SIV = structured investment vehicle

News Home

Home - Index - News - Krisen 1992 - EMU - Economics - Cataclysm - Wall Street Bubbles - US Dollar - Houseprices

Foreclosures

Some 5.6m US home loans are at least three months in arrears on payments

FT January 23 2011

But the most visible “crops” sprouting up these days are For Lease or foreclosure signs in the real estate market.

CNN September 2, 2010

"There has been an effective moratorium on foreclosure," said Roubini.

CNBC 28 Dec 2010

And the beginning of the end of that moratorium means more housing supply is about to become available on the market.

"The shadow inventory of not-yet-foreclosed homes—due to the moratorium—will surge in the next year," Roubini says.

Both factors, taken in concert, set up a scenario where market fundamentals put downward pressure on prices: "Supply will increase, demand will drop," Roubini said.

One of the foreclosure cascade's not-so-hidden secrets is that the banks and investors who hold millions of busted mortgages are in no hurry to kick debtors out of their homes.

The average homeowner in foreclosure now is an amazing 461 days behind in his payments.

CNBC 28 Aug 2010

The markets hardest hit by the foreclosure crisis are already stuck with an enormous and growing inventory of repossessed houses, now estimated by Lender Processing Services, which tracks foreclosures, at 1 million to 1.2 million bank-owned homes nationwide.

Banks have steadily slowed down the foreclosure process: The average homeowner in foreclosure now is an amazing 461 days behind in his payments.

Force me out if you can.

A growing number of the people whose homes are in foreclosure are refusing to slink away in shame.

They are fashioning a sort of homemade mortgage modification, one that brings their payments all the way down to zero.

NYT 1 Jun 2010

Foreclosure procedures have been initiated against 1.7 million of the nation’s households. The pace of resolving these problem loans is slow and getting slower because of legal challenges, foreclosure moratoriums, government pressure to offer modifications and the inability of the lenders to cope with so many souring mortgages.

The average borrower in foreclosure has been delinquent for 438 days before actually being evicted, up from 251 days in January 2008, according to LPS Applied Analytics.

America slides deeper into depression

The home foreclosure guillotine usually drops a year or so after people lose their job, and exhaust their savings.

One million American families lost their homes in the fourth quarter.

Ambrose Evans-Pritchard 10 Jan 2010

Diana Olick

Realty Check

Articles at CNBC

Given the combination of the expiration of the home buyer tax credit

and the increasing number of loans moving to final foreclosure,

we knew that home prices overall would take a hit, but it would take a while.

Well we're here.

Diana Olick, CNBC Real Estate Reporter, 15/9 2010

Twenty-six percent of sellers on the market in August, according to Trulia.com, had lowered their expectations, and hence their prices.

Sellers on the market today have cut $29 billion off their collective home equity.

Webmaster Rolf Englund: Diana Olick is one of my economic Gurus.

Click here for more of my Gurus.

Home Sellers Slashing Prices, While Banks Mow the Lawn

CNBC 14 Jul 2010

"People are sitting in their houses not paying their mortgages, and the banks are letting those delinquencies extend longer and longer periods of time before they put them in foreclosure,"

That, he adds, is the main reason we're seeing lower numbers of new defaults.

The borrowers are in default, but the banks aren't paying attention, so they don't show up in the numbers.

Diana Olick 13 may 2010

Realty Check takes you from the housing boom to bust and beyond. Led by Diana Olick, we were here when the house came crashing down and we have the singular expertise to explain how it will be rebuilt. The goal of this blog is to bring the market, the rescue plans, the politics and the pontification home to you

The number of US homes being repossessed hit an all-time high last month

Banks took control of 92,432 properties in April, a 45% rise from a year earlier, said RealtyTrac.

BBC 13 maj 2010

This year the housing market /in the US/ showed signs of life.

But with foreclosures and unemployment climbing, prices have further to fall.

CNN Money 8/12 2009

According to RealtyTrac, nearly 2 million housing units in the U.S. are in foreclosure or bank-owned, and millions more are likely to join them.

As of March, banks had an inventory of about 1.1 million foreclosed homes, up 20% from a year earlier

Another 4.8 million mortgage holders were at least 60 days behind on their payments …

Based on the rate at which banks have been selling those foreclosed homes over the past few months, all that inventory, real and shadow, would take 103 months to unload.

TIm Iacono/WSJ nice chart 26/4 2010

Mortgage loans: Record number are late

Efforts to combat foreclosure plague are falling short as the total number of delinquent mortgage loans hits 9.64%.

Les Christie, CNNMoney November 19, 2009

In the third quarter, 9.64% of all mortgage loans were delinquent.

That represents 4.5 million borrowers and is an increase from 9.24% in the prior three months.

Full text

"Strategic defaults" now account for nearly one in three foreclosures

The numbers of repossessed properties, also called real-estate owned or REOs, have been boosted by a spike in the number of homeowners voluntarily giving up their homes because their the value has dropped so precipitously.

CNN 13 maj 2010

More evidence has arisen that the "strategic default" consumer spending thesis is correct

- and that the economic recovery on the whole is based on a rotten sham.

In this sleazy imitation of a free market economy, liars, cheats and deadbeats are the ones getting rewarded.

Marcet Oracle, Apr 20, 2010 By: Justice_Litle

All this time, I thought working hard for my money and staying debt free was wise. I thought sticking with one credit card - paying down the balance every month, no exceptions - was prudent. I thought driving a five-year-old car - fully paid off, nothing flashy - was a sensible thing to do.

Two weeks ago your humble editor asked, "Did the Housing Bust Fuel the Consumer Spending Binge?" In that piece, it was explained step by step how the phenomenon of "strategic defaults," i.e. homeowners walking away from their mortgages, may have fueled a surge in retail spending by way of freeing up cash.

"Did the Housing Bust Fuel the Consumer Spending Binge?"In keeping short-term rates near zero, the Federal Reserve has given the banks a license to print money.

Thanks to Ben Bernanke, banks can borrow as much as they want for practically nothing... plow that cash into longer-dated U.S. Treasuries... and make perpetually huge profits with little to no risk. It's like a permanent backdoor bailout subsidy.

Interest rate cuts work their way through to the real economy by a number of transmission channels.

Cui bono? The banks, of course. The bank-bailout channel will be the only monetary transmission mechanism to function like clockwork.

So do not be fooled by anybody who says that the central bank should cut interest rates for the benefit of innocent citizens

Wolfgang Munchau, FT January 20 2008

Can't pay or won't pay?

The write-downs, whether voluntary or court-ordered, could destroy the lenders’ capital.

Aggregate negative housing equity is thought to top $500 billion.

The Economist print Feb 19th 2009

Because US mortgages are “no-recourse” loans (lenders have no recourse to the house’s owner beyond the value of the house),

individuals with negative equity have an incentive to default.

Martin Feldstein, FT May 7 2008

"The losses for the financial system from people walking away could be of the order of one trillion dollars when

the entire capital of the US banking system is only $1.3 trillion.

"You could have most of the US banking system wiped out, so this is a total disaster."

Roubini, BBC 29 July 2008

The Obama administration's foreclosure prevention program

CNNMoney.com)March 4, 2009

The multipronged fix calls for companies to help as many 4 million struggling borrowers by modifying loans so housing payments are no more than 31% of monthly gross income.

Separately, homeowners who haven't missed a payment can refinance into lower-cost loans even if they have little or no equity.

This is expected to help up to 5 million homeowners.

The plan, released in broad-brush terms two weeks ago, has three components.

The first two parts involve an expansion of the role of Fannie and Freddie – providing them with additional access to funds and pursuing a $200bn refinancing plan for borrowers with mortgages that exceed the value of their homes.

The third component provides for $75bn of subsidies for modifications to home loans owned by banks and investors. This will provide mortgage servicers with incentive payments to modify loans and borrowers with inducements to stay up to date on their payments.

Hope for Homeowners gives the FHA the authority to back 300 billion dollars worth of restructured loans,

if, among other things, the lenders voluntarily agree to drop the value of the principal to 90 percent of the home's current value.

Diana Olick, CNBC October 15 2008

Senate Banking Committee Approves Housing Bill

Washington Post 20/5 2008

The proposal marks Washington's most ambitious response to the nation's housing crisis, which has so far thrown more than 1.5 million homeowners into foreclosure. With foreclosures rising, home prices have fallen by more than 10 percent, leaving many borrowers both unable to make their mortgage payments and unable sell or refinance because they owe the banks more than their homes are worth.

To qualify for an FHA-backed loan in either proposed program, lenders would have to be willing to write a new, 30-year fixed rate loan for borrowers for an amount no greater than 90% of the appraised value of the home. The other 10% would be equity for the borrower.

CNN 20/5 2008

The US federal government has tried to stabilise residential real estate, but nationwide prices have dropped by 13 per cent in the past 12 months.

Analysts have forecast that by June 30, 10.6m families will have either no equity in their homes or a negative equity.

Wilbur Ross, FT May 20 2008

The writer has created the US’s second largest servicer of subprime mortgages by acquiring American Home Mortgage and Option One

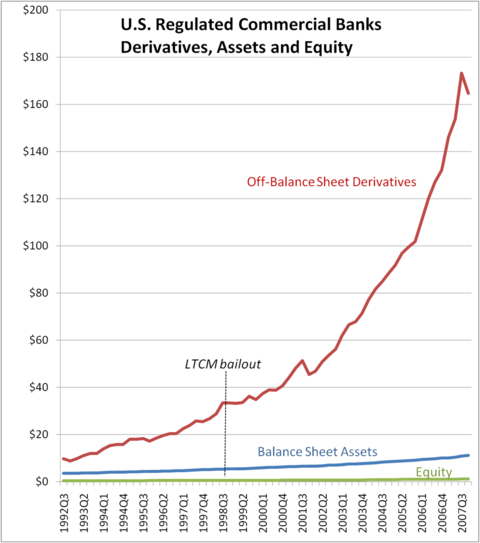

Back in April 1999, didn't the Chairman of the Federal Reserve, the Chairman of the SEC, The Secretary of the Treasury and the Chairperson of the CFTC jointly prepare a 140 page report on the Lessons of LTCM in which they stated that:

The principal policy issue arising out of the events...is how to constrain excessive leverage...

Mark Wenzel, April 13, 2008

"The principal policy issue arising out of the events...is how to constrain excessive leverage. By increasing the chance that problems at one financial institution could be transmitted to other institutions, excessive leverage can increase the likelihood of a general breakdown in the functioning of financial markets. This issue is not limited to hedge funds; other financial institutions are often larger and more highly leveraged than most hedge funds...The LTCM episode well illustrates the need for all participants in our financial system, not only hedge funds, to face constraints in the amount of leverage they can assume."

G7 försäkrade att deras centralbanker ska fortsätta att samordna åtgärder för att lindra kreditkrisen.

Penningpolitiken måste vara den första försvarslinjen, enligt IMF.

Samtidigt har IMF-chefen Dominique Strauss-Kahn efterlyst en plan för samordnade finanspolitiska stimulanser världen över.

Sådana megakeynesianska övningar bör man vara försiktig med.

DN-ledare 14/4 2008

För dem som har haft en övertro på marknadens självreglerande krafter

är förstås den internationella kreditkrisen en allvarlig missräkning.

Signerat, Ragnar Roos DNs ledarsida, 30/3 2008

What Exactly Is The G7 plan?

Mish, April 12, 2008

BusinessWeek is reporting Powers back plan to halt financial crux:

Finance officials from the world's top economic powers endorsed a plan Friday aimed at preventing another financial crisis like the credit and mortgage debacles that erupted in the United States and quickly sent tremors around the globe.

"Rapid implementation" of the plan "will not only enhance the resilience of the global financial system for the longer term but should help to support confidence and improve the functioning of the markets," the G7 officials said in a joint statement.

My /Mish's/ Comment: This sounds brilliant but exactly what is the plan?

President George W Bush has outlined plans to freeze rates on sub-prime mortgages

for five years to help people hit by the US housing market crisis.

Mr Bush said his plans did not signal a "bail-out" for mortgage lenders, property speculators or those "who made reckless decisions to buy a home they knew they couldn't afford".

BBC 6/12 2007

He isn’t conspicuously incompetent; and he isn’t trying to mislead us into war,

justify torture or protect corrupt contractors.

Paul Krugman, NYT, December 10, 2007

US Treasury Secretary Hank Paulson can be forgiven for pushing through a rescue plan last week that amounts to a flagrant abuse of contract law and capitalist principles.

Would free marketeers rather see the whole edifice of capitalism burned to the ground to make their point?

Ambrose Evans-Pritchard, Daily Telegraph, 10/12/2007

What we are witnessing is essentially the breakdown of our modern day banking system, a complex of levered lending so hard to understand

that Fed Chairman Ben Bernanke required a face-to-face refresher course from hedge fund managers in mid-August.

Bill Gross, December 2007

The trouble with the Paulson plan

In short, he said, it is a “market-based approach”.

Give the man some credit for using that term without laughing

Clive Crook, FT December 9 2007

Is there a housing-finance market on the planet that is more pervasively manipulated and distorted by government than that of the US – even before this latest intervention?

Start with virtually unlimited tax relief on mortgage debt.

Throw in the two giant “providers of liquidity”, Fannie Mae and Freddie Mac,

The tax deduction alone is nearly $80bn a year.

It is a little late for a market-based approach.

It would be surprising if dissenting investors did not challenge these modifications in court.

Normally it falls to conservatives to cry “moral hazard” when policies such as this, expressly designed to reward imprudent behaviour, are announced. This time, the indispensable Barney Frank, the Democratic chairman of the House financial services committee, is leading the chorus.

From now on, every mortgage foreclosure will be seen as proof of the policy’s failure – and partly the administration’s fault.

The US government’s attempt to stem the growing housing crisis involves arbitrary judgments, rewards for reckless behaviour and variations of contracts.

But it is justified by the extreme circumstances.

FT Editorial, December 7 2007

There are concerns that investor lawsuits protesting at breach of contract could derail the plan.

Sanctity of contract is indeed an important principle. But ....

There is moral hazard in rewarding foolish borrowing and it is exacerbated by a design flaw in the plan.

But authorities around the world have already found that this crisis demands extreme measures.

The promise and pitfalls of the Treasury's plan

for mortgage-loan modifications

The Economist print edition,Dec 6th 2007

Mr Paulson's attitude to the subprime mess has, to put it charitably, evolved over the past few months.

Half a year ago, he was firmly hands-off. The market should be left well alone, to shake out weak subprime borrowers and imprudent lenders.

The Treasury has now embarked on a third approach. Worried that the avalanche of resetting subprime mortgages (some 2m in the next 18 months) would bring a surge of foreclosures and further weaken house prices, Mr Paulson has prodded lenders and mortgage servicers to come up with “an aggressive, systematic approach” to get “able” borrowers into modified loans.

One reason to step in is that the Treasury solves a co-ordination problem. All lenders would be better off if a downward price spiral from unnecessary foreclosures could be prevented. Individually, however, each mortgage servicer might prefer foreclosing now, rather than waiting and possibly seeing the value of his asset fall. A second argument is that government involvement offers mortgage servicers some legal protection against investor lawsuits by, in effect, creating an industry standard for loan modification.

But set against those gains are some risks.

One is that the plan simply prolongs the subprime mess.

A second worry is that the plan is a form (albeit a gentle one) of government meddling in private contracts, one that could have far-reaching consequences for investors' willingness to hold future subprime debt. America's debt markets will be permanently damaged if investors fear that government will simply change the rules to suit the times.

"I think the plan is good in theory," said Mark Zandi, chief economist for Moody's Economy.com,

"but, in practice, it's going to come up short. There are too many impediments to its widespread adoption by investors and servicers."

"S&P Says Mortgage Freeze Plan May Cause Downgrades"

Note how, nevertheless, S&P bends over backwards to look supportive....

nakedcapitalism 7/12 2007

S&P, the largest ratings company, said bondholders may benefit from mortgage modifications if they result in fewer foreclosures....

Mortgage Meltdown 2007

CNN Portal

The current economic crisis, with its roots in the sub-prime mortgage and real estate markets is just the latest example of an old classic, the speculative market bubble.

These two industries, sub prime lending and housing, rose together in recent years, with climbing real estate prices driving higher demand in sub-prime mortgage lending. This led to more creative loans, both in the sub-prime market and in a market that came to be referred to as exotic loan products, as skyrocketing housing prices pushed consumers into ever higher levels of borrowing, exceeding what they could possible get in the prime lending zone.

Sharon L. Secor, December 3, 2007