wolf

US dollar fell below 96 yen, its lowest level for 13 years, BBC

$9.4 trillion in dollar-denominated securities were sitting in the vaults of foreign investors, James Grant

This may prove to be the dollar’s epochal moment, Conway Daily Telegraph

FEER of falling, PPP $1.16, Yet a euro buys $1.55, Economist

The results for the US would be unpleasant:

a currency crash and even higher domestic inflation, FT Editorial

Does the new dollar policy make sense?, The Economist

Why hasn’t dollar devaluation worked? FT Lex

Matters could get out of hand unless America took steps to halt the slide, Jean-Claude Juncker

Trade balances are determined by national savings propensities, not exchange rates, Hanke

Divine intervention, The Economist

Själv har jag sedan i maj 2006 argumenterat för att det mesta talar för att dollarkursen befinner sig i en nedåtgående trend, Olle Wästberg

There seems to be no floor for the dollar, Economist

En dollar kostar nu mindre än 6 kronor, DI

Dollar low against the euro touched 1.5239, BBC

Central banks and sovereign funds supplied the US with $52.1b, Private investors supplied $8.4b (net), Brad Setser

U.S. trade deficit december $58.8 billion, 2007 deficit $711.6 billion

The US cannot drive the world economy for ever, Financial Times editorial

America's current account deficit is due more to bubbles in asset prices , Roach

Can the troubles of the US currency be confined to the financial world or are they set to undermine Washington’s place on the international stage? - FT

How to solve the problem of the dollar, Bergsten

Why the dollar’s drop is failing to rebalance the world, Giles FT

Dollar crisis on top of credit crunch and weakening economy frightening, The Economist

Dollar’s last lap the Bretton Woods II theory, Munchau

Dangers of a deepening crisis, Summers

United Arab Emirates and Qatar are considering dropping the dollar peg, Münchau

The only factor that could mitigate, or even prevent, an outright recession in the US is a very sharp further fall in the dollar, Munchau

US trade deficit for September dipped by 0.6 percent 56.5 billion, CNN

“monetary disorder risked turning into economic war”, Sarkozy

The imbalance problem has begun to fade away, Samuel Brittan

This constellation of forces could prove especially vexing for the US dollar, Roach

The dollar has finally begun its long overdue correction, Feldstein

Dollar Overvalued, IMF

Fall in the dollar will increase inflation Jeffrey Garten Naked Capitalism

A dreadful dilemma, Martin Wolf

If the US Treasury doesn’t think the dollar is overvalued, can it also think that RMB is undervalued? Brad Setser

The US trade gap fell in June, Rpts

Dollar against the currencies of main trading partners, Justin Fox

The recent sell-off in financial markets is good news, The Economist

China would have grown by 9% even if its trade surplus didn't grow

This is a time when the global economy should be adjusting, Brad Setser

Without political union, the eurozone has little chance of survival, de Grauwe

The Monetary Union of United States and China, McCulley

Dollar-euro? It's the yen, stupid, CNN

US trade deficit $60 billion May

U.S. trade deficit April $58.5, Bloomberg

'Prophets of doom' will be right in the end... a markets economy, Englund, FT

US debt might unsustainable pressure on dollar coordinated strategy

adjust global imbalances while avoiding recession, Good idea from UN

How did we get here? The process was started by money printing to bail out the last bubble, Fleckenstein

IMF Plan for Action on Global Imbalances, Martin Wolf, Nicholas Lardy, John Lipsky, Thomas Dooley

Larry Summers /and Paul Volcker/ described himself as a “chastened prophet”, Brad Setser

Best Quotes of April 2007, dollarcollapse.com

The coming US current account surplus, Gabriel Stein

The burden of supporting the world economy can hardly rest indefinitely on the shoulders of Anglo-American shoppers and home owners, Samuel Brittan

The falling dollar (read falling RMB) has done more to stimulate China’s exports than to stimulate US exports, Brad Setser

U.S. March Trade Gap widened 10.4 percent to $63.9 billion, Bloomberg

I don't see the euro in the $1.40s for long, Robert Mundell

A very substantial correction of the US external deficit,

including via a very large decline of the exchange rate of the dollar, is inevitable, Bergsten

Measured in euros U.S. economy has been in a seven-year recession, The Market Oracle

The story right now is generalized euro strength, not generalized dollar weakness, Brad Setser

What is it that people don’t understand about the trade deficit? It’s not rocket science, Mike Whitney

It all boils down to the consumption response to the bursting of the US housing bubble, Roach

Wanted: a guardian of the world’s financial system updating Bretton Woods, John Grieve Smith, FT

"Global imbalances" biggest threat to long-term stability - Rodrigo de Rato

China runs a big surplus with the world, not just the US - $230b, Brad Setser

Nouriel Roubini is a real grizzly, not just a bear, Brad Setser

Caveat Emptor, Lawrence Kudlow. Yes, Lawrence Kudlow

A set of policies that would facilitate global adjustment, Brad Setser

Real possibility combination of higher long-term interest rates and a weaker dollar, Summers

Within an hour of the statement, the dollar had slipped to its lowest level

against the euro in two years, FT

Chinese purchases of yen. Fred Bergsten

Wait until the U.S. tries to buy imports with depreciated dollars. Eric Janszen I-Tulip

December 21st month with negative savings rate, Peebles

Significant part of what people call excess liquidity comes from US current account deficit". Marc Faber

US trade deficit at record high of $763.6bn in 2006 BBC

Kina ska lyfta ut 210 miljarder dollar ur sin valutareserv

OPEC nations unloading Treasuries Bloomberg

The People's Bank of China (PBOC) is well-respected. However... Bernanke

Will the dam break in 2007? Stiglitz

The greatest divergence for a generation between the general view of global risks and the risks as priced in financial markets. Summers

In looking to 2007, my main message is to be wary of extrapolation. Stephen Roach

The optimists will be right until they are wrong. Wolfgang Munchau

Can the world economy thrive without ever-increasing U.S. trade deficits? Robert J. Samuelson

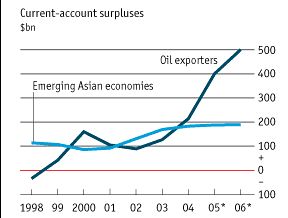

China's surplus is dwarfed by oil-exporting economies,

surpluses may undermine efforts to unwind global imbalances in an orderly way. The Economist

"the dollar is our currency, but your problem".

US exports are also at last growing at roughly the same rate as imports Martin Wolf

The waning dollar and a not-so-brave new world John Plender

Countries worst affected would be the Netherlands, Denmark, Sweden, Norway, the UK and Switzerland.

None of these countries, save for the Netherlands, is a eurozone member. Wolfgang Munchau

Börsen faller - dollarn på lägsta nivån sedan mars 2005, Dagens Industri

America's economy has not significantly outperformed Europe's in recent years. The Economist

Pound at highest level since ejection from ERM September 1992.

The US may be able to cope with a fall in the dollar, FT editorial

Let us equip ourselves with a real exchange-rate strategy, Dominique de Villepin

The dollar is our currency, but your problem, John Connolly

USD trade-weighted index is within 2% of where it was when Lehman Brothers crumbled, Charlemagne Jan 2014

Why the dollar stays steady as America declines, Eswar Prasad, The Dollar Trap, Gillan Tett, February 2014

More News on this page

De globala obalanserna, där USA visar stora underskott mot omvärlden och framför allt länderna i Ostasien går med stora överskott, har länge oroat OECD. Nu konstaterar man att situationen - trots allt - förblir stabil,

så länge det amerikanska underskottet kan finansieras och de asiatiska centralbankerna bygger upp reserver av dollar.

Johan Schück om OECD 29/11 2006 Klick

The Dollar Crisis:

Causes, Consequences, Cures,

R. Duncan

The next administration — whether it's McCain or Obama — will be forced to restore the Resolution Trust Corp., which was created in 1989 to dispose of assets of insolvent savings and loan banks.

The effects on the dollar, however, will be catastrophic.

Mike Whitney 6 June 2008

The RTC would create a government-owned management company that would buy distressed MBS from banks and liquidate them via auction. The state would pay less than full-value for the bonds (The Fed currently pays 85 per cent face-value on MBS) and then take a loss on their liquidation.

"According to Joseph Stiglitz in his book, Towards a New Paradigm in Monetary Economics, the real reason behind the need of this company was to allow the US government to subsidize the banking sector in a way that wasn't very transparent and therefore avoid the possible resistance."

There it is; a taxpayer-funded bailout of Biblical proportions looming on the horizon, possibly as soon as 2009. Ultimately, it is the only sure-fire way to stabilize the crumbling banking system and put a floor under housing prices.

Full text

The Savings and Loans Bailout

The Resolution Trust Corporation and Congress, 1989-1993

Top of page

Does the new dollar policy make sense?

June 3rd Ben Bernanke left no doubt that American officials did not want further dollar weakness.

The Economist print Jun 5th 2008

Full text

Mr Bernanke’s comments may be an effective way to send a coded message about monetary policy. They are unlikely, however, to have much effect on the currency. The US economy – especially the financial sector – remains vulnerable and so does the dollar.

Real, non-verbal intervention may yet be needed.

Financial Times editorial

Top of page

Why hasn’t dollar devaluation worked?

When the dollar last slumped, between 1985 and 1991, the US current account responded, moving from a deficit of 3 per cent of gross domestic product to a small surplus.

This time round, having been at 4 per cent of GDP in 2002, the deficit sat at 5 per cent in 2007.

FT Lex May 9 2008

Foreigners were happy to lend to the US, while Americans were happy to borrow against their houses in order to consume imported goods.

As the IMF points out, fundamental metrics suggest the dollar may have to fall further to get the US deficit into sustainable territory of under 3 per cent of GDP.

But with the culture of over-borrowing against overvalued assets exposed as a mug’s game, it would be a surprise if the US current account did not sharply improve from here.

Full text

Top of page

Free fall

There seems to be no floor for the dollar at the moment.

Mar 16th 2008 Economist.com

Full text

Två dramatiska besked på söndagskvällen fick investerarna att sänka den amerikanska dollarn.

En dollar kostar nu mindre än 6 kronor.

Dagens industri 17/3 2008

How did we get here?

To make a long story short: The process was started by money printing in America to bail out the last bubble.

Bill Fleckenstein, CNBC 4/6 2007

That induced money printing in much of the world because so many countries had linked their currencies to the dollar. More importantly, the very regions that were primed to grow -- think Asia, India and the Middle East -- exploded, in no small part, thanks to money printing. Thus, America's housing boom kept our economy growing. Growth in the other parts of the world I just mentioned, together with the attendant commodities boom, conspired to create the worldwide growth (and inflation) that we have experienced.

A lot of what's transpired has been a function of absurdly low interest rates, given the level of inflation around the world, and the collapse in risk premiums, aided by ratings-agency alchemy, which has allowed debt -- from moderately risky to total garbage -- to be spun into high-quality credit structures. In other words, the debt markets have acted as unindicted co-conspirators in the frenzy.

Full text

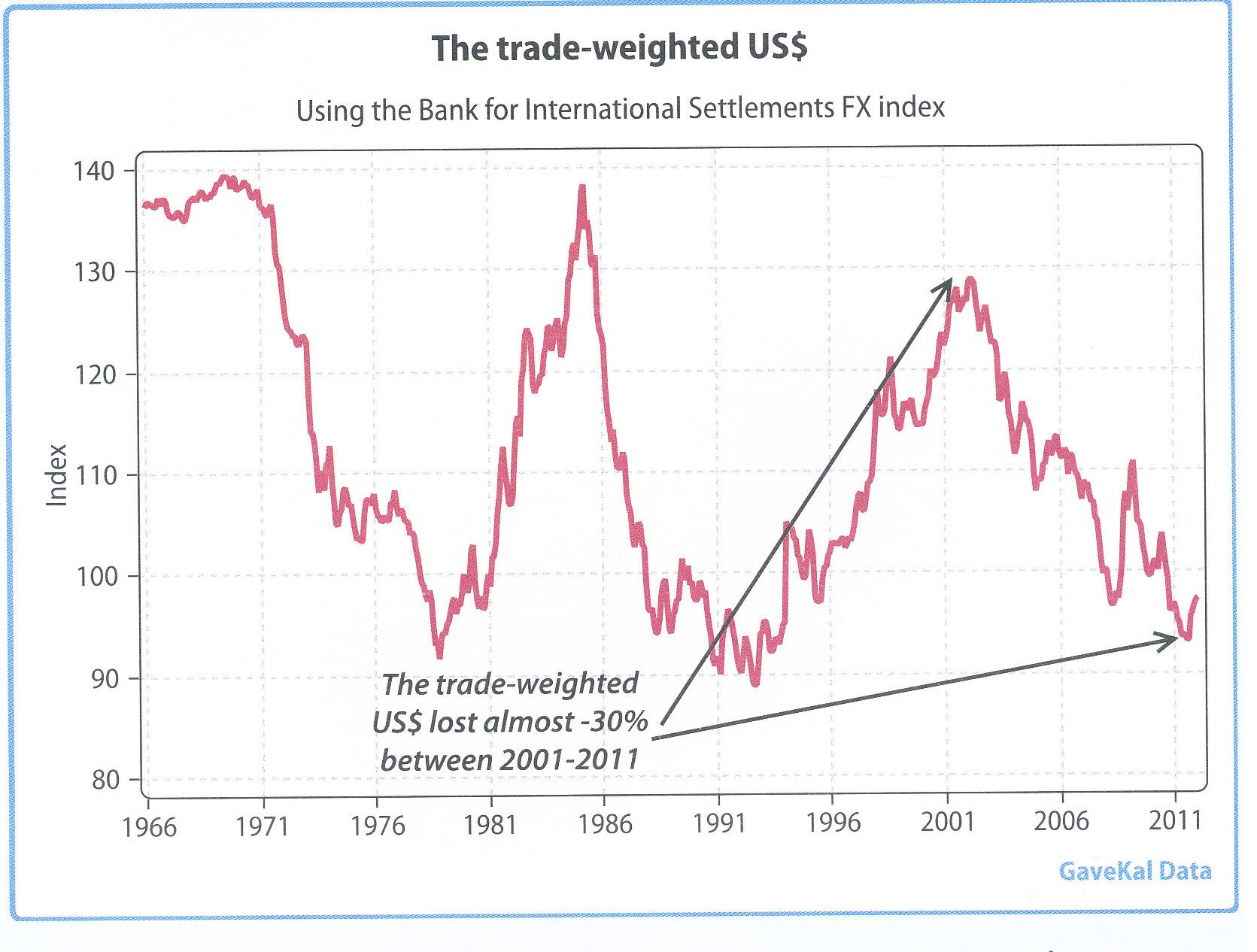

real trade-weighted exchange rate (the best measure of competitiveness)

The Economist print March 27th 2008

Since 1985 there have been five big examples of co-ordinated action: the Plaza Accord of 1985 to pull the dollar down; the Louvre Accord of 1987 to halt the dollar's slide; the joint intervention by America and Japan to halt the dollar's fall against the yen in 1995; and then to support the yen in 1998; and G7 action to support the euro in 2000.

Full text

Det var när dollarn sjunkit från 9:40 till 5:30 som Carl Bildt m fl till varje pris ville försvara kronkursen

Läs mer här och se diagrammet.

Dollar during 2007, CNN

From The Economist November 8th 2007

For more than a decade, Americans have been spending more and saving less. In June, people spent virtually everything they earned and saved almost nothing.

The government reported Tuesday that the nation's savings rate fell to a paltry 0.02%, the second-lowest monthly rate since the Great Depression.

Los Angeles Times 3/8 2005

A simple explanation of a big, big problem

Plaza Agreement in 1985 and Louvre Accord 1987

The Coming Collapse of the Dollar and How to Profit from It:

Make a Fortune by Investing in Gold and Other Hard Assets

Jim O'Neill, partner and head of global economic research at Goldman

won respect for prescient calls such as the one that accurately forecast that the euro would rise from $1.25 in February, 2004, to $1.30 a year later.

"He has been negative on the dollar since the late 1990s," - "He was initially wrong and then proved right."

Business Week

"The United States should just sit back — and enjoy the fall in the dollar."

(Jim O'Neill, Head of economics at Goldman Sachs, July 2002)

Top of page

news

Why the dollar stays steady as America declines

Eswar Prasad, a former IMF economist, points out in his new book The Dollar Trap, there is a paradox.

While common sense would say that these developments should have sparked a dollar crisis, precisely the opposite has occurred.

Against a trade-weighted basket of currencies, the value of the dollar is little changed from 2008.

Gillan Tett, FT 6 February 2014

Full text

Eswar Prasad

The Dollar Trap

Gillan Tett

Top of page

The dollar's perfect storm worsens

Europe's inflation is likely to prompt its central bank to raise interest rates

Jubak's Journal 4/12 2007

Top of page

The dollar has fallen by 36 per cent on the official trade-weighted index against major currencies

since its high point in 2002 and

by a sensational 41 per cent against the euro.

the imbalance problem has begun to fade away.

Samuel Brittan, FT November 8 2007

Problems are not so much solved as replaced by other problems. How many people remember that only a few months ago the main problem facing the world economy was supposed to be that of “imbalances”: the large current payments deficits of the US and a few other countries, offset by surpluses in China, Japan and the oil-exporting countries?

Since then, while all eyes have been on the bank credit crisis the imbalance problem has begun to fade away.

If the deficit countries are to reduce their deficits, they have to switch resources from home markets to exports or import saving activities. It would be lovely if this could be done painlessly without impinging on output and activity. But a substantial structural change of this kind does require some sort of domestic slowdown while resources are being switched.

The danger, in a nutshell, is that central banks and governments are so assiduous in promoting domestic growth that they will not tolerate a few quarters of lacklustre GDP performance.

It helps to remember that one object of monetary policy is to promote a reasonable, but not inflationary, growth of domestic demand. An approximation might be an objective for the growth of nominal GDP, which I have canvassed in the past but did not pursue, in view of a widespread lack of interest and the success, for a decade and a half, of the inflation target strategy.

Full text

Top of page

The dollar has finally begun its long overdue correction.

Its recent decline is just a prelude to the much more substantial fall needed to shrink the US current account deficit

Martin Feldstein, FT October 15 2007

The US current account deficit, running at a nearly $800bn (£393bn) annual rate, about 6 per cent of gross domestic product.

Even an unchanged trade deficit would require the rest of the world to buy $800bn of additional US debt over the next year, an amount that would grow in future years because of the rising interest payments on our external debt.

If foreign buyers do not want to keep acquiring US bonds at the current exchange rate, the dollar must fall enough to convince investors that it is unlikely to fall further or US interest rates must rise enough to compensate investors for the risk of holding dollar bonds.

The falling dollar should not be seen as a problem for the US economy. A more competitive dollar will raise net exports, reducing the probability that the current weakness will turn into an outright recession.

Full text

Martin Feldstein

Recession in 2007?

Top of page

IMF says dollar ‘overvalued’

FT October 18 2007

The International Monetary Fund said the greenback “remains overvalued” and rejected claims the euro had risen too far.

Contradicting Rodrigo Rato, the outgoing IMF managing director, who last week said “right now the dollar is undervalued”, the fund’s staff conclude the dollar is still too high.

Full text at FT

Annual Report of the Executive Board for the Financial Year Ended April 30, 2007

Top of page

If the US Treasury doesn’t think the dollar is overvalued,

can it also think that RMB is undervalued?

Brad Setser, Aug 23, 2007

The US – led by former Treasury Under Secretary Tim Adams and his deputy for IMF affairs Mark Sobel -- spent a lot of time trying to get the IMF’s surveillance to focus more on exchange rates. That was the right thing to do

But if the US government isn’t prepared to accept that the IMF’s assessment that the dollar is overvalued, China certainly isn’t going to accept the IMF’s assessment that the RMB is undervalued.

Full text

Top of page

The story right now is generalized euro strength, not generalized dollar weakness

The reasons why the US slowdown didn't lead to an improvement in the trade balance in the first quarter aren't that hard to find.

Brad Setser 27/4 2007

The de facto US-Chinese currency and monetary union has introduced a lot of distortions into the global economy. It is a strange monetary union. The faster growing portion of the monetary union has lower interest rates than the slower growing portion of the monetary union (because of expectations of RMB appreciation). And it has led the real exchange rate of the industrialized economy with the largest current account surplus to depreciate even as its economy booms ...

Full text

Top of page

Doomsday for the Greenback

Mike Whitney, Global Research, April 11, 2007

What is it that people don’t understand about the trade deficit? It’s not rocket science. The Current Account Deficit is over $800 billion a year. That means that we are spending more than we are making and savaging the dollar in the process.

Everyone agrees that the current trade imbalances are unsustainable and will probably trigger major economic disruptions that will thrust us towards a global recession.

It’s madness.

The trade deficit puts downward pressure on the dollar and acts as a hidden tax.

In fact, that’s what it is - a tax!

Every day the deficit grows, more money is stolen from the retirements and life savings of working class Americans. It’s an inflation bombshell obscured by the bland rhetoric of “free markets” and deregulation.

Consider this: In 2002 the euro was $.87 on the dollar.

Last Friday (4-6-07) it closed at $1.34 - a better than 50% gain for the euro in just 4 years.

Full text

Comment by Rolf Englund:

Nice roar, Mike, but I think You got one thing wrong.

Central Bank intervention by China and Japan cannot be called "bland rhetoric of “free markets” and deregulation".

Let's vote and let's float,

that is my philosophy

Why people don't understand

Rolf Englund, July 26 1999

Without cheap imports, CPI inflation will go through the roof.

If you think inflation is high now as you experience it when paying tuition,

insurance, or medical care bills,

wait until the U.S. tries to buy imports with depreciated dollars.

Eric Janszen I-Tulip 8/3 2007

RE: A lot of Nice Charts!

Full text

Monetarism

Cataclysm

Stagflation

Top of page

Consumer borrowing slowing down in December

Economists had forecast that total credit would rise by $8 billion and

instead it increased by $4.5 billion to $2.52 trillion.

CNN 7/2 2008

Consumer credit, as measured by the Federal Reserve, does not include any debt secured by real estate, such as mortgages or home equity loans.

Full text

Where have all the Boy Scouts gone?

December was the 21st month in a row that the savings rate came in negative.

Rob Peebles February 7, 2007

The economists, whoever THEY are, got it right in December. Incomes rose 0.5%, just as predicted. And spending rose by 0.7%, just as predicted. So, based on those numbers, consumers spent more than they earned, just as predicted.

A person might think correctly forecasting that an entire nation would spend more than it earned shows incredible foresight. But really the economists did nothing more than what they do best.

And no, that does not mean eating a free lunch in a fancy hotel while predicting that GDP will grow 3% next year.

Rather than taking a shot in the dark, they extrapolated a trend. There was a trend to extrapolate because December was the 21st month in a row that the savings rate came in negative.

Top of page

"tro inte att det värsta är över"

Tongångarna från männen som förutspådde finanskrisen,

Nouriel Roubini, Marc Faber och Peter Schiff,

har inte blivit muntrare.

E24 2009-09-30

"At every market peak.. you have excess liquidity.

At the present time a very significant part of what people call excess liquidity comes actually from the American current account deficit".

That 800 billion dollars flows around the world and boosts economic activity.

Marc Faber at Michael Shedlock 1/3 2007

Full text

Top of page

The recent flurry in foreign exchange markets probably signals the start of a process of unwinding global imbalances. Suppose the market brings about the requisite dollar depreciation.

Then, if China and Japan were to maintain their dollar exchange rates there would be a large effective appreciation of the euro with potentially devastating effects on Europe.

Vijay Joshi, FT 15/12 2006

Alan Greenspan said he expected the dollar to stay weak for the next few years and will continue to drift down

"I expect that the dollar will continue to drift downwards until there will be a change in the U.S. balance of payments"

Reuters 11/12 2006

In looking to 2007, my main message is to be wary of extrapolation.

When a booming sector goes bust - dot-com six years ago, housing today - there are no built-in firewalls that contain the ripple effects. The US soft-landing scenario does not adequately allow for these risks, in my view.

Stephen Roach, 11/12 2006

Our US team now concedes that America has lapsed into a temporary "growth recession" -- econo-speak for a growth rate that is sluggish enough to allow the unemployment rate to start rising again

Only asset-driven wealth effects can explain how a decade of frothy consumption growth (3.7% in real terms) has exceeded after-tax real income growth (3.2%) by an average of 0.5 percentage point per year.

In the globalization debate I suspect that the focus is likely to shift away from the brilliant successes of China and India toward an increasingly politicized pro-labor pushback from the rich countries of the developed world.

The income shares of the major industrial economies are all at extremes - record high returns to capital and record lows for labor shares.

A pro-labor shift in the political power base of the industrial economies -- already evident in the US, Germany, France, Italy, Spain, Japan, and possibly Australia - could lead to a reversal of these trends.

Full text

More by Stephen Roach

The eurozone may boom until hit by the combined force of higher interest rates, a higher exchange rate and possibly lower global equity prices.

The optimists will be right until they are wrong.

I am not sure this scenario is any less likely than the optimists’ case, according to which global imbalances either never adjust or adjust in a benign way.

Wolfgang Munchau, FT 11/12 2006

As far as the global environment is concerned, the optimists may turn out to be right once again – they have been right for some time now. What we do know is that global imbalances will adjust one day and that such an adjustment would almost certainly be accompanied by a devaluation of the dollar. If that adjustment came about quickly, for example through an economic downturn in the US, it would undoubtedly reduce world economic growth. Of course, we have no idea when or how it will occur. In other words, the optimists will be right until they are wrong.

The case of the pessimists is intellectually more persuasive. While the timing of the adjustment is impossible to predict, it is certain it will eventually happen.

Once it happens, the eurozone will take the full brunt of this adjustment. While the eurozone trades less with the US even than with the UK, a significant devaluation of the dollar would normally leave the euro also strengthened against third currencies, especially from Asia.

Full text

More by Wolfgang Munchau

U.S. Trade Deficit:

If something cannot go on forever it will stop

Rolf Englund 2001

Top of page

Aldrig får man vara riktigt glad

The dollar initially jumped after the Labor Department said the U.S. economy added 132,000 jobs in November, above economists' expectations. That advance stalled, however, as investors focused on a sharp downward revision for the number of jobs created in October

Reuters 8/12 2006

China's surplus is dwarfed by those of oil-exporting emerging economies, which are expected to total $500 billion.

These surpluses are having a huge impact on international capital flows; and they may, unless the right policy prescriptions are applied, undermine efforts to unwind global imbalances in an orderly way.

The Economist 7/12 2006

China is at last moving slowly towards a more flexible exchange-rate, the currencies of Saudi Arabia, Kuwait, the UAE and most other Gulf economies are still firmly pegged to the dollar

The dollar peg means that, as the price of oil has soared, those currencies' real trade-weighted exchange rates have, perversely, fallen. This is pushing up inflation and stoking asset-price and credit bubbles in their domestic economies. Pegging those currencies to the weak dollar also dampens demand for imports in their economies, and thus hinders the rebalancing of global current accounts. Higher levels of both imports and government spending by the oil-producing countries would help unwind the imbalances that endanger the world's economic stability.

Full text

End of the Oil Era

Richard Nixon’s Treasury secretary, John Connally, famously remarked that "the dollar is our currency, but your problem".

US exports are also at last growing at roughly the same rate as imports

Martin Wolf, 6/12 2006

Rolf Englund: Observera att senast USA hade balans i handeln var

det händelserika året 1992...

US exports are also at last growing at roughly the same rate as imports: between the third quarter of 2003 and the third quarter of this year exports of goods and services grew 27 per cent, in constant prices, while imports rose 26 per cent.

Full text

Comment by Rolf Englund:

Because the U.S. imports about 50 percent more goods and services than it sells abroad, exports have to grow about twice as fast just to stabilize the deficit.

John Connally

Wikipedia

On November 22, 1963, he was seriously wounded while riding in President Kennedy's car in Dallas, when the president was assassinated. Connally does not endorse the conclusions of the Warren Commission. When asked if he believed the Warren Commission's findings he said: "Absolutely not.

I do not, for one second, believe the conclusions of the Warren Commission."

Rolf Englund:

Connolly hade varit marinminister och därvid avslagit Lee Harvey Oswald överklagande

av sitt vanhedrande avsked ur Markinkåren. Det var kanske Connoly som Oswald siktade på och inte JFK?

Top

The waning dollar and a not-so-brave new world

As the prospect of the pound costing $2 edges closer, it is worth looking back to the early 1980s when we last explored such remote exchange rate territory.

John Plender, FT 4/12 2006

Yet stability cannot be taken for granted. Mervyn King, the governor of the Bank of England, highlighted last week how low levels of long-term interest rates have boosted asset prices and helped sustain global demand. The biggest risk to the world economy, he argued, lies in a rapid rise in real rates prompting a nasty correction in all asset prices.

With US demand exceeding domestic income by 7 per cent – the current account deficit – asset values and household debt would have to rise forever in relation to incomes to keep growth on trend. That really would be a brave new world, and as real as Prospero’s island, where Shakespeare’s Miranda coined the phrase.

Full text

More by John Plender

Comment by Rolf Englund:

Stein's Law: If something cannot go on for ever it will stop.

Top of page

Börsen faller -

dollarn på lägsta nivån sedan mars 2005

De amerikanska inköpscheferna är mer pessimistiska än väntat vilket fick både dollarn och Stockholmsbörsen på fall.

DI 1/12 2006

The main reason for the dollar's strength has been the widespread belief that the American economy vastly outperformed the world's other rich-country economies in recent years.

But the figures do not support the hype.

Contrary to popular perceptions, America's economy has not significantly outperformed Europe's in recent years.

The Economist 30/11 2006

Sure, America's GDP growth has been faster than Europe's, but that is mostly because its population has grown more quickly too.

productivity growth over the past decade has been almost the same in the euro area as it has in America. Even more important, the latest figures suggest that, whereas productivity growth is now slowing in America, it is accelerating in the euro zone.

So, contrary to popular perceptions, America's economy has not significantly outperformed Europe's in recent years.

America's growth, thus, has been driven by consumer spending. That spending, supported by dwindling saving and increased borrowing, is clearly unsustainable; and the consequent economic and financial imbalances must inevitably unwind.

Does a falling dollar, with its implications of American weakness, spell doom for the rest of the planet? Not necessarily.

Full text

"USA har ryckt åt sig ett stort försprång och har världens mest framgångsrika ekonomi"

Klas Eklund på SvD:s ledarsida 2000-08-11

Sterling hit its strongest level against the dollar in 14 years on Thursday as traders continued to put pressure on the beleaguered US currency.

The pound its highest level against the greenback since its ejection from the European Exchange Rate Mechanism in September 1992.

FT 30/11 2006

16 september 1992:

England låter pundet flyta och lämnar ERM

The crowd that has long believed the greenback needs to be devalued because of the large U.S. trade deficit is declaring that day has finally arrived.

Our view is simpler: When U.S. economic policies look like they might take a turn for the worse, dollar-denominated assets lose some of their allure

Wall Street Journal editorial 29/11 2006

The jury is still out on the Federal Reserve's resolve to correct its inflationary easy-money blunder of 2003-2005.

Full text

Alan Greenspan

The US may be able to cope with a fall in the dollar.

Its debts are denominated in its own currency, and while rising import prices could push up inflation, foreign firms tend to price to keep their share of the US market. But if the dollar falls further, the economy will have to rebalance to-wards exports and away from consumption. That is a necessary process. But the worry is whether America's exporters, battered by years of foreign competition, would be able to do so quickly.

If they cannot, the US could suffer a recession while it adjusts.

FT editorial 28/11 20006

France's prime minister Dominique de Villepin:

"Let us equip ourselves with a real exchange-rate strategy which integrates the objectives of growth, protection of our industry and, of course, employment. It is a major subject which we should address at European level."

Wall Street Journal 15/11 2006

Month in and month out I keep reading article after article on how to fix the global economy.

Let's take a look at two of the recent ones.

Michael Shedlock, 12/10 2006

The 1985 Plaza Accord precipitated an appreciation in the yen that eventually led to an asset bubble in Japan that burst in the early 1990s, leading to a 15-year period of lackluster growth during which the world's second-largest economy had three recessions.

Plaza Accord

The Fed does not have control over money supply. For that matter the Fed does not really control interest rates either (except at the short end, and only if the market is willing to oblige). In fact, the Fed is not really in control of much of anything and Hussman talks about it in Superstition and the Fed and Independent Thought.

John P. Hussman, Ph.D.: It continues to astonish me how much power investors appear to ascribe to the Federal Reserve. The institution can do nothing but purchase debt (mainly U.S. Treasuries) and pay for it by creating bank reserves, or sell debt and receive payment by reducing bank reserves. When you realize that the total volume of bank lending has virtually no link at all to bank reserves (since the majority of monetary aggregates other than checking accounts have had zero reserve requirements since the early 1990's), and that foreign purchases of U.S. Treasuries have swamped Fed activity in Treasuries three-to-six times over in recent years, this whole focus on every word, syllable, and inflection from the Federal Reserve is just preposterous.... more

How long can the global economy endure America's enormous trade deficits or China's growing trade surplus of almost $500 million a day?

- the United States borrows close to $3 billion a day -

Joseph E. Stiglitz, Herald Tribune, October 3, 2006

Joseph E. Stiglitz, a professor of economics at Columbia University and the author, most recently, of "Making Globalization Work," was awarded the Nobel in economic science in 2001.

China knows well the terms of its hidden "deal" with the United States: China helps finance the American deficits by buying Treasury bonds with the money it gets from its exports. If it doesn't, the dollar will weaken further, which will lower the value of China's dollar reserves (by the end of the year, these will exceed $1 trillion).

Underlying the current imbalances are fundamental structural problems with the global reserve system.

John Maynard Keynes called attention to these problems three-quarters of a century ago. His ideas on how to reform the global monetary system, including creating a new reserve system based on a new international currency, could, with a little work, be adapted to today's economy. Until we attack the structural problems, the world is likely to continue to be plagued by imbalances that threaten the financial stability and economic well-being of us all.

These imbalances simply can't go on forever.

Full text

Stein's Law:

If something cannot go on for ever it will stop.

John Maynard Keynes

A slump in the US economy is bad for everyone

Wolfgang Munchau, Financial Times August 13 2006

Countries such as Germany and Italy are structurally hooked on exports and suffer from an underdeveloped services sector. This makes it difficult for them to switch from exporting tradeable goods to the production of non-tradeables.

The present eurozone recovery is based on export-led growth that resulted in more investment and consumer spending after some delay. The recovery appears relatively robust, but suppose the euro’s exchange rate overshot against the dollar as part of a rebalancing of the US current account deficit?

Second, monetary policy would not come to the rescue either. While US interest rates may soon be heading downwards, European rates are still on their way up.

What about fiscal policy? Here, the news is a little better. It is a common misunderstanding that the stability and growth pact acts as an artificial constraint. If the eurozone contracted, governments would be able to run public sector deficits at more than the agreed 3 per cent of gross domestic product.

The real constraint is the level of debt in some eurozone countries. Italy, for example, with a debt-to-GDP ratio of about 106 per cent, would face difficulties running an expansionary fiscal policy for more than short periods.

Another problem is time lag: in many countries, the political systems take so long to enact and implement fiscal policy measures that their economic effects are only felt after the recession is over.

The unpalatable truth is that a slump in the US economy is bad news for almost everyone.

Stability Pact

Europe has to face threat of US trade deficit

This cumulative process could be enough to send some European economies into recession.

Martin Feldstein, FT August 1 2006

The inevitable decline of the US trade deficit will pose a big challenge for the economies of Europe. Shrinking America’s $800bn annual trade imbalance requires a decline of US imports and a rise in its exports. When US imports decline, European exports will fall; and when a lower dollar makes American exports more competitive, US shipments to Europe will rise and American products will replace European goods in global markets.

This fall in the demand for European products will cause a slowdown in Europe’s already weak growth. With lower demand, European companies will invest less and hire fewer workers. The resulting slowdown in incomes will hurt consumer spending and have second-round effects on business investment. This cumulative process could be enough to send some European economies into recession.

With this separation of monetary and fiscal responsibilities, there is virtually no feedback from larger budget deficits in the form of higher interest rates and a weaker currency that would otherwise discipline fiscal authorities. The revision of the growth and stability pact only exacerbates this problem by substantially weakening the Maastricht treaty that required eurozone countries to limit their fiscal deficits and national debt.

Full text

Cataclysm

Stability Pact

More by Martin Feldstein

Record exports of farming goods helped to narrow the US trade gap in June

June's deficit dipped 0.3% to $64.8bn. Imports also hit record levels.

The trade gap for 2006 looks set to surpass last year's record of $716.7bn, as the annual rate is running at $768bn.

BBC 10/8 2006

The US Trade Deficit climbed by just $500m to $63.8bn in May.

This was despite a $4.4bn increase in the deficit on petroleum products

Excluding petroleum, the deficit shrank from $42.3bn to $38.4bn.

BBC 12/7 2006

2.4 per cent increase in exports to $118.7bn

Imports rose 1.8 per cent to a record $182.5bn.

Top

Global imbalances are not sustainable in the long run, Federal Reserve Governor Donald Kohn said Thursday,

but adjustments to the current account deficit are "not likely to be disruptive,"

although the Fed cannot rule out sharp price increases during an unwinding period.

Wall Street Journal 6/7 2006

"we certainly cannot rule out the possibility of further sharp asset price movements as product prices and spending adjust," Mr. Kohn added.

Mr. Kohn said strong demand for dollar denominated assets is critical to keep any unwinding smooth and non-disruptive.

Top

A soft landing means sustained $1 trillion plus (7% of GDP) current account deficits

Brad Setser, June 27, 2006

The following graph shows what happens if the pace of import and export growth moderate a bit – and both retreat to their long-term averages. As a result, the expansion of the US trade deficit slows. But the expansion of the US current account deficit doesn’t slow. Existing debts get repriced at higher interest rates as they come due. And borrowing $1 trillion a year at 5% plus starts to add up.

US has a different external vulnerability. With gross debts of nearly $8.6 trillion at the end of 2005 – nearly 70% of US GDP (the end 2005 estimate is mine; the formal data will be out soon) and an estimated 2005 net international investment position of around $3.2 trillion (25% of GDP), the US is increasingly vulnerable to an interest rate shock.

Full text

Top

The Leverage in the System and the Weak US Dollar

By GaveKal Research, at John Mauldin, 26/6 2006

Top of page

USE/EUR

Top

A year from now the dollar will almost certainly be stronger than it is today

Anatole Kaletsky, The Times 18/5 2006

What, then, is the real trouble? The answer is much less abstract. In fact, it can be reduced to just two names: Ben Bernanke and George W. Bush.

I am convinced that the Fed will eventually pass this test, that any US inflation scare will turn out to be a minor hiccup and that the dollar will, in time, re-establish itself as the most trusted currency in the world. A year from now the dollar will almost certainly be stronger than it is today against the euro and the pound and gold will be valued again for its usefulness in dental fillings, rather than its monetary magic. But first, investors will have to be persuaded of the Fed’s ability to control US inflation — and of Professor Bernanke’s ability to control his words.

Full text

Top of page

Den svenska budgetsaneringen på

90-talet komma att te sig enkel

jämfört med den kris som

nästa amerikanska president, eller kanske redan George Bush,

kommer att tvingas ta itu med.

Stefan de Vylder, Socialpolitik, nr. 4/2006

Misery Index, Mark II, could help explain why US inflation is so low

To get an easily understood measure of the underlying inflation you could add the inflation rate to the trade deficit.

Rolf Englund, Financial Times 22/6 2006

Sir, While reading Wolfgang Munchau's interesting article "Why they take the strawberries out of the basket" (June 19), about problems with correctly measuring the underlying inflation, I came to think of The Misery Index, initiated by the Chicago economist Robert Barro in the 1970s. As we perhaps remember it is simply the unemployment rate added to the inflation rate. Perhaps a similar Misery Index, Mark II, could help us understand why the recorded US inflation is so low.

In a closed economy, when you spend 107 per cent of gross domestic product you will get inflation of perhaps 7 per cent. In an open economy you might get price stability and a 7 per cent trade deficit. So to get an easily understood measure of the underlying inflation you could add the inflation rate to the trade deficit.

If something cannot go on for ever, it will stop, as Herbert Stein once wrote. When the dollar drops to a level consistent with a trade balance of zero, General Motors and Ford will probably survive, and cars, among other things, will be more expensive, and the recorded inflation rate will rise. If you think The Misery Index, Mark II, is too easy, think of Misery Index, Mark I.

Text at Financial Times

More by Rolf Englund in Financial Times

Kommentar av Stefan de Vylder:

Enkelt, skoj och smart!

Ditt index påminner mig om hur jag en gång under 90-talskrisen konstruerade ett nytt index (som dock aldrig slog igenom). Det du kallar Misery Index kallades ofta "Discomfort Index", DI. Mitt index kom att heta GADI - "Growth-Adjusted Discomfort Index".

Från summan av öppen arbetslöshet och inflation subtraherade jag helt enkelt BNP-tillväxten. Det var först då man verkligen såg djupet i 90-talskrisen. Under 90-talets första år var ju inflationen hög, och arbetslösheten låg - efter 1992 blev det tvärtom, varför DI inte påverkades alls; upp- och nedgång tog helt enkelt ut varandra. Men med hjälp av GADI var det lätt att se uppgången i eländesindexet. Om vi i slutet av 80-talet och början av 90-talet även hade tagit med bytesbalansunderskottet hade vi ånyo fått högre index dessa år, vilket givetvis hade markerat att krisen efter 1992 hade grundats under de föregående åren.

Slutsats: enkla index är bra, men bör hanteras med stor försiktighet eftersom de så lätt kan missbrukas. Varje regering som vill skylla ifrån sig kan välja det index som bäst passar syftet.

RE: Se även:

En gemensam räntepolitik i ett valutaområde innebär med nödvändighet att räntan blir för hög i vissa länder - de som behöver stimulera ekonomin - och för låg i andra. Detta helt oberoende av hur väl den europeiska centralbanken sköter sitt jobb.

Det faktum att den nominella räntan är gemensam i en valutaunion innebär dessutom automatiskt att realräntan blir lägst i de länder som har den högsta inflationen, det vill säga de som skulle behöva en hög ränta, och högst i de länder som skulle behöva stimulera ekonomin. En inbyggd perversitet.

Stefan de Vylder, Göteborgs-Posten 2002-10-22

Top

Asking about the implications of a dollar collapse is a different ball game from predicting its likelihood or timing.

Instead of hopeless crystal ball gazing we can ask what this event would mean and what kind of policies should be adopted in response.

Samuel Brittan, Financial Times, 16/6 2006

I will be forgiven for beginning with a relatively benign scenario.

The most likely trigger for a dollar collapse would be a US housing market setback, which would deliver a blow to US consumer spending. The Federal Reserve would then pause in, or even reverse, its present policy of gradually raising short-term interest rates.

If the world is experiencing excess demand, as the pressure on oil and commodity markets and the abundance of credit suggest, a modest recessionary movement in the US might be just what the doctor ordered.

It follows from this that if there is to be a dollar crash the sooner the better.

Full text

How do we get out of this scenario alive?

Rolf Englund, Financial Times 4/10 2005

Top

Martin Feldstein:

The U.S. savings rate has been falling for decades. But that downward trend will likely soon be reversed.

It could cause serious problems for the United States and its trading partners unless they start preparing immediately.

Foreign Affairs, May/June 2006

The U.S. savings rate has been falling for decades. But that downward trend will likely soon be reversed, as factors such as rising mortgage interest rates force Americans to start saving more. The change will ultimately be for the better, but in the short term it could cause serious problems for the United States and its trading partners unless they start preparing immediately.

Read more here

Det går bra för Sverige just nu, med mer än fyra procents tillväxt. De nya BNP-siffrorna för årets första kvartal visar på en snabb tillväxt i ekonomin, som troligen fortsätter ett tag till.

Längre fram kan diskussionen om hur bra det just nu går för Sverige framstå som aningslös och oansvarig.

Johan Schück, DN 10/6 2006

Top

The biggest single problem, however, is that there are trillions of U.S. dollars outside of the U.S. Unlike Americans, foreigners have no reason to hold them. And at some point very soon, perhaps when the Fed finally hits the wall on its ability to raise rates, these overseas dollars are going to start flooding back home, while the products and titles to real wealth flow out of America. Therefore, when the trade deficit starts turning around--which most people will think is a good thing--that will be the real tip-off the game is over. Trillions coming back to the U.S. will skyrocket long-term interest rates and inflation. The dollar will go into freefall.

Doug Casey, 13/6 2006

Top

- Det behövs en anpassning där dollarkursen försvagas

Men denna förändring kan komma successivt. Sannolikheten för ett plötsligt dollarras har minskat, säger Stephen Roach.

Jag är optimist om Kina, som gradvis kommer att lägga om sin politik. Kinesernas långsiktiga intresse är bygga upp sitt eget land, inte att köpa amerikanska statsobligationer.

Johan Schück, DN 1/6 2006

Top

One danger area - shared by his Bush predecessors at Treasury and some in the White House - may be his willingness to fall for the temptation of a weaker dollar.

In the 2004 PBS interview, Mr. Paulson said that "I really believe that the decline in the dollar, the orderly decline in the dollar, will lead to a natural adjustment" in the trade deficit.

Wall Street Journal 31/5 2006

Resolving the massive trade imbalances without a global cyclical downturn can be achieved,

but only if countries approach this challenge in a constructive way.

Instead of seeking to resist the dollar’s shift to a more competitive level, governments in Europe and Asia should focus on developing policies to maintain aggregate demand in their individual economies as their export sales decline.

Martin Feldstein, Financial Times 26/5 2006

Bernanke’s Sophie's Choice:

"The housing market or stock market Mr. Bernanke. You may only be able to try and save one..."

Brady Willett, May 18, 2006

OECD warns on global imbalances

Opening the global think tank's annual forum, Greek finance minister George Alogoskoufis said that the situation posed major risks to global economic stability.

"The large extent of deficits of some countries, combined with the surpluses of their trade partners and the oil-producing countries, can pose considerable risks to global economic stability, so it is crucial that we do something about them," Mr Alogoskoufis said.

BBC 22/5 2006

Markets have recently become worried that the growing US trade gap is unsustainable, and there is concern that a sharp fall in the dollar to boost US exports would unravel Europe's tentative economic recovery.

There is also concern that the US budget deficit is unsustainable in the long-term, and that tax increases are needed both to balance the budget and reduce US consumers' insatiable demand for foreign goods.

Full text

Kan man undvika recession i USA när man måste minska importen

med 600 miljarder dollar?

Rolf Englund på Nationalekonomiska Föreningen 30/11 2004

The market is gripped by two scares: an inflation scare and a dollar scare.

Of the two scares, investors should worry less about US inflation and more about the dollar (though the two are obviously related).

Financial Times editorial 20/5 2006

Huvudfrågan kvarstår: vad händer när USA tvingas minska sitt underskott mot omvärlden, om inte överskottsländer - som Sverige - är beredda att ta ett större globalt ansvar?

Ingen centralbank, varken i USA eller någon annanstans, är villig att släppa fram en snabbt stigande inflation. Hellre låter man ekonomin gå in i en tillfällig svacka, även om den skulle övergå i recession

Johan Schück, DN Ekonomi 20/5 2006

The weak state of the dollar feeds fears of inflation.

Currency trading on Friday and Monday saw the dollar dip below ¥110—the level

below which Hiroshi Okuda, the chairman of both Toyota and the Japan Business Federation, recently said the government might have to intervene in the currency market.

It has also been flirting with one-year lows against the euro.

The Economist 17/5 2006

And even China, which has historically kept its currency cheap in order to subsidise exports, is showing signs that it is ready to let the yuan appreciate. News released on Tuesday that America’s housing market is weaker than expected pushed the dollar down further. Though expectations for higher inflation—and thus interest rates—have stemmed some of those losses, it is still trading near one-year lows.

A weaker currency would help America’s current-account deficit, which currently stands well above $800 billion, but it would also translate into inflationary pressure at home, by raising the price of imports.

This week we look at the links between the US trade deficit, the low savings rate in the US, home prices, and interest rates, all in an effort to answer the question: "Do trade deficits matter?"

"Deficits of US$800bn are perfectly sustainable, not just for many more years and decades but, if necessary, forever."

John Mauldin (An essay by Anatole Kaletsky) 12/5 2006

Charles and Louis-Vincent Gave, along with colleague Anatole Kaletsky answered in their book, Our Brave New World, that trade deficits do not in fact matter at all. It is different this time. They make a persuasive argument that the US trade deficit can last forever and that the deficit is in fact a sign of US strength, not weakness.

"This is one point which almost all economists and policymaking institutions - the Fed, the IMF, the OECD - all absolutely agree on: even if the US deficits were perfectly harmless or even desirable, they would soon have to be narrowed, because borrowing $800 billion a year is simply unsustainable. What I now want to tell you is that all these distinguished experts are exactly wrong.

"I cannot be sure whether the present US deficits are a good or a bad thing; but on their sustainability there is absolutely no doubt. Deficits of US$800bn are perfectly sustainable, not just for many more years and decades but, if necessary, forever. This is a matter of simple and irrefutable arithmetic.

Full text

Analysts said that US policymakers are signalling they are happy for the dollar to decline by not aggressively talking up the currency.

A falling dollar would benefit the US economy by making US exports cheaper. That could help reverse the $700bn trade deficit.

BBC 15/5 2006

The dollar's fall could also increase the cost of US imports, thus fanning inflation and forcing the Fed, the US central bank, to continue to increase interest rates.

Figures last week showed that the total US trade deficit for the first three months of 2006 was $196.2bn, putting it on track to beat last year's record of $724bn.

Top of page

The US dollar suffered a severe sell-off on Friday, taking it to its

weakest level against a trade-weighted basket of currencies since

October 1997, in a tumble that helped to trigger falls across world

equity markets.

The dollar ended at $1.293 to the euro

Financial Times May 12 2006

US government bonds also suffered, bringing the yield on the benchmark

10-year bond to its highest level in four years.

The dollar has lost 7 per cent against the euro, yen and sterling since

the start of April – a slide that will in turn intensify worries about

inflation in the economy. Traders are concerned about the role a weaker

dollar will have in correcting the US current account deficit, which is

now about 7 per cent of GDP.

In New York, the dollar ended at $1.293 to the euro and at $1.894

against sterling. Against the yen, it stood at Y110.02. Traders thought

a correction was likely.

Full text

The Stock Market

Let dollar fall or risk global disorder

Is it possible to reduce the US deficit substantially without exchange-rate changes. The answer is that it would be possible, but catastrophic for all participants, because it would demand a deep US recession

Martin Wolf, Financial Times, May 9 2006

The biggest threat to what was otherwise an “unusually favourable” economic environment

The International Monetary Fund on Wednesday stepped up the pressure for far-reaching shifts in exchange rates, declaring that the dollar will have to depreciate “significantly” over the medium term if global economic imbalances are to be resolved in an orderly fashion.

Financial Times 19/4 2006

By Krishna Guha and Scheherazade Daneshkhu

In its clearest statement to date on this highly-charged subject, the IMF said it was essential that currencies in Asia and of oil exporters were allowed to appreciate as part of the required “realignment of exchange rates”.

The statement came in the IMF’s twice-yearly World Economic Outlook, published on Wednesday, which highlighted global imbalances as the biggest threat to what was otherwise an “unusually favourable” economic environment.

Full text

By Martin Wolf, Financial Times April 19 2006

Many in the US Congress blame China for their country’s huge and growing current account deficits. While the US economy is expanding strongly, protectionist pressure is contained. But what will happen during the next downturn? As Harvard university’s Martin Feldstein has also noted recently, such a downturn is hardly unlikely, since only exceptionally low savings and high borrowing by US households have sustained US domestic demand at levels sufficient to offset the country’s huge trade deficits.

The Case for a Competitive Dollar, www.nber.org

Why is the only workable solution a multilateral one? The first part of the answer is economic: the global balance of payments is inherently multilateral. Even if one focuses, wrongly, on bilateral balances, the US deficit with mainland China accounts for only a quarter of its overall deficit. In the global picture, we find that China’s current account surplus was roughly a sixth of the aggregate surpluses of oil exporters and advanced economies (other than the US) in 2005.

Full text

Top of page

Market interest in global imbalances waxes and wanes but the economic facts do not change. The US current account deficit is unsustainable in the long run.

To reduce it to manageable proportions by means other than a global recession will require macroeconomic policy changes on the part of surplus countries as well as the US itself.

These will have to be accompanied by big shifts in real exchange rates to alter the relative prices of imports and exports, traded and non-tradeable goods

Financial Times editorial 13/4 2006

To focus narrowly on China is misleading: the increase in its surplus since 1996 is about one-sixth the increase in the US deficit.

Other Asian economies show consistent big increases in reserves, too. These countries need to tackle far more urgently the domestic causes of external imbalances while allowing greater currency flexibility.

This would not eliminate the need for painful changes in the US, including a substantial rise in national savings. But it would provide the best possible global environment for such a necessary adjustment.

Full text

Top of page

Sveriges bytesbalansöverskott är lika stort som USA:s underskott

Enligt ett diagram hos Danne Nordling april 2006

Läs mer här

Many observers - including myself and the IMF - predicted in 2004 and later that high oil prices would lead to a U.S. and global economic slowdown; but such a slowdown actually did not actually materialize.

http://www.rgemonitor.com/blog/roubini/123823

Current-account deficits

Still waiting for the big one

Today Iceland and New Zealand. Tomorrow the United States?

The Economist print edition, Apr 6th 2006

When average interest rates in the developed world fell to a record low earlier this decade, investors wanted extra yields. They took bigger risks, dragging down risk premiums. Cheap money attracted capital into “carry trades”, where investors borrow short-term at low rates to invest in riskier, higher-yielding bonds, such as those issued by Iceland and New Zealand—or the American Treasury. By underpricing risk, investors have, in effect, subsidised extravagant borrowers, letting them run ever bigger deficits. A correction may be under way.

As yet, the greenback is little affected by Iceland and New Zealand—and not only because they are small. Money is still cheap. The Bank of Japan has ended its “quantitative easing”, but interest rates are still zero. America's bond markets have gained most from the yen carry trade (borrowing in cheap yen to buy American T-bonds), so future increases in Japanese interest rates will spur investors to ask if historically low yields still compensate for the risk of holding dollar assets. This week ten-year T-bonds were nudging 4.9%, up from 4.4% in January.

Full text

Carry trade - Räntearbitrage