The key problem for the US currency is that investors do

not need to sell US assets for the dollar to fall. All that is necessary is

that they fail to buy. The bloated US current account deficit, running at about

4 per cent of gross domestic product, means that the US needs to attract a net

inflow of around Dollars 1.5bn (Pounds 1.04bn) every day in order to stop the

dollar falling. The latest figures from the US Treasury provide strong

indications that capital inflows are finally drying up. In January the net

inflow into US equities and fixed income was just Dollars 9.5bn. This is weak

even compared with the Dollars 17.8bn the US attracted in September.

There are two theories about Wall Street's role in the bubble years of

the new economy. Either investment analysts were swept up, like everybody else,

in the prospect of extraordinary gains in efficiency that the Internet would

bring, so justifying ever higher share prices.

Or Wall Street saw a golden chance to peddle dirt.

New York's attorney-general, Eliot Spitzer, is a promoter of the second

theory. On April 8th he delivered an affidavit to the state's supreme court

that paints Merrill Lynch's share-buying recommendations for Internet companies

during 2000 as little more than a pretext to stuff gullible buyers with the

shares of rotten businesses. (Big customers, meanwhile, were whispered the

truth.)

00 peak, one of the worst 10 declines the US market has experienced

since the first world war.

Augusti kommer före september

Rolf

Englund i mail 2001-09-20

Jeff Madrick: Will the Market Crash?

The New

York Review of Books, Cover Date: August 10, 2000

Different Times, but the 1990s Do Resemble the

1920s

By Robert J. Samuelson The Washington Post

International

Herald Tribune, Thursday, April 23, 1998

More articles

Två tredjedelar av hela

börsvärdet på

Stockholmsbörsen försvann på

två och ett halvt år

DI-ledare 30/12 2002

År 2002 uppenbarades att vi just har varit med om en

av historiens största finansbubblor. Och Sverige drabbades hårdast,

två tredjedelar av hela börsvärdet på

Stockholmsbörsen försvann på två och ett halvt år.

Det behövs en uppgång på 200 procent

för att komma tillbaka till nivån från mars 2000 något

som kan ta decennier. Att Frankfurt ligger nästan lika illa till är

en klen tröst.

Bara två av den moderna historiens finanskriser har

varit värre, New York 1929 och Tokyo 1989. I det första fallet tog

det 25 år för börsindex att komma tillbaka och i det andra

fallet pågår raset fortfarande efter 13 år. Tokyoindex ligger

i dag 73 procent under 1989. Börsbubblor är inget att ta lätt

på.

Fyra av det sena 1900-talets största hjältar i

svenskt näringsliv - Percy Barnevik, Lars Ramqvist, Jan Stenbeck och Jan

Carendi - har fått se sina livsverk radikalt omvärderade.

Wallenberg, den finansfamilj som dominerat scenen i Sverige

i 70 år, är nu på sin höjd den främsta bland

jämlikar. Betyget över Peter Wallenbergs insats får skrivas

ned.

Investors förlorade pengar överskuggas av de 100

miljarder kronor som statens AP-fonder lyckades bränna på kort tid

genom att kasta in den statliga sparreserven i pyspunkan.

Det sena 1990-talets it-entreprenörer liknar mest -

så här efteråt - bondfångare. En del var naiva och andra

smarta. Frågan är i vilken av kategorierna namn som Mandators Lars O

Petterson, Icon Medialabs Johan Staël von Holstein, Sprays Jonas Svensson,

Mirror Images Alexander Wik, Ledstiernans Jan Carlzon, Connectas Christer

Jacobsson, Framfabs Jonas Birgersson och Emerging Technologies Kjell

Spångberg ska sorteras. Det som förenar är att it-bubblan

löste deras försörjningsproblem.

Socialdemokratin, som tog över hegemonin i svensk

politik efter Kreugerkraschen, har nu hjälpt till att blåsa upp

två nya bubblor,

först en i fastigheter och finans år 1989 och därefter den

senaste i it och telekom år 2000.

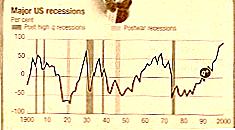

The boom that did not bust

By

John Plender

Published: February 6 2003 21:02

In the developed world it appears that financial crises no longer derail

economies. Even in Japan, which has experienced four years of price deflation

and where the banking system has been in crisis for over a decade, the output

loss has been minor. And now the collapse of a phenomenal stock market bubble

in the US has defied historical precedent by spawning only a modest recession

and no banking crisis at all.

There are many possible explanations for the failure of this financial

dog to bark. Much more of the risk-taking was happening outside the banking

system than in the 1980s. Banks appear better capitalised as a result of the

Basle capital regime. Most important, policymakers in the US have been acutely

aware of the risks of deflation and swift in their monetary and fiscal response

to the bursting of the bubble. Thursday's cut in UK interest rates likewise

suggests that the risks in UK policy are not being taken on the side of

deflation.

So now the politicians and central bankers are intensively managing the

business cycle, can we stop worrying about the impact of financial instability

on economic growth? Not in the emerging markets, where financial crises in

Asia, Latin America and Russia have inflicted devastating losses of output and

employment. And there is one important snag in the developed world, especially

in the English-speaking economies.

The existence of a monetary and fiscal safety net creates moral

hazard. That is, companies, financial institutions and private individuals

engage in balance sheet adventuring - an evocative phrase used by the economist

Hyman Minsky, whose thinking on financial instability and the business cycle is

particularly relevant in the post-bubble world.

Financial crises serve a purpose. In cycles that have been characterised

by debt-financed and unremunerative over-investment, the discipline of

bankruptcy ensures that debt is written down to realistic values and capacity

is brought into line with demand to pave the way for an upturn. But the

adjustment is painful.

If financial crises are eliminated, the business cycle is extended.

Asset prices continue to rise, generating wealth effects that encourage people

to run down savings and borrow on the strength of the rising value of their

collateral. As the Montreal-based Bank Credit Analyst points out, the failure

to correct balance sheet excesses in the downturn means that each new US

expansion begins from progressively lower levels of liquidity.

US household debt has gone from less than 40 per cent of gross domestic

product in 1960 to close to 80 per cent in 2002. The comparable rise for the

non-financial corporate sector has been from 26 per cent to 46 per cent. The

greater the balance sheet excesses, the more painful the corrective process

will ultimately be. So with each new cycle, say the BCA editors, the stakes

become higher, pushing the economy closer to a deflationary end-point. An end

is inescapable since debt cannot rise faster than incomes for ever.

The denouement of the debt drama is sparked by deteriorating credit

quality, which exposes the vulnerability of a banking system that hitherto

appeared well capitalised. The risk is of a 1930s-style deflation and liquidity

trap, as banks stop lending and the private sector tries to restore its balance

sheet. It was on such grounds that Peter Warburton, the British

economist, warned in a recent book - Debt and Delusion, Penguin Books -

of an explosion thatould shock the western financial system rigid.

Yet there is a problem with timing. Governments have become used to

managing the cycle and deferring the debt problem. For their part, private

individuals in the US and UK continue to be happy to borrow for home ownership

without fully grasping the extent of the repayment burden in a low inflation

era.

Many feel a high level of debt is affordable on the basis of a

one-off fall in interest rates to very low levels. Yet there is no such thing

as a one-off fall in interest rates. Throughout history interest rates have

gone up as well as down. And the debt will not go away.

So while Mr Warburton, like Noah, builds his ark, a question remains.

If debt continues to accumulate over the next economic cycle, will central

bankers and governments be able to confront an apocalyptic financial crisis by

simply muddling through?

Full

text

Greenspan's fight

Low interest

rates is not enough

By Martin Wolf

Financial Times, November 12 2002

Last week, the Federal Reserve decided to blow, once again,

into the flapping sails of the US economy. The puncturing of the bubble economy

continues to create fierce headwinds. Further interest rate cuts - perhaps more

unorthodox measures - remain likely.

The last time the Fed Funds rate was as low as this was

July 1961. The decisions to cut the rate from 6.5 per cent in late 2000 to the

lowest rate for more than 40 years underlines the devastating impact of asset

price bubbles on economic stability.

The aggressive easing of monetary policy is not the only

stimulant on offer to the economy. The rate of just over 4 per cent on 10-year

Treasuries is the lowest since 1963. Moreover, according to the Congressional

Budget Office, the fiscal stimulus this year is worth 2.4 per cent of gross

domestic product, the biggest since records began in the early 1960s.

If not for these huge fiscal and monetary boosts, a deep

recession would surely have occurred. They have also returned the economy to

reasonable growth this year, at 3 per cent over the 12 months to the third

quarter. This is much stronger growth than in other leading industrial

countries, except Canada.

The remarkable productivity record of the US economy is now

a two-edged sword. Over the year to the third quarter, output per hour in the

non-farm business sector grew 5.4 per cent. As Alan Greenspan, chairman of the

Fed, has noted: "Over the past seven years, output per hour has been growing at

at an annual rate of more than 2? per cent, on average, compared with a rate of

roughly 1? per cent during the preceding two decades."* This suggests trend

growth in the economy is in the neighbourhood of 3? per cent.

If this productivity performance is sustained, economic

growth of less than 3? per cent means rising excess capacity and downward

pressure on profitability, wages and prices. Worse, given that there is

substantial excess capacity today, still faster growth is needed first, to

bring the economy back to more normal levels.

The current account deficit has reached 5 per cent of GDP.

Absent a miraculous turnaround in demand in the big economies outside the US,

the only way this could shrink, in the short run, would be via a huge US

recession. Far more likely is a continuing rise in the deficit, with 7 or 8 per

cent of GDP readily imaginable in the not too distant future. This is how the

US is stimulating demand in parasitic economies elsewhere.

For a long time, consumer spending grew faster than

disposable income, as the household saving rate fell and borrowing increased.

In the second quarter of 1992, the household saving rate was 8.9 per cent of

disposable income. It had fallen to 0.8 per cent by the end of last year. It is

on its way back up this year, as stock market wealth has fallen, unemployment

risen and uncertainties increased. The financial balance of the household

sector went from close to plus 5 per cent of GDP in 1992 to minus 2 per cent in

the last quarter of 1999. It has still to recover.

US

Trade Deficit

Greenspan and the

Asset Price Bubble

Full

text

Top of page

Bubble, bubble default trouble

By John Plender

Financial Times, October 3 2002 20:15

The most damaging bubbles are those in which stock market exuberance is

accompanied by lending euphoria. This was true of the 1920s and of the 1980s

Japanese bubble.

What makes the combination so destructive is the pro-cyclical nature of

credit expansion, which causes asset prices, incomes and profits to rise in a

boom that feeds on itself. It then becomes viciously self-feeding in the

downturn, courtesy of the regulators, since banks' capital adequacy

requirements go up instead of down when credit quality deteriorates.

Full

text

John Plender Financial Times; Jul 15, 2002

So you think this bear market is

rough?

It is positively limp-wristed when compared with the depths of

the mid-1970s.

Top of page

The surprising fact is not that /US stock/

markets have fallen, but that they remain so overvalued.

Martin Wolf: The

bubble will keep deflating

Financial Times 2002-06-19

The story is told in my chart.

This shows the Standard & Poor's composite index (deflated by

consumer prices) since the 1880s. On this logarithmic scale, the steeper the

slope the faster the rate of growth. There have been several bull markets: the

fastest rise was in the 1920s, but the longest and cumF" VALIGN="TOP">

real interest rates, which are

relevant, with changes in inflation, which may not be.

Nobody is behaving as if the expected real return on - and cost of -

capital is far lower than ever before. If this were true, surveys would suggest

lower expected returns from markets than before: the opposite is the case. In

addition, companies would sustain investment as returns fell: the recent

investment "bust" suggests just the opposite.

Either this has been a bubble the scale of which is making deflation

slow and painful, or the long-run real return on - and cost of - capital in the

US is lower than before. If it is the former, markets remain very expensive. If

it is the latter, everyone expects historically low returns.

I, for one, think the market is simply expensive.

Full

text

Top of page

Terrible twins?

Economic parallels

between America and Japan

America's economy looks awfully like Japan's

after its bubble burst

Jun 13th 2002 From The Economist print

edition

The similarities between America's financial bubble in the 1990s and

Japan's in the 1980s have been well rehearsed. In both cases, share prices and

capital spending soared; households and companies went on a borrowing binge.

Japan, like America a decade later, enjoyed a spurt in productivity growth,

suggesting to some that it had a superior economic model.

Yet the conventional wisdom now is that the economies have taken

divergent paths since their bubbles burst. Thanks to resilient consumer

spending, America is widely tipped to enjoy robust growth this year and next.

Meanwhile, Japan is expected to languish in perpetual recession.

Full

text

Top of page

The recovery myths

The world economy is

coping with the aftermath of two huge asset-price bubbles: the Japanese of the

1980s; and the US-led worldwide bubble of the second half of the 1990s.

Adjustment to the end of the first is not yet over. Adjustment to the end

of the second has, contrary to conventional wisdom, hardly begun.

By

Martin Wolf, Financial Times June 11 2002

According to that wisdom, the world's largest economy is leading the

rest of the world into a durable, if restrained, recovery after a surprisingly

brief and shallow recession. Yet this may turn out to be no more than a fairy

story for frightened children. Recent falls in the stock market and the US

dollar suggest the children are unconvinced. At its closing price of 1,031 on

Monday, the Standard & Poor's 500 was only 7 per cent above its

post-September 11 low and 33 per cent below the peak reached in March 2000.

Similarly, on a trade-weighted effective basis, the dollar had lost 6 per cent

of its value since its peak on January 25 2002.

To understand the risks ahead, it is necessary to analyse where the

world economy now is in its post-bubble adjustment. Between 1996 and 2000, the

US economy generated 40 per cent of global incremental real demand (at market

exchange rates). While US real domestic demand rose 26 per cent over those

years (a compound rate of 4.7 per cent a year), output grew by 22 per cent (a

compound rate of 4.1 per cent). The difference was the rise in the US current

account deficit, to 4.5 per cent of gross domestic product in 2000.

This expansion was unsustainable and, last year, came to an end.

Symptoms of excess were, as Brian Reading of London-based Lombard Street

Research argues (Monthly International Review 115, April 2002), too much

investment, too little saving and too big a current account deficit. Behind

these three phenomena was belief in the miracle of the "new economy", as

demonstrated by asoaring stock market, huge capital inflows and a surging

dollar.

Over the past year and a half, the US economy and, given the global role

of the US, the world economy, has begun its post- bubble adjustment. Yet what

is remarkable about this period is how modest that adjustment has been.

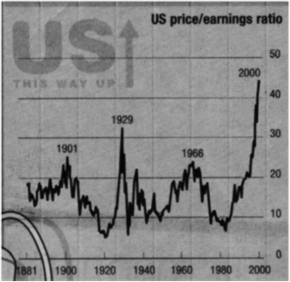

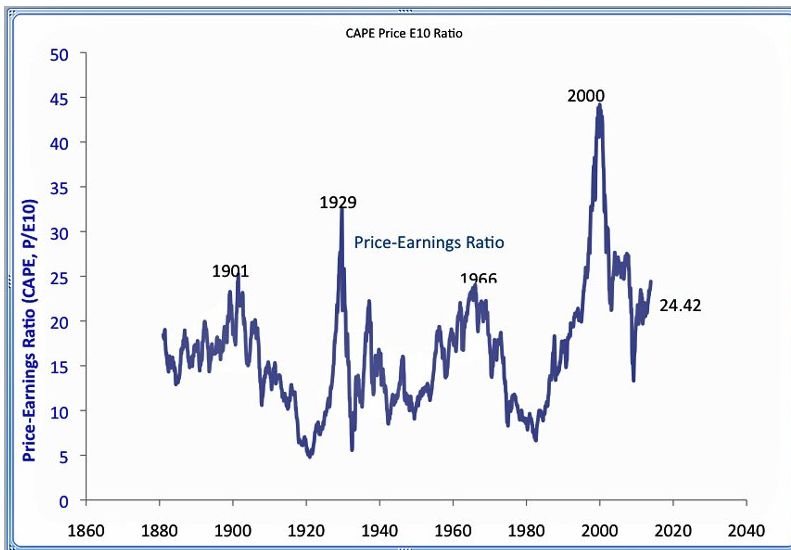

On June 7, the price/earnings ratio for the overall stock market was

still close to double its long-run average. Measures of underlying value

suggest that the market is still more generously valued than at any period in

the past hundred years, apart from the peak of the recent bubble and in 1929.

On a trade-weighted basis, the US dollar is 35 per cent higher than in May

1995. Estimates of the real exchange rate suggest the dollar remains almost as

high as in 1985.

Last year, business fixed investment in the US was only 3.2 per cent

below its level in 2000. This year, it is forecast by Goldman Sachs to be down

only another 7 per cent. The resilience of consumption has been astounding.

Supported by rising house prices and low interest rates, 00">1925

1929

Alan Greenspan's Federal Reserve has, in effect, restricted the

post-bubble adjustment almost entirely to the corporate sector. It has propped

up asset prices and supported household borrowing and spending. The big

question today is whether it has durably averted or temporarily postponed that

adjustment.

The answer is that, however unpredictable its timing and speed, it is

highly implausible that adjustment can be averted for ever. That would imply a

continuation of extraordinarily low household saving. It would also mean an

explosive rise in the current account deficit. If the US were to continue to

grow faster than most of the rest of the world, the deficit could reach 5 per

cent of GDP next year. Under plausible assumptions, net claims by foreigners on

the US would also rise from 20 per cent of GDP to 50 per cent of GDP, or more,

five years from now.

This looks inconceivable. A more natural outcome would be a weakening

dollar, weak domestic demand and an improving external balance. That change

could, in turn, be triggered by a diminished willingness of foreigners to

purchase US assets. The vulnerability is evident. As a gigantic net borrower

from the rest of the world, the US depends on foreigners to sustain the value

of its corporate assets and its currency. As London-based Smithers & Co

says, domestic corporate cash flow is now weak and US households have been

persistent net sellers of the stock market. This is, in part, to finance the

purchase of other assets, especially houses. If foreigners fail to fill the

gap, stock prices, as well as the dollar, must fall.

Further asset price adjustment is thus likely. If it coincided with

weakening household demand and if the adjustments, particularly in the dollar,

were slow and limited, it would also be helpful for the US. If, for example,

the trend rate of economic growth were to be 3? per cent a year and domestic

demand were to grow at, say, 2? per cent, there could be a steady contraction

in the current account deficit at half a percentage point of GDP a year.

Instead of adding demand to the rest of the world, the US would then be

subtracting from it. The question is where this would be offset. The eurozone

has, alas, generated growth in domestic demand of more than three per cent in

only two years - 1997 and 1998 - since 1993. Growth in demand averaged only a

little over 2 per cent between 1993 and 2001. Over these years, Japanese growth

in demand averaged 1.2 per cent.

With Japan's room for manoeuvre limited, much would depend on the

ability of the eurozone to generate faster growth in demand. Without aggressive

action by the European Central Bank, that seems depressingly unlikely. It is at

least as plausible that weaker export growth and a strengthening currency would

undermine investment and consumption in the eurozone.

One can therefore envisage three alternative scenarios for the medium

term.

First, there may be no significant further adjustment in the behaviour

of the US consumer or in US asset prices. In that case, the US would generate

strong additional demand for the rest of the world and even more un- balanced

household and national balance sheets. This would be a Gadarene rush for the

cliff. But that cliff may only be reached years from now.

Second, there may be smooth adjustment in US household behaviour and the

dollar. The latter would help offset weak demand at home by forcing adjustment

on the rest of the world. This scenario would be most beneficial for the US but

decidedly problematic for the rest of the world.

Third, there may be brutal adjustment in the near future, with a vicious

downward spiral in US and world equity prices, higher long-term interest rates,

an exodus of capital and dollar weakness. This would force a strong reduction

in investment and consumption in the US and an unpleasant adjustment on the

rest of the world. This would be the world of the double dip.

None of these alternatives can be ruled out. But the second is

preferable, for both the US and the world. If the dollar were now set on a

gradual decline, that would be altogether helpful. Unfortunately, this scenario

is too rosy to be plausible. The true choice may be between going over a high

cliff some years from now or going over a rather lower cliff quite soon.

The consensus view is not necessarily wrong. There may be a US-led

recovery in the next year or two. But it is too short-sighted. The post-bubble

adjustment can only have been postponed. It would be better if adjustment

continued at a moderate pace right now.

See also Dollar and

US Trade Deficit

Klas Eklund: USA har

världens starkaste ekonomi

Top of page

"Hög produktivitet

rättfärdigar inte p/e-tal"

DI 2002-03-11

Även om den amerikanska ekonomin permanent skulle bibehålla

den starka produktivitetstillväxten från slutet av 1990- talet

så skulle inte det rättfärdiga de "urvuxna" p/e-talen för

amerikanska aktier. Det sa chefen för Federal Reserve i St Louis, William

Poole.

Under det sena 1990-talet upplevde den amerikanska ekonomin en kraftig

produktivitetstillväxt, enligt flertalet ekonomer drivet av

införandet av ny digital teknik och av ett fördjupande av den

generella kapitalbasen i ekonomin. William Poole varnade dock för att

historien visar att tekniska innovationer "inte har bestående effekt

på företagens intjäningsförmåga, som slutligen

ofrånkomligt måste konvergera med den generella tillväxttakten

i ekonomin."

Det genomsnittliga p/e-talet i S&P-500-indexet är 26,0 baserat

på prognoserna på resultaten 2002, enligt Standard & Poor's.

Enligt William Poole skulle även ett genomsnittligt p/e-tal på 20

"vara en generös nivå givet att det historiskt genomsnittliga

p/e-tal har legat på 15."

Beträffande Nasdaq-100 indexet sade William Poole att p/e-tal

på 1FONT>

Top of page

The houses that saved the world

Mar 28th

2002 From The Economist

IT IS somewhere to live; but a home is also, for many folk, a valuable

asset. No wonder people love talking about house prices over the dinner table.

In this economic recovery, however, homes have done much more than shelter

people from wind and rain. They have helped to shelter the whole world economy

from deep recession.

Many economists were worried last year that the wealth loss from falling

share prices would force consumers to cut their spending. Even after the recent

recovery, American stocks are still worth 25% less than two years ago. Yet, as

falling share prices made some households feel poorer, rising house prices have

made many more feel richer. Over the past year average house prices in America

have risen by 9%, their fastest-ever in real terms.

Although American households as a whole have more of their wealth in

equities than in housing, a relatively few rich people hold the bulk of the

shares. For most people, housing is by far their largest form of wealth.

Two-thirds of Americans own their homes, and gains in the value of those assets

have encouraged them to keep spending.

Full

text

Top of page

John H. Makin, American Enterprise Institute

By

the end of 2001, American debt service burdens relative to disposable income

were at forty-year highs

Between September and December of last year, real consumer spending rose

at an 8.1 percent annual rate, above the smoothed quarter-over-quarter rate of

5.3 percent reported in the GDP statistics, while real disposable income fell

at a 7.2 percent annual rate. The rush to buy homes and automobiles on

favorable terms was financed largely on credit rather than through a surge in

incomes.

Indeed, by the end of 2001, American debt service burdens relative to

disposable income were at forty-year highs, though still sustainable provided

that the economy bounces back.

At the end of last year, American households and investors believed in a

quick recovery of the U.S. economy and increased spending at a rate that will

be sustainable only if that recovery fully comes to pass.

Full

text

Top of page

There is still worth in value

Philip

Coggan

Financial Times, January 26 2002

It may be time to dust off that list of high-yielding stocks

Sophisticated investors sneer at the division of their profession into

"value" and "growth" schools, seeing it as the kind of simplistic

generalisation beloved of lazy journalists.

But last year, one of the simplest valuation measures available -

dividend yield - was the key to successful UK investment performance. Value

stocks, as represented by the highest yielders in the FTSE 350, outperformed

the low-yielding growth stocks by 23 percentage points. According to the

statisticians at CAPS, that followed a 30-point outperformance by value in

2000.

After all the fuss about "sophisticated" market measures such as

EV/Ebitda (enterprise value/earnings before interest, tax, depreciation and

amortisation), it may seem odd that something as rough and ready as the

dividend yield could have been so useful.

But that may simply reflect the extremes to which the market's obsession

with growth had driven valuations in the late 1990s. At the peak, according to

Credit Suisse First Boston, the price-earnings ratios of the most highly rated

stocks were 6.5 times those of the lowest-rated. That compares with a ratio of

less than 3 for much of the 1990s.

All that we have seen, therefore, is a correction of the insane

valuations witnessed during the technology bubble.

But the odd thing is that growth investors do not seem in the least bit

abashed by their battering over the past two years. As soon as the market began

to bounce in late September, they piled into the TMT (technology, media and

telecommunications) stocks all over again. Because earnings have fallen as fast

as share prices over the past two years, valuations in the technology sector

are still up in the stratosphere. According to Thomson Financial, the historic

price-earnings ratio on the sector is about 100.

So why are investors, having been once bitten by the technology bug, not

twice shy? One answer, according to Bart Dowling, director of global asset

allocation at Merrill Lynch, is that investors are not entirely rational.

His statistical analysis shows that investors are much more influenced

by recent returns than they are by long-run performance. In the late 1990s, the

returns from owning technology stocks were phenomenal. Any fund manager who was

underweight in the sector underperformed the indices and was in danger of

losing clients.

The passion for growth stocks may be reinforced by the feeling that

overall returns from equities are likely to be low in future years. An annual

return of 7 per cent or so simply looks unappetising to most investors. Growth

stocks offer stronger meat.

Value stocks, in contrast, are seen as working just once in the cycle

(as an economy emerges from recession) but are not serious long-term

investments.

Academic evidence, however, suggests that, over the long term, value

strategies such as buying companies with low price-to-book ratios tend to

outperform the market. Remarkably few fund managers have attempted to exploit

such apparent anomalies.

This may simply be a function of the lack of respect with which the fund

management community holds academics. They did not believe the academics when

they said the markets were efficient and that most active fund management is a

waste of time; they do not believe them now when they are told to concentrate

on value stocks.

Where are we now in the cycle? It is tempting to think, after two

fantastic years for value, that it is time to switch back into growth. But

bubble valuations have not entirely disappeared, even if one dismisses the

price/earnings ratio of the technology sector as a statistical fluw.prudentbear.com/bc_library_book_store4.html">Books

ke (on the

grounds that the sector has virtually no earnings). Other measures such as

price-to-sales still leave the market looking more expensive than it was in the

early 1990s.

Full text

Top of page

The doom-mongers

The Economist 2002-01-24

The doom-mongers (including The Economist) who predicted a deeper

downturn have, many argue, been proved wrong. Perhaps. But what the optimists

have lost sight of is that America's recession was caused neither by the events

of September 11th nor, like every previous post-war recession, by tightening by

the Federal Reserve in response to rising inflation.

The root cause of this recession was the bursting of one of the biggest

financial bubbles in history. It is wishful thinking to believe that such a

binge can be followed by one of the mildest recessions in history—and a

resumption of rapid growth.

Full

text

Remember fiscal policy?

How to

use fiscal policy in a recession

The Economist Jan 17th 2002

When it works, monetary policy is fine. But sometimes it does not work.

Problems arise, especially, under the circumstances that most interested

Keynes when he first developed his thinking on

deficit spending as a cure for recession—that is, at times of low, or even

negative, inflation.

Full

text

Top of page

America sails serenely through a perfect storm

Gerard Baker, Financial Times, Jan 24 2002

The US has gone through its own elemental sequence of shocks in the past

three years that ought to have left it in a slump at least as bad as anything

it has experienced in the postwar period.

Beginning at the end of 1998, it was hit with the financial damage from

the Asian and Russian financial crises, followed by rising interest rates, a

steep increase in energy prices, the bursting of the dotcom bubble, the sharp

fall in the equity market, the steepest drop in capital spending in decades,

the most destructive terrorist attack in history and a hot war all over the

world which, for the first time in more than a century, poses a clear risk to

US security at home.

For good measure, on the political front, it had the impeachment of a

president and an election that failed to produce a winner until the courts

ruled five weeks after polling day.

It has been, to use the current cliche, the perfect storm of economic

and political shocks. And yet, here we are, almost before we have come to grips

with recession, staring at the growing probability that a recovery is under

way.

Output began falling last March. If it stops falling in the current

quarter - and then climbs again - the entire decline in GDP will be less than 1

per cent. In other words, if the current trends take hold, it is possible that,

having enjoyed the longest expansion in its history, the US is now climbing out

of the shortest and shallowest recession on record.

Let me enter some caveats. Recovery is by no means assured, of course.

The US has not eliminated imbalances that built up in the late 1990s.

Levels of corporate and personal sector debt remain high and could act as a

drag on growth. The extent to which the capital-spending binge of the latter

stages of the expansion created an investment overhang is still unclear, with

capacity utilisation rates remaining low. Corporate profits are weak and could

act as a further constraint on an investment recovery. Stock market valuations

still look presumptuous and vertiginous. Above all, perhaps, the durability of

the productivity miracle that seemed to be behind the rapid growth of the late

1990s is uncertain, although output per hour has held up remarkably well during

the downturn so far.

But consumption has remained robust in the past year and consumers'

balance sheets have been improved by falling interest rates, rising house

prices and last year's tax rebate.

If recovery does take hold, there will be plenty of candidates for the

credit: the Federal Reserve, certainly, for cutting interest rates more

aggressively than at any time in living memory; Congress, probably, for

shrewdly ignoring the initial request of the Bush administration not to pass an

immediate fiscal stimulus and for providing tax rebates at just the point when

they were most needed. The Bush administration's original tax cut proposals -

until last April - were all long-term and it opposed the idea of rebates last

summer.

Luck has played a part too, of course. Falling oil prices have raised

consumers' spending power. Inflation has all but disappeared. There have been

no more terrorist attacks so far.

If we see a recovery as 2002 unfolds, it is possible it will not be a

particularly robust one. Unemployment may still rise, especially if the

productivity gains are maintained. And in any case, since consumption did not

fall all that much last year, it may not stage its traditional rally into the

recovery. Corporate profits will probably stay weak, and an overvalued equity

market may still hover over the economy's prospects. But in the face of a

whirlwind of adversity over the past two years, it would be remarkable if there

is any recovery at all.

To listen to much of the commentary on the US at present, you would

think there was something rotten in the very foundations of America's economic

structure. The Enron collapse, and the evident greed, corruption and negligence

that went with it, certainly point up the need for reforms to the system of

checks and balances in American capitalism.

But in condemning and setting right the weaknesses, it would be wise,

too, to pause for a while, look at what has happened to the US economy in the

past few years, and, quietly, marvel.

Full

text

Top of page

The 1990s’ Boom Went Bust. What’s

Next?

Milton Friedman

Wall Street Journal 2002-01-22

To an economist, the 1990s bear an uncanny resemblance to two earlier

decades: the 1920s in the United States and the 1980s in Japan. In all three

decades, technological change produced extraordinary economic growth, leading

to talk of a “new era” and triggering a bull market in stocks that

terminated in a market collapse-widely regarded as the bursting of a

speculative bubble.

The 1920s were followed by the Great Depression in the U.S., the 1980s

by stagnation and recurrent recession in Japan.

What will the 1990s bring? And what role has monetary policy played in

these episodes?

Economic growth during the first 10 years of each episode was remarkably

similar. Real gross domestic product grew an average of 3.3% per year in the

U.S. from 1919 to 1929; 3.7% in Japan from 1980 to 1990; and 3.2% in the U.S.

from 1990 to 2000 -- clearly, remarkable similarity.

In the two earlier episodes, what followed was very different-a major

catastrophe in the U.S., stagnation in Japan.

From the peak in 1929 to the trough in 1933, U.S. GDP fell by more than

a third, and had not returned to the 1929 peak by the next cyclical peak in

1937. In Japan, GDP fell below the initial peak level by trivial amounts for a

few quarters, plateaued for about two years, and then resumed slow but highly

erratic growth.

In the U.S., unemployment reached 25% at the trough of the depression in

1933. During the rest of the decade, 1934 to 1939, unemployment averaged 18%.

In Japan, reported unemployment never exceeded single digits. This number

understates the severity of the situation, thanks both to different methods of

recording and different national cultures bearing on employment. Nonetheless,

it seems clear that an estimate comparable to U.S. figures would never have

reached anything like 25%.

The three bull markets in stocks likewise display remarkable similarity,

even extending to the early stages of the current decline. In the six years

prior to the stock market peak, the indexes rose 333% in the U.S. from 1923 to

1929, 387% in Japan from 1983 to 1989, and 320% in the U.S. from 1994 to 2000.

The subsequent decline was decidedly less in Japan in the 1990s than in

the U.S. in the 1930s -- 55% compared to 80% from the peak to the initial

trough. However, the Japanese index remained flat throughout the 1990s. and

more recently has fallen sharply again, while the U.S. index rose rapidly from

its 1933 trough.

The quantity of money rose fairly steadily in all three of the decades

preceding the stock market peak, but at a much higher rate in the Japanese

decade -- 9.1% per year from 1980 to 1990, compared with 3.9% per year from

1919 to 1929 and 4.1% per year from 1990 to 2000 in the U.S. The higher rate in

Japan may explain why the Japanese bubble was so much more sweeping than its

counterparts in the two U.S. episodes.

The behavior in the following years differed much more sharply. The U.S.

quantity of money fell by more than a third from the cyclical peak in 1929 to

the trough in 1933. The Japanese quantity of money fell by two-tenths of one

percent in the first year after the cyclical peak, and then rose by 2.5% per

year in the next two years. In the current episode, the quantity of money in

the U.S. has already risen by more than 11% during the first five quarters

after the cyclical peak.

These differences in monetary growth are a major reason why the

contraction in the United States from 1929 to 1933 was so much more more severe

than the flat economic growth or modest contraction in Japan. They also suggest

that the current reaction in the U.S. will be far less severe than in either of

the earlier episodes.

The evidence linking the behavior of the stock of money with the

behavior of the economy goes well beyond these three episodes. Every great

depression has been accompanied or preceded by a monetary collapse-banking

difficulties plus a decline in the quantity of money-just as every great

inflation has been accompanied or preceded by sharp increases in the quantity

of money.

Central bankers, like other students of money, have learned this lesson,

which is part of the reason that there has been no repeat of the Great

Depression in the post-World-War II period despite repeated scares. The Federal

Reserve under Alan Greenspan is currently applying that lesson, which is reason

to believe that the current recession will be mild and that expansion will soon

resume.

What the future brings will depend of course on how monetary policy

evolves. While the current rate of monetary growth of more than 10% is

sustainable and perhaps even desirable as a defense against economic

contraction and in reaction to the events of Sept. 11, continuation of anything

like that rate of monetary growth will ensure that inflation rears its ugly

head once again.

However, the Fed preempted on the downturn and I suspect it will again

preempt on the upturn, so as to avoid such an outcome.

Full text

Klas Eklund:

USA

har ryckt åt sig ett stort försprång och har världens

mest framgångsrika ekonomi

More about New Era

Top of page

USA i kraschläge

DI:s Cecilia Skingsley

2002-01-21

Hur stor är risken att USA glider in i samma långvariga

stagnation efter IT-kraschen 2000 som efter börskraschen 1929 eller hamnar

i samma decennielånga bekymmer som Japan efter deras krasch 1990?

Det finns alltför många otrevliga likheter mellan USAs

1920-tal, Japans 1980-tal och de senaste årens händelser.

Om historien håller på att upprepa sig måste man

skrota alla proffsprognoser om en konjunkturvändning i år,

likaså är finansmarknaderna på tok för optimistiska om

2002.

Amerikanskt 1920-tal, japanskt 1980-tal och amerikanskt 1990-tal

kännetecknades av extrema uppgångar i tillgångspriser. Danske

Bank har tittat närmare på perioderna och konstaterar att Dow Jones

steg med 135 procent från 1927 till kraschen i september 1929.

Tokyobörsen steg med dryga 140 procent 1986 till 1990. Den

uppgång 1990-taleONT COLOR="#000000">Dollar and

Trade Deficit

t bjöd på var ännu större: Standard

& Poor's 500 klev upp 230 procent från januari 1995 till mars 2000.

Värst var Nasdaqbörsen som steg med mer än 500 procent mellan

1995 och mars 2000.

Andra likheter mellan tidsperioderna är den kraftiga

tillväxten i investeringar och konsumtion. Optimismen om framtiden

flödade. På 1990-talet gav den långvariga

konjunkturuppgången upphov till begreppet "ny ekonomi".

IT och telekommunikation utmålades som nyckeln till framtiden. Det

glada 1920-talets version av IT- upphetsningen var bilen. Antalet bilar

mångdubblades mellan 1920 och 1929 och symboliserade framtidsanda och

dåtidens teknologiska under.

Japan slog på 1980-talet igenom som Det Ekonomiska Undret.

Japanska företag ansågs allmänt vara mer effektiva än sina

europeiska och amerikanska konkurrenter.

Produktivitetsutvecklingen var imponerande i båda USA och Japan

under uppgångsfaserna och de ackompanjerades av investeringsplaner som

bågnade av framtidstro.

Tillgångsprisernas påverkan på

konjunkturförloppet har kommit mer i fokus både i centralbankernas

beslutsfattande och den ekonomiska forskningen. Den grundläggande tanken

är att hushåll försöker sprida ut sin konsumtion ganska

jämnt över livet.

Den så kallade förmögenhetseffekten blir då

viktig. Om hushållen bedömer att deras egna tillgångar har

blivit varaktigt mer värdefulla (till exempel aktieportföljen eller

ett eget hus) spenderar de mer pengar.

Flera amerikanska studier visar att 1 dollar mer i

förmögenheten leder till en permanent uppgång i

hushållets konsumtion med mellan 3 och 5 cent.

På detta beteende kan man också lägga

hävstångseffekter som uppstår när optimistiska

hushåll (och företag) belånar sina värdestegrande

tillgångar och använder det till ökad konsumtion eller nya

investeringar. Sparandet faller och blir till och med negativt (i Japan

på 1980-talet och i USA under 1990- talet).

När spekulationsbubblan har blivit uppenbar och

tillgångspriserna börjar falla igen sker en rad anpassningar i

samhällsekonomin som försätter konjunkturutvecklingen i

nedförsbacke.

Investeringarna faller kraftigt och konsumtionen brukar samtidigt mattas

av när hushållen inser att de är för skuldsatta för

att fortsätta sin köpfest och i stället börjar betala av

på lånen.

Om spekulationsbubblan involverat stora krediter från

finanssektorn finns också risken för en bankkris. Den amerikanska

bankkrisen på 1930-talet och den japanska på 1990-talet

försämrade kreditförsörjningen till näringslivet

så mycket att den försatte USA i depression och har försatt

Japan i en långvarig lågkonjunktur.

I dagens ekonomiska bekymmer i USA saknas en bankkris vilket är en

välkommen indikation på att historien inte behöver upprepa sig.

En viktig skillnad mellan dagens situation och de tidigare historiska faserna

är att den ekonomisk-politiska reaktionen i USA har varit så mycket

snabbare.

Centralbanken Federal Reserves många räntesänkningar

under fjolåret underlättar lånesaneringen hos företag och

hushåll och det minskar mängden kreditförluster i

bankssystemet. Skulle förlusterna tillta i banksektorn kommer Federal

Reserve att reagera snabbt.

Vid de tidigare börskrascherna i Japan och USA var den politiska

reaktionen till en början felaktig och i bästa fall

otillräcklig. Den japanska centralbanken förde en stram

penningpolitik med hög styrränta under en stor del av 1990-talet.

Detta försvårade skuldanpassningen och kreditförlusterna

exploderade.

I USA efter börskraschen drog man visserligen ned

ränteläget, men eftersom inflationen föll dramatiskt ned till

negativa tal blev realränteläget ändå mycket högt.

Den misskötta bankkrisen som uppstod fick

kreditförsörjningen att haverera och det skulle dröja till 1933

innan politiken lades om.

Trots att USA nu befinner sig i lågkonjunktur efter den ovanligt

äventyrliga resan i tillgångspriserna måste alltså inte

historien upprepa sig.

Den ekonomisk-politiska reaktionen har varit så snabb och

kraftfull man kan begära och det är en viktig förklaring till

den vitt spridda uppfattningen att USA ska återhämta sig under

året.

Klas Eklund:

USA

har ryckt åt sig ett stort försprång och har världens

mest framgångsrika ekonomi

More about New Era

Top of page

Hoping for a recovery

Financial Times

editorial, January 19 2002

Recessions end. This one will be no exception. One can even identify the

sources of a turnround: the reversal of the worldwide collapse in manufactured

output. The question is whether this will be much more than the proverbial

dead-cat bounce. "Highly unlikely" is the answer.

To understand what lies ahead, one must start with the downturn. Not so

long ago people argued that new technology meant the end of the business cycle.

It is now evident that new technology has, instead, generated the cyclical

extremes - via the stock market bubble, the investment surge in high-technology

equipment and subsequent collapse, and the inventory cycle.

Can US consumers pull all these rusty freight cars along behind them?

With difficulty, alas. Normally, during a recession savings rates rise. This

provides the platform from which subsequent rapid rises in consumption begin.

But such a correction has not yet happened in the US.

On the contrary, US household savings remain very low, particularly

given rising unemployment and a stock market well below its peaks. Yet the

stock market is also, once again, highly valued, with a trailing price/earnings

ratio roughly double the historic average.

True, monetary policy has been loosened heroically. But the US Federal

Reserve's activism has not come through into lower long-term interest rates.

Top of page

A world without easy money

Martin Wolf,

Financial Times, Dec 11 2001 19:33:18 GMT

A little sunshine is breaking through the clouds of recession. That is

what equity markets are saying. The question is whether this upsurge in

optimism rests on reality or is a temporary high induced by a flood of cheap

money.

Scepticism about the wisdom of markets is warranted by experience.

Remember what they were saying about prospects for the high-technology sector

in March 2000, when the Nasdaq composite index reached 4,959, against just

1,992 on Monday.

It is equally wise to be suspicious of macroeconomic forecasts. In its

World Economic Outlook of October 2000, the International Monetary Fund

forecast world economic growth in 2001 at 4.2 per cent and the US at 3.2 per

cent. The latest consensus of forecasts suggests that the world economy will

grow by only about 1.2 per cent and the US by 1.1 per cent. Moreover, the

authoritative National Bureau of Economic Research has decreed that this

slowdown was well under way by September 11. It has now set the end of the

record-breaking US expansion in March.

The November consensus of forecasters was for growth next year of just

1.3 per cent in the world economy, with 0.7 per cent in the US, 1.5 per cent in

the eurozone and minus 0.6 per cent in Japan. Thereafter, mainstream forecasts

become more cheerful. The Organisation for Economic Co-operation and

Development forecasts growth in the OECD area of 3 per cent in 2003, with the

US on 3.8 per cent, the eurozone on 3 per cent and Japan on 0.8 per cent. The

OECD’s underlying view, again close to conventional wisdom, is that the

rebound will begin in the middle of 2002.

The strength of a recovery depends on what caused the downturn. The

standard explanation would include soaring oil prices during 1999 and 2000,

tightening of monetary policy during late 1999 and 2000, particularly in the

US, and the bursting of the high-technology bubble. These changes in background

macroeconomic conditions triggered a cutback in investment, a decline in demand

for manufactured output, an accumulation of unsold inventories and then a still

greater cutback in output. In the US, for example, output of manufactures in

October 2001 was 7 per cent below its peak in June 2000.

The slowdown has become global partly because the background forces -

higher oil prices, tighter monetary policy and the bursting of the

high-technology bubble - were also global. But between 1996 and 2000, the US

alone generated just under half of total world incremental demand, at market

exchange rates. With that gone, there was not much demand dynamism left.

September 11 was merely the coup de grace.

The justification for optimism is that these conditions have changed.

Oil prices are now down about 40 per cent in real terms from their peak in

2000. Monetary policy has eased dramatically, particularly in the US, with

short-term rates down 4.5 percentage points in less than a year. With inflation

subdued, there seems to be little constraint on further monetary easing. Fiscal

policy is also becoming more expansionary, particularly in the US. Aware of

this and aware, too, of the success of the first stage of the war against

terrorism, markets have recovered strongly: the Standard & Poor’s 500

is up 18 per cent from its low on September 21.

All this seems to justify expectations of a fairly normal recovery. Some

optimists suggest that the quantity of monetary petrol poured by the Federal

Reserve on the dying embers of the US expansion will even generate a vigorous

resurgence.

Alas, the opposite is more likely. The view that there will be a more or

less conventional recovery rests on the assumption that this was a conventional

downturn for which conventional demand management policies are an effective

remedy. But that cheerful view could turn out to be grievously mistaken.

The case for pessimism has two elements. The first is the dependence of

the world on US demand. The second is the fear that the US is now a post-bubble

economy. The argument has been well laid out by Stephen King of HSBC

(Decline and Fall - Bubbles, Busts and Deflation). Its analytical heart

goes back to non-Keynesian and non-monetarist views of recession. A period of

unwarranted optimism can generate exaggerated asset market valuations and

equally inappropriate investment. A consequence is likely to be falling

propensities to save. These will be associated with rising indebtedness, in

relation to incomes if not to (temporarily) elevated asset values.

The US in the 1930s and Japan in the 1990s were the 20th

century’s most spectacular examples of post-bubble economies. Mr King

argues that it is particularly difficult for very large economies to grow out

of post-bubble corrections, because they cannot easily use the rest of the

world as a source of demand. The US can hardly do so today.

This description fits the US experience of the 1990s disturbingly well.

If one takes the cycle as a whole, economic growth, at 3.1 per cent a year, was

no faster than in the 1980s and far slower than in the 1960s. The stock market

reached a valuation peak never seen before in history. The share of

non-financial corporate profits in non-financial corporate gross domestic

product recovered strongly during the 1990s, only to fall back to the levels of

the early 1980s. There was a big investment surge in the private sector, while

household savings rates fell. The wealth held in the stock market soared by

$12,000bn between 1994 and 2000, equal to more than six years of normal gross

saving in the economy. Why save when the stock market does it painlessly for

you?

The US is now in what Mr King calls an “unplanned recession”,

one that the policymakers did not want and desperately wish to halt. This is a

correction that originates more in disappointment than in overheating. But the

correction among households has hardly begun. It is also this that easy money

is intended to prevent.

If this view of the forces at work is correct, a normal postwar recovery

is unlikely. More probable is an extended period of weak growth in private

demand, offset by a sizeable fiscal expansion but not, alas, by demand from

abroad. This then would be a limping recovery, stronger, no doubt, than

Japan’s in the 1990s but far indeed from the “new economy” of

the late 1990s.

Is this certain to happen? No. Is it likely? Yes. This story of

post-bubble correction is not yet over. It may have hardly begun.

Full

text

Top of page

A poor defence for

Klas Eklund

Rolf Englund share prices

Martin Wolf Financtial Times, Oct 23 2001

Europe's Economies Find Convergence, Easing

the Formation of Monetary Policy

Wall Street Journal, October 5,

2001

The economies of the euro zone are finally starting to move in step,

though unfortunately they're all heading in the wrong direction.

The convergence makes it much easier for the ECB to operate a

one-size-fits-all monetary policy.

Full

text

Monstruöst, sade

Economist (om stabilitetspakten)

Rolf Englund i EU-krönika i Nya

Wermlands-Tidningen 2001-08-30

Top of page

It’s time to come back down to earth

By Philip Coggan, Financial Times, October 5 2001

A share is just that - a share in the assets and profits of a company.

Its value depends on the current and future level of those assets and profits.

But for a while in the late 1990s, investors seemed to ignore those

fundamentals. They bought shares because they were going up and let the next

investor worry about things like assets or profits.

What about the professionals? When stocks were trading at 100 times

historic profits, it was pretty hard to recommend their purchase on the basis

of traditional valuation methods.

Did this mean that analysts told investors to sell such stocks? Not a

bit of it. Instead they went in search of new valuation methods that might

justify a holding in the stock.

There is a problem with many of these short cuts, however. Take the

price-earnings ratio. It may appear to provide a useful rule of thumb as to

whether a share is cheap or dear.

But the p/e is based on earnings per share, a figure which managers find

relatively easy to manipulate. To take just one example, when a company with a

high p/e uses its shares to make a successful bid for a company with a low p/e,

its earnings per share go up. This is nothing to do with whether the bid is a

business success.

In the late 1990s, many analysts shifted their attention away from the

p/e ratio and towards a measure based on “ebitda” (earnings before

interest, tax depreciation and amortisation). This measure was an attempt to

look at the cashflow available to service all the obligations of a company

(debt as well as equity) and allowed the comparison of companies with different

capital structures or accounting treatments.

Secondly, companies shifted to returning cash to investors via share

buy-backs, rather than dividend payments; in the US, in particular, buy-backs

had tax advantages. The UK government gave this change momentum by abolishing

the dividend tax credit in the late 1990s.

*A full discussion on valuation models appears in

Determining

Value: Valuation Models and Financial Statements by Richard Barker, published

by Prentice Hall.

Full

text

The troubles with technical trends

Barry

Riley, Financial Times, October 4 2001 19:35

Those eight years took in a stock market bubble. This in part reflected

favourable economic trends, and especially growth in corporate profits. But the

scale of the price rise also reflected uprating. When I started writing the

column, the S&P 500 offered a dividend yield of 2.7 per cent and a

price/earnings ratio of 23, falling to 16 in 1995: at the market peak in March

2000 the yield was just 1.07 per cent and the p/e ratio had reached 35.

This bubble was often presented at the time as being created by

day-trading amateurs, but it can be better viewed as a collective mistake by

investment professionals. How did it happen? Here are a number of the themes I

discussed during the late 1990s:

http://news.ft.com/ft/gx.cgi/ftc?pagename=View&c=Article&cid=FT34WZHVESC&live=true

U.S. Lost 199,000 Jobs in September

Oct. 5 (Bloomberg)

U.S. payrolls plummeted in September, posting the largest drop in more

than a decade, the Labor Department said in a report that doesn’t reflect

job losses after the terrorist attacks. Unemployment stayed at 4.9 percent.

Payrolls fell by 199,000 last month after declining by 84,000 in August,

as service businesses lost more jobs than factories did. The largest previous

drop, of 259,000, occurred in February 1991, toward the end of the last

recession.

Top of page

Summer of discontent

Barry Riley, Financial

Times, September 28 2001

This is turning into the worst bear market since 1973-74. It is not only

deep (a 37 per cent decline in the S&P 500 at its lowest close on September

21) but it has also been unusually long, with the Dow so far into the 21st

month of decline.

That compares with 23 months in 1973-74, when the total fall was 45 per

cent, and almost three years in the record-setting 89 per cent collapse between

1929 and 1932. In contrast, the peak-to-trough decline of 36 per cent centered

on the October 1987 crash was fitted into just 8 weeks.

This time it is different, as they say. In recent months the world has

been awash with liquidity, and bond yields have been relatively steady: no

problems there. It has been the valua tion error that has dominated: a vast gap

has become apparent between the incredibly optimistic future growth rate

implied by equity market levels at the peak and the rather sombre economic

reality now unfolding.

How this mistake happened is too complex a subject to discuss here now.

But some vital points are raised in a paper published this week by Bob Semple,

UK equity strategist for Deutsche Bank, entitled (with an arguably superfluous

question mark) The end of the equity cult? In particular, institutions

like pension funds and life insurance companies have accepted too much risk in

equities. The great bubb le turned out to be a disaster for risk contr

Gold

ol: the

current bear market represents a restructuring of portfolios in favour of safer

assets, notably fixed income bonds.

The puncturing of the bubble now under way bears a worrying resemblance

to the post-1929 Wall Street correction and the ending of the Japanese

"miracle" in 1990. Such a comparison would fit in with the extended nature of

the adjustment now taking place: but more optimistically, we can reasonably

hope that today's governments in the US and Europe will not make the mistakes

made in the early 1930s in the US, or more recently in Japan.

Full

text

Top of page

Global Recession—Longer and Deeper

Stephen Roach, Morgan Stanley

2001-09-25

Needless to say, this downwardly revised prognosis -- 1.9% average

growth in world GDP over the 2001-02 period—depicts a world in deep

recession. After all, 2.5% growth is usually viewed as the global recession

threshold. Moreover, if the verdict ultimately falls at the lower end of our

new risk range, it would qualify as the worst global recession of the

post-World War II era—both deeper and longer than the contractions of the

mid-1970s and early 1980s.

Full

text

Top of page

As The Implosion Begins . . .?

Prospects

and Policies for the U.S. Economy: A Strategic View1 Wynne Godley and Alex

Izurieta Jerome Levy Economics Institute, July 2001 (rev. August 2, 2001)

The U.S. economy is probably now in recession,2 and a prolonged period

of subnormal growth and rising unemployment is likely unless there is another

round of policy changes. A further relaxation of fiscal policy will probably be

needed, but if a satisfactory rate of growth is to be sustained, this will have

to be complemented by measures that raise U.S. exports relative to imports.

Full text

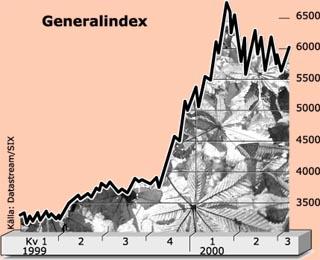

Över 2 600 miljarder kronor, eller 54 procent, av

börsvärdet den sjätte mars i fjol är borta. Det är det

tredje största raset någonsin på Stockholmsbörsen

mätt i procent och förstås det största mätt i

värde.

Bengt Carlsson i DN 2001-09-22

2001 tampas med Kreugererans 1931 om att vara det sämsta

börsåret någonsin, mätt i real kursuveckling. I

löpande kurser ligger ännu 1931 och börskraschåret 1929

något före 2001.

Ericsson slutade efter en liten uppgång i fredags 84 procent under

toppkursen från 2000. Det motsvarar ett tapp på ofattbara 1.500

miljarder kronor, mer än den svenska statsskulden, i värde.

I procent har Nokia klarat sig bättre, vilket är rättvist

med tanke på att det finska bolaget är det enda stora i sin bransch

som tjänar pengar, men nedgången från toppen är

ändå 69 procent, och fallet i börsvärde är med 1 750

miljarder kronor rent av värre än Ericssons.

Och ABB har, medan huvudkonkurrenten General Electric i fredags kunde

avisera att de håller fast vid sin tvåsiffriga vinsttillväxt,

gått från problem till problem. Kursen har fallit med 81 procent,

detsamma gäller Skandia det främsta exemplet på svensk

tjänsteexport och en tillväxtstjärna för världens

aktieinvesterare så sent som för ett år sedan.

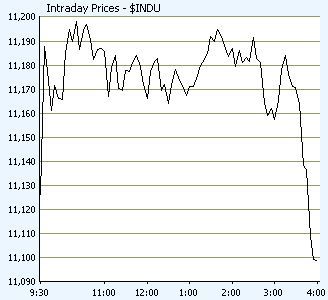

The great bear - Stock markets have been in

decline since early 2000.

Philip Coggan, Financial Times, September 21 2001

This is now one of the worst bear markets in history. In early trading

on Friday, the Dow Jones Industrial Average had fallen 31 per cent from its

January 2000 peak, one of the worst 10 declines the US market has experienced

since the first world war.

And the Dow has held up relatively well in global terms. In Germany, the

DAX index has more than halved since the peak in March 2000; in London, the

FTSE 100 has fallen 36 per cent since its peak in December 1999.

What has made the bear market all the more pernicious is its length. The

Dow peaked in January 2000 and many other bourses reached their highs in March

of that year. Markets have been falling, with the occasional rally, for 18-20

months. In contrast, it took only two months in 1987 for the Dow to fall from

peak to trough.

If one combines time and severity, only four other US bear markets since

1914 are more significant:

(Data taken from

Survive

and Profit in Ferocious Markets by John Rothchild, published by John Wiley

& Sons)

1919-21, when the Dow fell 47 per cent over 21 months in postwar

economic disruption; 1929-32, when the Dow fell 89 per cent at the start of the

Great Depression; 1939-42, when the Dow fell 40 per cent in the early stages of

the second world war; and 1973-74, when the Dow fell 45 per cent in the face of

Watergate and the oil price surge.

There have been significant effects on certain sectors in the short

term: Oliver North, speaking on CNN on Friday, said he was the only passenger

on a scheduled flight to New York.

Lower interest rates, in these circumstances, may not help. Who cares if

the return on cash falls from 3.5 to 3 per cent? At least by holding cash

investors are guaranteed the preservation of their capital.

The problem is that the valuation case is less clear cut than at the

bottom of previous bear markets. At the end of 1974, the Dow traded on a

price-earnings ratio of 6.2 and a dividend yield of 10.5 per cent; at

Thursday’s close, the Dow was on a p/e of 22 and a dividend yield of

slightly more than 2 per cent.

These still-high valuations (in historical terms) reflect the excesses

of the late 1990s bull market, when it was quite common to argue that such

measures were irrelevant. The dividend yield on the FTSE 100 index, for

example, moved above the 3 per cent level this week; but this level was seen as

a floor for dividend yields until recent ye

Full

text

Augusti kommer före september

Rolf

Englund i mail 2001-09-20

Det som hände i augusti kan inte ha påverkats av det hemska

terrorattentatet, vilket skedde i september, och som av allt att döma inte

låg i marknadens förväntningar.

Den avmattning som CNN rapporterar om i dag kan således inte

skyllas på muslimska fundamentalister.

Vad kan den då skyllas på?

Sossarna förståss. Och 68-vänstern som åter har

börjat röra på sig?

Nja, det kan ju också vara så att att den bubbla som nu

brister, redan hade börjat brista i augusti, och dessförinan ,som

alla innehavara av Ericsson anar.

Då var det alltså en bubbla.

Om det var en bubbla var det ingen ny Era.

Om det inte var någon ny Era kan den nya eran inte har berott

på Ronald Reagans skattesänkningar i början på

1980-talet, vilket våra egna talibaner plägar hävda i sina

spalter.

- We are all Supply-Siders (vi vill sänka skatterna) now, hette det

förut.

Nu hoppas alla på att de amerikanska hushållen, som redan

köper för mer än 100 procent av sina disponibla inkomster, skall

ta fram sina kreditkort och ytterligare öka sin skuldsättning.

Soon we will all be Keynesians again.

Utom talibanerna förstås.

Dessa tankar fick jag vid läsning av nedanstående

nyhetstelegaram.

“Housing starts tumbled in the United States last month as what has

been a pillar of strength in the world’s largest economy showed some signs

of weakness. Groundbreaking on new homes and apartments fell 6.9 percent to a

seasonally adjusted annual rate of 1.53 million units in August from July.

Economists surveyed by Briefing.com expected housing starts at a rate of about

1.63 million.” (CNN 2001-09-20)

The Vision Thing - Why

people don't understand

Rolf Englund på internet 1999

Fler av mina bästa

artiklar

Uncertainty

By John H. Makin

American Enterprise Institute

October 2001

The employment report for August released in early September showed a

jump in the unemployment rate from 4.5 to 4.9 percent. Hours worked, the

broadest indicator of the path of total economic activity, fell at a 2.9

percent annual rate during July and August. That level, unlikely to be reversed

in September, is consistent with third-quarter annual growth of about minus 2

percent-i.e., a contraction of the U.S. economy-well below what had been the

consensus in early September. The employment data forced second-half growth

forecasts to be lowered while increasing the amount of expected Fed easing.

Again, before September 11, emerging signs of further excess capacity

and disinflation or outright deflation (as in Japan) promised continued

pressure on profits and further layoffs as companies attempted to cushion the

negative impact of shrinking demand on profit margins. Underscoring the global

breadth of this trend, second quarter nominal GDP growth in Japan was reported

early in September to be falling at an annual rate of 10.7 percent. Profit

growth simply cannot revive until prices stop falling, because the response to

falling prices, accelerated layoffs, will weaken demand further and cause

prices to continue to fall.

The global economic slowdown had, in short, reached a self-reinforcing

negative phase by September 11. Attempts by companies to preserve profit

margins were leading to more layoffs, which by reducing demand growth and

accelerating deflation further, produced an additional negative feedback effect

on profit margins.

Englund om detta

http://www.aei.org/eo/eo13322.htm

Det ser mörkare ut än på länge

Bengt Carlsson

i DN 2001-09-20

Börsvärdet har nu fallit med närmare 37 procent sedan

årsskiftet, lägg till tre procents inflation och den reala

nedgången är 40 procent. Samma nivå som finans- och

fastighetskrisens 1990, då dock den nominella kursnedgången

.htm">James Grant

Full

text

Those who argue that the Dow is now a ‘bargain’ may be

highly delusional.

Dow Jones Industrial Average—August 31, 2001:

Price-to-Book: 4.61

Price-to-Earnings: 26.76

Price-to-Sales: 2.44

Dividend Yield%: 1.75%

Full

text

IMF warns of a significant danger of

global recession

Financial Times, August 30 2001 19:43GMT

Economists at the International Monetary Fund have warned of a

“significant danger” of a global recession along the lines of the

early 1980s and early 1990s.

A leaked draft version of the IMF’s World Economic Outlook,

obtained by Financial Times Deutschland, predicts the world economy will grow

by 2.8 per cent this year but states that there could be “a much deeper

and more protracted global downturn”.

The focus of the IMF’s concern is the outlook for the US. Although

the IMF forecasters have not changed the prediction made in April that the US

will grow by 1.5 per cent this year and 2.5 per cent next year - roughly in

line with the US administration’s expectations - they see a serious risk

of a much worse outcome.

If US productivity growth is less than expected, then stock markets

could fall, triggering sharp declines in business investment and private

consumption. That would cause a global recession, and possibly

“substantial financial market turbulence”, including “a possible

abrupt decline in the value of the dollar”.

The impact of global recession and market turbulence might be

particularly severe for developing countries, the IMF economists note.

The IMF’s economists argue that the impact of a US recession on the

world economy would be made more severe by the weakness of the economies of

Japan and Europe.

The World Economic Outlook is to be published ahead of the

IMF’s annual meetings at the end of next month. It may be revised after it

is discussed by the IMF’s executive directors next week but is unlikely to

be substantially changed.

Full

text

Forget the Second-Half Recovery

By John H. Makin resident scholar

at the American Enterprise Institute

August 2001

Every time I hear a typical analysis of the U.S. economy in 2001, with

its components of global recession, investment collapse, falling profits,

record deterioration of household balance sheets, and the rising need for

companies to lay off more workers, I wonder when the analysts are going to

lower their U.S. growth forecasts for the second half of this year.

Notwithstanding a positively awful set of economic conditions, most forecasts

from investment firms call for a 1, 2, 3 scenario: 1 percent growth in the

second quarter, 2 in the third, 3 in the fourth.

The “easy as 1, 2, 3” recovery outlook is beginning to look

like a bad joke. It is based on the simplistic notion that 275 basis points of

Federal Reserve easing since the start of this year, together with a

combination tax cut–rebate that adds about $40 billion to household income

in the third quarter, will boost spending enough to justify the 1, 2, 3

scenario.

Rather, rate cuts appear to have helped sustain a high level of

household spending on autos and housing, but one result of that sustained

spending has been a sharply elevated level of household debt.

Interest payments on consumer installment debt are soaking up 3.1

percent of disposable personal income, by far the highest level since 1968,

when a continuous data series began.

As a result, U.S. consumer installment debt is also at a record high, 22

percent of GDP, while total consumer and corporate debt has reached 135 percent

of GDP.

With debt-service burdens at record levels relative to incomes, will

U.S. households keep spending and running up more debts just because the Fed

has pushed short-term interest rates down to “neutral”—that is,

neither stimulative nor contractionary—levels and a check for somewhere

between $300 and $600 arrives from the Treasury this summer?

It is time for economists to quit touting a second-half recovery.

Otherwise they will look as foolish as the equity (sales) “analysts”

who, every week, have revised downward their earnings forecasts by 2 percent or

more as negative “surprises” about prospective profits have flowed

in.

The sooner analysts acknowledge that the U.S. and global economic

slowdowns are intensifying—not abating—the sooner policymakers,

households, and corporations can undertake necessary, realistic adjustments and

the sooner the recession will be over.

Meanwhile, an unbecoming chorus of denial is only making a bad situation

worse.

Full text

Stockholm dyrast av Europas börser

DI

2001-08-14

Svenska börsen värderas i särklass

högst i Europa. Trots kursfallet de senaste 15 månadernas kursras.