|

Rolf Englund IntCom internetional

|

Monetarism

Finanskrisen/The Great Recession - Stabiliseringspolitik - Next Bubble: U.S. Government Bonds

“The process by which money is created is so simple that the mind is repelled.”

Click here

Recall that the conventional story in which banks merely channel existing funds from savers to those with investments to finance is wrong.

Banks create new money in the form of deposits when they issue loans.

This is why banking is an inherently unstable and destabilising activity.

Martin Sandbu, FT 1 March 2018

As many of you know, I have spent much of the last seven years explaining to anyone who will listen that banks do not "lend out" deposits or reserves.

Rather, they create both loan assets and matching deposit liabilities "from nothing" by means of double entry accounting entries.

Creating money with a stroke of the pen (or a few taps on a computer keyboard) is what banks do.

Frances Coppola, 29 October 2017

The Center for Financial Stability in New York "Divisia M4"

Let me introduce you to John Kenneth Galbraith.

He taught at Harvard University for many years and was active in politics, serving in the administrations of Franklin D. Roosevelt, Harry S. Truman, John F. Kennedy, and Lyndon B. Johnson; and among other roles served as United States Ambassador to India under Kennedy.

He was one of a few two-time recipients of the Presidential Medal of Freedom.

Clearly a pretty accomplished and stand-up kind of guy.

About money, he famously said:

“The process by which money is created is so simple that the mind is repelled.”

Only the ignorant live in fear of hyperinflation

Failure to understand the monetary system has made it more difficult for central banks to act

Martin Wolf, FT April 10, 2014

Fortunately the Bank of England is providing much needed education.

In its most recent Quarterly Bulletin, its staff explain the monetary system.

So here are seven fundamental points about how it really works as opposed to how people think it does.

The act of saving does not increase deposits in banks. If your employer pays you, the deposit merely shifts from its account to yours.

This does not affect the quantity of money; additional money is instead a byproduct of lending.

What makes banks special is that their liabilities are money – a universally acceptable IOU. In the UK, 97 per cent of broad money consists of bank deposits mostly created by such bank lending.

Banks really do “print” money. But when customers repay, it is torn up.

Understanding the monetary system is essential. One reason is that it would eliminate unjustified fears of hyperinflation. That might occur if the central bank created too much money.

But in recent years the growth of money held by the public has been too slow not too fast.

Asset price bubbles and Central Bank Policy

Money creation in the modern economy

Bank of England pdf, QB 2014 Q1

Lysande och pedagogisk

Too much state-created money is by definition a bad thing. And so is too little.

But how do we know how much is too much and how much too little?

It is a pity that the central banks decided to use the ugly term quantitative easing for what they were doing.

If they had called them “extended open-market operations”, or something similar, they would have had less explaining to do.

Samuel Brittan, Financial Times, October 31, 2013

Eurozone banks need to shed €3.2tn in assets to meet Basel III

Europe’s biggest banks will have to cut €661bn of assets and generate €47bn of fresh capital

Deutsche Bank, Crédit Agricole and Barclays the banks most in need

Financial Times, August 11, 2013

This is not about Mr Greenspan, or a single monetary policy decision at a particular time, or whether US interest rates were raised too late in the last cycle.

This question relates to the longer-term impact of monetary policy during the age of global disinflation,

which started in the early 1990s, and which has just ended.

The ECB, the Fed, and the Credit Crisis, Wolfgang Münchau. 07.11.2007

Wolfgang Munchau

Central bank money printing and the mystery of soaring shares

'Why did nobody see it coming?", the Queen asked four years ago on a visit to the London School of Economics,

a brilliantly faux naïve question that cruelly exposed the failings of modern economics.

Well, here's another in a similar vein she might like to ask when she next returns to matters financial.

"How come the stock market is going up, when the economy keeps tanking?"

Jeremy Warner, Telegraph 7 March 2013

It would certainly be nice to think so after five years of blood, sweat and tears, and I don't doubt that sentiment is a lot more positive than it was. Unfortunately, it's failing to filter through to the corporate world, where cash accumulation, not business expansion, continues to be the name of the game, at least as far as stagnant advanced economies are concerned.

Chief executives are not yet anticipating the strong cyclical upturn which stock markets seem to be pointing to. If companies themselves don't think highly enough of our economic prospects to start investing, how come investors do?

One reason is zero interest rates, allowing companies which, in a conventional recession, would have gone bust, to stay in business. At the same time, banks have been bailed out, so that bad debts have in effect been nationalised.

Taxpayers rather than investors are being made to pay the price for past excesses. The insolvency problem has been transferred from the private to the public sector.

The other related explanation is central bank money printing. This may or may not have prevented a much deeper economic collapse, but it has certainly put a rocket under asset prices.

As long as the central banks keep printing, equities will keep rising. Thus do central banks answer each successive bubble by blowing up another.

Eventually it becomes socially and politically unacceptable for companies to keep expanding their profits at the expense of labour.

The backlash is already beginning.

What is the use of economics if it cannot answer even such a basic question?

Two years ago at the height of the financial crisis, the Queen challenged staff of the London School of Economics with a simple but devastating question:

“Why did no one foresee this?”

The inability of professional economists in Britain and America to agree on something as important as whether

reductions in government deficits will accelerate or slow growth

Anatole Kaletsky, The Times September 29 2010

About six months later the cream of the British economics profession responded with a mealy-mouthed letter of self-justification from the British Academy, waffling on about “a failure of the collective imagination” and “the psychology of denial”.

Some of the developed world’s biggest central banks are trying deliberately to raise inflation.

Their continued failure to do so is arguably damaging the economy, but it boosts asset prices for investors.

If they were ever to succeed, then the relationship between inflation and stocks could itself begin to change.

John Authers, FT, 1 March 2013

A convenient market measure of expected inflation comes from bond market break-evens – the rates of inflation at which the returns on fixed-income bonds would equal the returns from equivalent inflation-linked bonds.

As the chart shows, the relationship between US 10-year inflation break-evens and stocks has been rigid, with the post-Lehman crash of 2008 coinciding with a deflation scare in which investors thought prices would actually fall over the ensuing decade.

Next Bubble Is Forming: U.S. Government Bonds

It must be flattering for Shinzo Abe, a man whose knowledge of economics is matched only by Ben Bernanke’s expertise in ikebana flower arrangement, to have a whole new branch of the dismal science named after him. “Abenomics” has proved such a potent force that its mere invocation – before any real action to speak of – has helped knock a fifth off the value of the yen and put a third on the value of Japanese equities since October.

At the heart of Abenomics lies a simple, and entirely orthodox, proposition:

that deflation is a monetary phenomenon.

In Japan, where prices as measured by the gross domestic product deflator have fallen 18 per cent since 1994

David Pilling, Financial Times, 20 February 2013

For more than a decade, the orthodoxy in Japan – at least at the central banks – has been the reverse: that deflation is a “real economy” phenomenon, essentially beyond the reach of monetary policy to fix.

The case for helicopter money

I fail to see any moral force to the idea that fiat money should only promote private spending

Martin Wolf, Financial Times 12 February 2013

When arguing that monetary policy is already too loose, critics point to exceptionally low interest rates and the expansion of central bank balance sheets. Yet Milton Friedman himself, doyen of postwar monetary economists, argued that the quantity of money alone matters.

Measures of broad money have stagnated since the crisis began, despite ultra-low interest rates and rapid growth in the balance sheets of central banks,

Under fiat (that is, government-made) money the supply of reserves is potentially infinite.

True, central banks can pretend reserves are limited. In practice, however, central banks will advance reserves without limit to any solvent bank (and, as we have seen, to insolvent ones).

With central banks able to supply reserves at will, the constraints on lending are solvency and profitability. Expanding banking reserves is an ineffective way to increase lending, not a dangerous one.

Mer än 95 procent av alla pengar skapas i och av privata banker.

Pengaskapandet sker när banker beviljar lån.

Andreas Cervenka, SvD Näringsliv 2 september 2012

Money is a system of abstract tokens that complex societies use to manage the distribution of goods and services, and that’s all it is.

Money can consist of lumps of precious metal, pieces of paper decorated with the faces of dead politicians, digits in computer memory, or any number of other things, up to and including the sheer make-believe that underlies derivatives and the like.

John Michael Greer, January 22, 2013

Money and Credit – There Is A Difference

The Link between Money and Credit in the Fractionally Reserved Banking System

Pater Tenebrarum, December 18th, 2010

Their biggest fear following the denouement was a repeat of the interbank funding crisis that triggered all the manic activity by the Fed and ECB (beginning in late 2007 already), which were providing an alphabet soup of 'emergency lending facilities' for banks and other large financial players alike, that had all stopped trusting each other. The banks certainly don't like to have to rely on emergency funding by the Fed if they can avoid it. After all, you never know who will and who won't be bailed out (cue: Lehman).

Början på sidan - Top of pageCentral Bank's monetary policy was not the primary cause of

the persistant decline in inflation and long-term interest rates

Alan Greenspan, The Age of Turbulence, p. 14

Our knowledge about many of the important linkages is far from complete

and in all likelihood will always remain so.

Monetary Policy under Uncertainty,

Alan Greenspan, Jackson Hole, August 29, 2003

"Despite the extensive efforts to capture and quantify these key macroeconomic relationships, our knowledge about many of the important linkages is far from complete and in all likelihood will always remain so. Every model, no matter how detailed or how well designed conceptually and empirically, is a vastly simplified representation of the world that we experience with all its intricacies on a day-to-day basis. Consequently, even with large advances in computational capabilities and greater comprehension of economic linkages, our knowledge base is barely able to keep pace with the ever-increasing complexity of our global economy."

Full text

Monetary Policy under Uncertainty

Ben S. Bernanke, October 19, 2007

Början på sidan - Top of page

The Death of Paper Money

As they prepare for holiday reading in Tuscany, City bankers are buying up rare copies of an obscure book on the mechanics of Weimar inflation published in 1974.

Ambrose Evans-Pritchard, 25 Jul 2010

Ebay is offering a well-thumbed volume of "Dying of Money: Lessons of the Great German and American Inflations" at a starting bid of $699 (shipping free.. thanks a lot).

The crucial passage comes in Chapter 17 entitled "Velocity".

Each big inflation -- whether the early 1920s in Germany, or the Korean and Vietnam wars in the US -- starts with a passive expansion of the quantity money. This sits inert for a surprisingly long time. Asset prices may go up, but latent price inflation is disguised

As a signed-up member of the deflation camp, I think the Bank and the Fed are right to keep their nerve and delay the withdrawal of stimulus -- though that case is easier to make in the US where core inflation has dropped to the lowest since the mid 1960s. But fact that O Parsson’s book is suddenly in demand in elite banking circles is itself a sign of the sort of behavioral change that can become self-fulfilling

As it happens, another book from the 1970s entitled "When Money Dies: the Nightmare of The Weimar Hyper-Inflation" has just been reprinted. Written by former Tory MEP Adam Fergusson -- endorsed by Warren Buffett as a must-read -- it is a vivid account drawn from the diaries of those who lived through the turmoil in Germany, Austria, and Hungary as the empires were broken up.

The US money supply has experienced the sharpest contraction in modern history

"Monthly data for July show that the broad money growth has almost collapsed," said Gabriel Stein, the group's leading monetary economist.

Mish/Ambrose Evans-Pritchard, August 19, 2008

The US money supply has experienced the sharpest contraction in modern history, heightening the risk of a Wall Street crunch and a severe economic slowdown in coming months.

Today we tackle an economic concept called the velocity of money

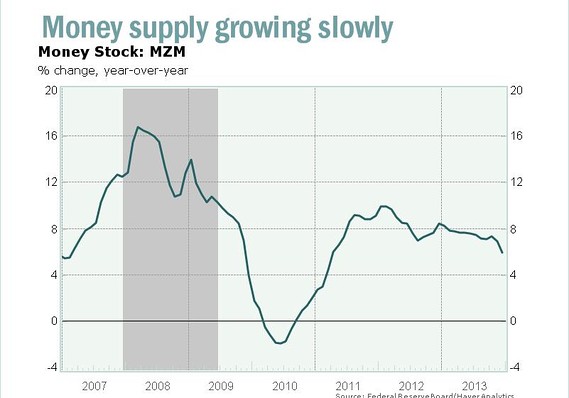

Is the Money Supply Growing or Not?

John Mauldin, April 25 2008

Let's start with a few charts showing the recent and high growth in the money supply that many are alarmed about.

The money supply is growing very slowly, alarmingly fast or just about right, depending upon which monetary measure you use.

In a short series of briefs we will analyze how single minded monetary policies and misguided micro oriented risk management created today’s financial markets’ mess.

The first brief argues that any simple minded, explicit and specific targeting procedure is bound to fail at some point since these are always too restrictive for the complexity of the macro economy.

Casper de Vries, Erasmus University Rotterdam, Eurointelligence, 11/2 2008

Many central banks currently operate under some form of inflation targeting. Monetary policy makers believed they had found the alchemist recipe for gold, as this latest fashion in central plan banking went hand in hand with years of low inflation. Suddenly there is this wake up call from financial markets and central bankers stand ready with liquidity. Are such infusions a logical consequence of this newest operating procedure, or is something else at stake?

History is rife with different targeting procedures, considering that the following targets have been used as intermediate goals towards reaching a central bank’s final objective: Money, domestic credit, exchange rate, nominal income and the interest rate. The Bank of England at least paid lip service to each of these targets at some point during the past fifty years.

In September 1992 the matter was decided for government by the markets.

The pound was bounced out of the ERM, but not till after a desparate last ditch battle, which cost the country still untold millions of pounds and the business community an undocumented number of heart attacks and near-suicides.

The day after the chancellor was singing in his bath, a few weeks on the British economy began to improve and in 1993 Norman Lamont left the government, clearly the intended scapegoat.

WILLIAM (Bill) CASH about Norman Lamont's book "Sovereign Britain".

Kronkursförsvaret 1992

Dom var inte ondskefulla, men deras inkompetens var förfärande

Läs mer här

Fed's interest-rate cuts may be a quick fix for 2008,

but they'll create a massive inflationary push in 2009,

leading us right back into another boom-bust cycle.

Jim Jubak, CNBC 5/2 2008

At the consumer level, headline inflation, which includes energy and food prices, hit a 17-year high in 2007 as the Consumer Price Index climbed 4.1%.

That's way above the Fed's 2% inflation target.

The core inflation rate, which excludes food and energy prices, climbed 2.4%, also above the Fed's target.

zc

The chance of an inflation shock may be higher than you think

Dan McCrum FT Alphaville 13 August 2018

Peter Berezin, Chief Global Strategist for BCA Research revisited the 1970s for lessons relevant to today, and finds that some common assumptions about the decade are wrong.

For instance, US inflation actually got going in 1966, long before the Bretton-Woods system of fixed exchange rates collapsed in 1971, and the oil cartel Opec prompted an oil price shock two years later.

Full textNext Bubble U.S. Government Bonds

Why am I not worried about an inflationary spike? Because monetary variables tell me so.

Lars Christensen 16 April 2018

Critics say the Fed is relying on a broken model and pays no attention to broad money data,

preferring backward-looking indicators such as unemployment and wage growth.

Ambrose Evans-Pritchard, 3 April 2018

This ‘New Keynesian’ outlook led to a series of mistakes in 2008

when it ignored red alert warnings from the monetary aggregates and allowed the incipient financial crisis to metastasize.

If foreigners use their dollars to build a factory in, say, South Carolina, our real economy gets a boost that neutralizes the circular flow’s leak. But if they only buy stocks and bonds in our financial economy, that shouldn’t provide as much of an offset to the leak.

Well, data show the foreign sector mostly draining dollars from our real economy and then investing them in our financial economy

ffwiley.com/blog/2018/02/26/an-inflation-indicator-to-watch-part-2/

In the past, I used the name “MDuh” for bank-created money, the measure Friedman and Schwartz studied, not the measures they popularized

For this article, though, I’ll use “M63,” referring to the year they published their work.

ffwiley.com/blog/2018/02/18/an-inflation-indicator-to-watch-part-1/

A rate rise this month — to which investors still ascribe a low probability — would be a serious mistake.

The risk is not just a sudden jolt to financial markets around the world.

An increase in borrowing costs now would also confirm suspicions that the Fed is working with substantially the wrong model of monetary policy in mind

FT editorial 9 September 2016

Lack of NGDP growth is the real reason for Italy’s banking crisis

The Market Monetarist, 7 July 2016

Ambrose via The Market Monetarist

The primary purpose of doing QE is — or should be — to expand purchasing power

John Greenwood, FT 30 May 2016

Money is TIGHT

We hear it all the time – central banks are printing money like no time before and

it is not working and now there is nothing more central banks around the world can do to fight deflation.

However, this is all a myth and this is what I will demonstrate in this post by looking at global money base growth.

The Market Monetarist 15 May 2016

Donald Trump Is Right: Deficits Don’t Matter.

Sounds a lot like Modern Monetary Theory (MMT)

New Republic 11 May 2016

Modern Monetary Theory (MMT)

Wikipedia

Since we commonly understand why lowering interest rates stimulates debt and economic growth,

and less commonly understand how QE works, I’d like to explain it.

Ray Dalio, founder and head of hedge fund group Bridgewater, FT 25 January 2015

Andreas Cervenka om Stephen Williamson och Hayek

Världsekonomins medicin sedan 2008 fungerar inte

Augusti 2015

Syntesen av Hayek, Friedman och Keynes,

mitt storhetsvansinniga och föga framgångsrika projekt

Rolf Englund 7 augusti 2015

Banks are Not Intermediaries of Loanable Funds – and Why This Matters

Yves Smith, June 19, 2015

Yves here. Over the years, we’ve regularly criticized economists like Bernanke and Krugman, who rely on the so-called loanable funds model, which sees banks as conduits of funds from savers to borrowers.

Despite the fact that many central banks, such as the Bank of England, have stressed that that’s not how banks actually work

(banks create loans, which then produce the related deposit), central banks still cling to their hoary old framework.

For instance, when I saw Janet Yellen speak at an Institute of New Economic Thinking conference in May,

she cringe-makingly mentioned how banks channel scarce savings to investments.

Even worse, the macroeconomic models used by central banks incorporate the loanable funds point of view.

This article describes what happens when you use a more realistic model of the financial system.

Even though the paper is a bit stuffy, the results are clear:

economies aren’t self-correcting as the traditional view would have you believe

but have boom/bust cycles (the term of art is “procyclical”) and banks show the effects of policy changes much more rapidly.

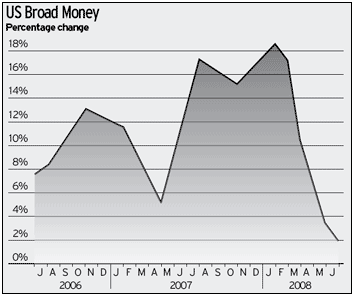

Bonds beware as money catches fire in the US and Europe

The broad M3 money

"Forecasters ignore broad money at their peril," says Gabriel Stein, at Oxford Economics.

A dynamic measure of eurozone M3 known as Divisia - tracked by the Bruegel Institute in Brussels - is back to growth levels last seen in 2007.

Ambrose Evans-Pritchard, 15 Apr 2015

Mr Stein said total loans in the US are now growing at a faster rate (six-month annualised) than during the five-year build-up to the Lehman crisis.

"The risk is that the Fed will have to raise rates much more quickly than the markets expect. This is what happened in 1994," he said.

That episode set off a bond rout. Yields on 10-year US Treasuries rose 260 basis points over 15 months, resetting the global price of money.

It detonated Mexico's Tequila crisis.

Next Bubble Is Forming: U.S. Government Bonds

It is with regret and sadness we announce the death of money on November 16th 2014 in Brisbane, Australia

G20 will announce that bank deposits are just part of commercial banks’ capital structure,

and also that they are far from the most senior portion of that structure.

With deposits then subjected to a decline in nominal value following a bank failure, will some investors prefer banknotes to bank deposits?

Such a change in preference is known as a "bank run."

Russell Napier of ERIC, via zerohedge, 11 November 2014

Dragi trollar fram 850 miljarder euro - men vad säger Bundesbank och Författningsdomstolen?

ECB pumps cheap cash into the banks through the targeted long-term loan program,

which kicks in next month and which Draghi says might supply 850 billion euros ($1.1 trillion).

Next, the banks lend that cash to companies.

They then bundle the loans together into asset-backed bonds,

and sell those securities to the ECB.

Mark Gilbert, Bloomberg View 8 August 2014

One of the lessons to emerge from the 1970s and 1980s is that it is difficult to define what money is.

All those naive souls who imagined that it would be dead easy to control inflation by controlling “the money supply” were on to a loser from the start.

Hence all that tortured travel along the various monetary motorways, M1, M2, M3, M4, which led nowhere.

In practice, different assets have different degrees of “moneyness”.

Paul Krugman is puzzled why it’s suddenly news that banks have the power to create money.

As he noted on his blog this week, it’s hardly something that contradicts standing economic theory.

We have, as he notes, known about the money-creation role of banks for a long time

Izabella Kaminska, FT blog Apr 30 2014

So why then is it suddenly such a talking point?

Who is it really that’s been misunderstanding the system for so long and how much damage has this been doing?

I’ve seen a number of people touting this Bank of England paper (pdf) on how banks create money as offering some kind of radical new way of looking at the economy.

And it is a good piece. But it doesn’t seem, in any important way, to be at odds with what Tobin wrote 50 years ago (pdf)

Paul Krugman 28 April 2014

One of the abiding truisms of economics is that growth doesn’t happen without credit expansion.

This is well explained in a recent paper by the Bank of England,

which points out that money in the modern economy is largely created by commercial banks making loans.

It is a common misconception to think that banks only lend what they can borrow from depositors.

Jeremy Warner, 24 March 2014

Money creation in the modern economy

Bank of England pdf, QB 2014 Q1

We believe strongly that monetary policy should be based on rules rather than on discretion.

But to change the wrong rules (inflation targeting) to the right rules (NGDP targeting) you need to make a discretionary decision.

The Market Monetarist 15 March 2014

Targeting the level of nominal gross domestic product - NGDP

A quiet revolution is sweeping over central banks.

The past five years have led central banks to a revolutionary situation.

Fed said it would keep interest rates close to zero until the US unemployment rate falls below 6.5 per cent (it is 7.7 per cent today).

For a central bank, let alone the Fed, to tie rates to the economy in this way was without precedent.

Robin Harding, Financial Times 14 december 2012

Deflation - A nightmare for the debt-stricken states of southern Europe, still trapped in a slump with mass unemployment

With Germany at zero inflation, they have to go into even deeper deflation to claw back lost competitiveness within EMU under "internal devaluations".

This, in turn, plays havoc with debt dynamics through the denominator effect.

Their debt loads are rising on a base of flat or contracting nominal GDP.

It is a key reason why Italy's public debt has risen from 119pc to 133pc of GDP since 2010 despite achieving a primary budget surplus

Ambrose Evans-Pritchard 12 March 2014

Mr Blanchard said their gains in competitiveness risk being overwhelmed by a rise in the "real value" of their debt.

Olivier Blanchard, the International Monetary Fund's chief economist.

Fotnot: Denominator = Nämnare (tal som står under bråkstreck) eller som man sade i skolan: Täljaren i topp, nämnaren nere

Euro Area — “Deflation” Versus “Lowflation”

March 4, 2014 by iMFdirect

Recent talk about deflation in the euro area has evoked two kinds of reactions.

On one side are those who worry about the associated prospect of prolonged recession.

On the other are those who see the risk as overblown.

This blog and the video below sift through both sides of the debate

Is there an inflation bubble?

For five years, two of the country’s leading economists have disagreed over whether billions of pounds of quantitative easing

will lead to uncontrolled inflation or a deflationary spiral.

Here Liam Halligan and Professor Tim Congdon try to settle their differences

Telegraph, 15 Feb 2014

MZM verkar vara gamla kära M1 eller M2 - http://en.wikipedia.org/wiki/Money_with_zero_maturity

No, the Fed doesn’t have a helicopter, why do you ask?

The growth of the money supply has actually slowed since the adoption of QE3.

In a $16 trillion economy, $1 trillion would be if that money were in circulation in the economy.

But most (if not all) of that money remains outside the economy, parked at the Fed

Rex Nutting, MarketWatch 14 February 2014

Yes, the Fed has conjured about $1 trillion in the past year to buy super-safe Treasury and mortgage-backed bonds from the private sector

in a bid to force investors to put their money into riskier investments that will help the economy grow a bit faster.

But most (if not all) of that money remains outside the economy, parked at the Fed in what are known as bank reserves.

The fact that bank reserves increased in 2013 by about $900 billion to about $2.5 trillion is often seen as a failure of the Fed’s quantitative-easing program,

because it shows that banks did not lend out their excess reserves.

(The topic of how bank reserves work is far too complicated for one column.

Interested readers can start with this paper by Paul Sheard of Standard & Poor’s: “Repeat After Me: Banks Cannot and Do Not ‘Lend Out’ Reserves” or with this paper,

“Why Are Banks Holding So Many Excess Reserves?” by a couple of New York Fed economists.)

Bernanke was tagged with the mocking nickname “Helicopter Ben” after he spoke of his certainty that, in a paper-money system, a “determined government” could always prevent deflation from occurring, even if it meant having to drop cash out of a helicopter to inflate the money supply.

The Fed doesn’t have a helicopter or its equivalent. It can’t drop cash out of the sky. Only the federal government can do that.

Helicopters are a tool of fiscal policy, not monetary policy.

Should there be another round of QE/helicopters, we must surely find a better way to inject the money.

Today’s method is enriching the uber-elites, with a painfully slow trickledown.

The better alternative is to stick the needle straight into the veins of the economy

- building roads, railways or nuclear power stations.

Ambrose 29 May 2013 with nice pic of Fed

Rolf Englund blog 5 december 2009:

Jag tycker det är skriande uppenbart att räntan världen över är för låg och att en större del av stimulanserna borde ske via finanspolitiken.

Men väljarna och därmed deras medlöpande politiker är rädda för budgetunderskott och vill hellre att villaägarna skall låna än att staten skall göra det.

Strategin synes vara att det gäller att stabilisera, helst höja, villapriserna så att konsumenterna främst i USA skall återgå till att konsumera med lånta pengar, dvs just det som ledde fram till katastrofen.

Full text

A long time ago, the debate between monetarists and Keynesians was the debate in macro.

But it was a rather limited debate: both sides generally used the same model (IS-LM), and so it was all about parameter values.

More recently, but before the recession, that debate had largely gone away, but since then it seems to have come back.

This post asks why that is.

Simon Wren-Lewis, an economics professor at Oxford University, and a fellow of Merton College, 6 January 2014

Before the recession, what I have called the consensus view was this.

Under flexible exchange rates, monetary policy was the instrument of choice for demand stabilisation.

Textbooks tend to give you a list of reasons why this is, but as I and colleagues argue here, it follows naturally in a New Keynesian model.

It is not because fiscal policy cannot stabilise demand, but because (in fairly simple cases) monetary policy is better at doing so.

Nobel laureate Christopher Pissarides earlier this week gave a lecture at the London School of Economics on the theme “Is Europe Working?”.

It is an extremely interesting lecture. I disagree with a lot of what professor Pissarides is saying. He focuses far too much on fiscal policy issues and far to little on monetary policy.

But it is in general a very enlightened lecture and he raises a number of extremely important questions about the future of the euro zone.

The Market Monetarist, 13 december 2013

Listen to Professors Pissarides’ excellent lecture here (I say this despite the fact he says in the end of lecture that he “was born a Keynesian and will die a Keynesian”)

PS I now know how uncomfortable Gustav Cassel must have felt agreeing more with Keynes than Hayek on the causes of and the solutions to the Great Depression.

PPS maybe the euro zone’s real problem is that European economists are all either Keynesians or Austrians (or should I say “Germans”?) Where are the European monetarists? And Market Monetarists?

One of the world’s leading economists will today admit he was wrong to back the creation of the euro – and call for it to be dismantled.

Sir Christopher Pissarides, who won the Nobel Prize for economics in 2010, was once a passionate believer in the benefits of the single currency.

But in an extraordinary change of heart, today he will warn the euro is creating a ‘lost generation’ of unemployed youngsters and is ‘dividing Europe’.

Daily Mail 12 December 2013

My trips to Sweden have once again reminded me about the dangers of conducting monetary policy with interest rates at the Zero Lower Bound (ZLB).

Lets say we can describe monetary policy with a simple Taylor rule:

r = rN+a*(p-pT)+b(ygap)

The Market Monetarist, 26 November 2013

Growth rates have remained stubbornly low and unemployment rates unacceptably high,

partly because the increase in money supply following QE has not led to credit creation to finance private consumption or investment.

Nouriel Roubini, Project Syndicate, 31 October 2013

Lysande och pedagogisk

Too much state-created money is by definition a bad thing. And so is too little.

But how do we know how much is too much and how much too little?

It is a pity that the central banks decided to use the ugly term quantitative easing for what they were doing.

If they had called them “extended open-market operations”, or something similar, they would have had less explaining to do.

Samuel Brittan, Financial Times, October 31, 2013

More silliness from the tin foil hat Austrians

The Market Monetarist, Lars Christensen 19 October 2013

I love reading the normally good blog posts on freebanking.org written by clever economists such as George Selgin and Kurt Schuler.

However, the Facebook page of freebanking.org very often fails to live up to the same good standards as the blog.

In fact most updates are what I consider to be internet-Austrian nonsense.

The freebanking facebook page is quoting an article by Lawrence J. Fedewa. I have never heard about him before, but his article is a pretty good example of the kind of "the-world-is-coming-to-an-end" nonsense,

which is floating around in cyberspace mostly written by tin foil hat Austrians.

As you may have seen, Japan’s public debt has hit one trillion quadrillion yen.

That is roughly $10 trillion. It will reach 247pc of GDP this year (IMF data).

No problem. Where there is a will, there is a solution to almost everything.

Let the Bank of Japan buy a nice fat chunk of this debt, heap the certificates in a pile on Nichigin Dori St in Tokyo, and set fire to it.

That part of the debt will simply disappear.

You could do it as an electronic accounting adjustment in ten seconds.

Ambrose Evans-Pritchard, August 9th, 2013

Or if you want preserve appearances, you could switch the debt into zero-coupon bonds with a maturity of eternity, and leave them in a drawer for Martians to discover when Mankind is long gone.

Fed’s policymakers want prices to go up because they believe that a little bit of inflation is good for growth.

The Fed wants interest rates to be below the rate of inflation to give homeowners

and businesses a strong incentive to borrow and spend, generating jobs.

The Fed can’t do that if there’s no inflation because interest rates can’t be lower than zero.

Bloomberg, 1 May 2013

The death of inflation

Central banks in the rich world may have been too successful in subduing price pressures

The Economist, April 13th 2013, print

Two flaws exist in the belief that the Fed can create rising aggregate demand.

First, they do not directly control M2. Second, velocity is almost entirely outside their control.

In order to understand how these two variables prevent the Fed from increasing aggregate demand,

it is necessary to become conversant with a few terms: monetary base, bank reserves, and money multiplier.

Hoisington Investment Management – Quarterly Review and Outlook, First Quarter 2013

via John Mauldin

Not only does the Fed not control money, but it cannot determine velocity (V), the speed that money turns over, either.

The great American economist, Irving Fisher, identified this connectivity between money and economic growth with a straightforward formula:

Nominal GDP equals money (as defined by M2) times its turnover (GDP=MV).

Presentation by Norges Bank governor

Have a look at the graph on slide 17 of the presentation.

The graph shows nominal GDP for what is called mainland Norway (“Fastlands-Norge”)

which is the non-oil part of the Norwegian economy.

The Market Monetarist 21 February 2013

Related posts:

Denmark and Norway were the PIIGS of the Scandinavian Currency Union

Danish and Norwegian monetary policy failure in 1920s – lessons for today

Fear-of-floating, misallocation and the law of comparative advantages

Money is a system of abstract tokens that complex societies use to manage the distribution of goods and services, and that’s all it is.

Money can consist of lumps of precious metal, pieces of paper decorated with the faces of dead politicians, digits in computer memory, or any number of other things, up to and including the sheer make-believe that underlies derivatives and the like.

John Michael Greer, January 22, 2013

Important differences separate these various forms of money, depending on the ease or lack of same with which they can be manufactured, but everything that counts as money has one thing in common – it has only one of the two kinds of economic value, use value and exchange value

All forms of real wealth – that is, all nonfinancial goods and services – have use value as well as exchange value. They can be exchanged for other goods and services, financial or otherwise, but they also provide some direct benefit to the person who is able to obtain them. All forms of money, by contrast, have exchange value but no use value. You can’t do a thing with them except trade them for something that has use value (or for some other kind of money that can be traded for things with use value).

For the last three hundred years, as industrial society emerged from older socioeconomic forms and became adept at finding ways to use the immense economic windfall provided by fossil fuel energy, there have been two principal brakes on economic growth.

The question is:

Is higher inflation the most painless way to escape current economic troubles?

The Economist, by invitation, October 2012

It is very clear that had it not been for the utterly damaging effects of the gold standard

on Germany’s economic and social well-being then Hitler and his Nazi party would never have gotten to power in 1933.

The Market Monetarist, 14 December 2012

Highly Recommended

So while the UK and the USA started to move out of the crisis and started economic and social recovery the result was nonetheless that both countries got dragged into a World War. I am not saying that that will happen again, but I certainly see the same commitment in continental Europe today to failed monetary policies as was the case in 1930s.

Dear Mario Draghi here is a few blog posts on 1930s economic and monetary history:

1931:

The Tragic year: 1931

Germany 1931, Argentina 2001 – Greece 2011?

Brüning (1931) and Papandreou (2011)

Lorenzo on Tooze – and a bit on 1931

“Meantime people wrangle about fiscal remedies”

“Incredible Europeans” have learned nothing from history

The Hoover (Merkel/Sarkozy) Moratorium

80 years on – here we go again…

“Our Monetary ills Laid to Puritanism”

Monetary policy and banking crisis – lessons from the Great Depression

1932: .....

Utan bindningen av pundkursen kanske Hitler i stället hade fortsatt som konstnär.

Monetarists from across the world can mostly agree on one thing.

The US Federal Reserve caused the Great Recession.

The "Bernanke Depression" if you want, a term gaining traction in elite circles.

Ambrose Evans-Pritchard, 23 September 2012

The indictment is a little unfair. The European Central Bank was worse. It raised rates into a deflationary oil shock in August 2008, and worsened a run on the dollar that constrained Fed actions.

There was little that Bernanke could do about the deeper causes of the crisis, whether the `Savings Glut' of Asia and North Europe, the `China Effect', the $10 trillion reserve accumulation by the world's rising powers.

Yet three heavyweight books now lay the blame squarely on the Fed: the 'Great Recession' by Robert Hetzel, a top insider at the Richmond Fed; 'Money in a Free Society' by Tim Congdon from International Monetary Research; and 'Boom and Bust Banking: The Causes and Cures of the Great Recession' by David Beckworth from Western Kentucky University.

Come on Bernanke, fire up the helicopter engines

Samuel Brittan, Financial Times, August 30, 2012

Quite why gold bugs think that the Gold Standard prevents asset bubbles and excess debt is beyond me. The 1920s saw US debt levels surge to around 300pc to 350pc of GDP.

It is very similar to what occurred in our own Noughties up to 2008.

As Paul Krugman says, Europe has replicated the worst features of interwar Gold with monetary union.

Ambrose Evans-Pritchard, August 29th, 2012

Folk är vana vid att man måste arbeta för att få pengar.

Dom, och tydligen många som anses lärda, har inte tagit till sig att man, om man är en riksbank, kan skapa pengar genom att skriva en summa på datorn och sedan trycka enter.Konsten är, som vi monetarister brukar säga, att skapa lagom mycket pengar.

Inte för mycket, då blir det inflation,

Inte för lite, då blir det massarbetslöshet

Läs mer här

Tea Party

In her parting shot on leaving the State Department, Hillary Clinton said of her Republican critics,

“They just will not live in an evidence-based world.”

Paul Krugman, Herald Tribune 10 February 10, 2013

Last week Eric Cantor, the House majority leader, gave what his office told us would be a major policy speech. And we should be grateful for the heads-up about the speech’s majorness.

Otherwise, a read of the speech might have suggested that he was offering nothing more than a meager, warmed-over selection of stale ideas.

The truth is that America’s partisan divide runs much deeper than even pessimists are usually willing to admit; the parties aren’t just divided on values and policy views, they’re divided over epistemology.

One side believes, at least in principle, in letting its policy views be shaped by facts; the other believes in suppressing the facts if they contradict its fixed beliefs.

"The Great Recession: Market Failure or Policy Failure?" by Robert Hetzel

A fresh US slump is not just a risk any longer. It has already begun.

Bernanke was not paying full attention because he disdains the quantity of money theory of Milton Friedman and countless others before him - including Keynes - as hocus pocus.

Yet the moneratists were right. They saw the steam engine coming straight down the tracks.

Ambrose 15 July 2012

The Federal Reserve has drifted into fatalism, seeming to lose confidence in its own ability to shape events, displaying the same lack of "Rooseveltian resolve" as the Fed in the early 1930s -- to borrow an expression written years ago by a young Princeton professor, and Fed scourge, called Ben Bernanke.

It is worth reading "The Great Recession: Market Failure or Policy Failure?" by Robert Hetzel from the Richmond Fed, the most damning critique ever published by a serving insider.

Bernanke has bought most of the bonds from the banking system. This is a bad way to boost the broad M3 money supply. You have to go outside the banks to gain traction, buying from pension funds, life insurers, and the general public. Don't say QE has failed in the US. It has hardly been tried.

Market monetarists around the world argue that central banks can always fight off slumps, whatever is thrown at them. But to do so policy-makers must stop targeting inflation -- the wrong variable, indeed a particularly bad variable -- and instead deploy nuclear force to drive up nominal GDP to a trend line growth rate of 5pc, doing so transparently so that markets know exactly what the objective is and when the stimulus will be unwound.

I have no doubt that this would bring about a full recovery very fast if conducted with enough panache, but is it possible to marshal political consent for such revolutionary action?

The Tea Party Congress, like Europe's bourgeousie, would rather wallow in liquidation, Puritan cleansing, and mass default than tolerate the possibility of a solution.

On the other hand, there is people who argue that

As every effort to re-inflate and perpetuate the credit bubble is made,

the words of Austrian economist Ludwig Von Mises lurk ominously nearby:

Peak Prosperity, 10 July 2012

Clearly the sugar rush from the ECB's 3-year credit blitz has worn off, leaving behind some very toxic effects.

Why anybody thought that a €1 trillion liquidity blitz through the banks is better than €1 trillion in genuine QE is beyond me.

Ambrose Evans-Pritchard, 30 May 2012

Those banks in Italy and Spain that used the money to play the Sarkozy redemption trade by purchasing sovereign debt – some with ten times leverage – are in serious trouble.

I think the ECB has twisted itself in knots to comply with a dysfunctional mandate, enshrined in the dysfunctional Maastricht treaty.

One error begets another.

Mario Draghi’s latest half-trillion blast of credit averts a funding crunch for crippled banks and crippled EMU states,

but raises the ultimate cost to catastrophic levels if the underlying crisis in southern Europe drags on into the middle of the decade.

Mr Draghi has won high praise from monetarists around the world,

convinced that he has acted just in time to head off a dangerous contraction of the money supply and a full-blown banking disaster.

"Draghi has been very astute, and has given the single currency project another lease of life,"

said Professor Tim Congdon from International Monetary Research.

Ambrose Evans-Pritchard, 29 Feb 2012

Something is changing in policy doctrine.

After a couple of decades in which the money supply almost disappeared from view it is now coming back

A new paper by Tim Congdon

Samuel Brittan, Financial Times 14/10 2005

”De stabila bolagen med hög kreditvärdighet är vältrimmade, effektiva och entreprenöriella.

Bara i USA sitter bolagen på 2.000 miljarder dollar i kontanter.

Om deras tillförsikt förbättras skulle de kunna använda pengarna till investeringar, nyanställningar och bolagsköp.”

Nouriel Roubini, DI 17 oktober 2011

...

För att betala kalaset skapar den schweiziska centralbanken nya digitala pengar. På en enda månad mer än fördubblades mängden centralbanksfranc, den monetära basen på fikonspråk.

Tidningen Financial Times konstaterade att det är en penningproduktion som till och med hade gjort centralbankschefen i tyska Weimarrepubliken avundsjuk.

Där slutade det med hyperinflation och kollaps 1923.

Andreas Cervenka, SvD Näringsliv 17 okt 2011

Is monetary policy too expansionary or not expansionary enough?

Martin Wolf blog June 27, 2010

Why it is right for central banks to keep printing

Martin Wolf, FT June 22 2010

The number of unemployed Americans fell by 350,000 - and the unemployment rate fell to 9.5 per cent.

But consider that this was mainly due to a reduction in the civilian labour force of 652,000 workers.

FT blog Moneysupply July 2, 2010

Marianne Nessén, doktor i ekonomi och biträdande chef för avdelningen för penningpolitik på Sveriges Riksbank

- Hur mycket pengar det finns i Sverige? Det är omöjligt att svara på

Hur mycket sedlar och mynt som finns vet vi förstås, det handlar om ungefär hundra miljarder kronor.

Men om vi pratar om pengar i vid mening är begreppet otroligt fluffigt och flexibelt. Jag kan inte sätta en siffra på det, säger hon.

Andreas Cervenka, SvD Näringsliv 2 okt 2011

Riksbanken besitter den mycket speciella förmågan att skapa pengar.

Runt ett långsmalt bord täckt av skärmar sitter en handfull personer. De övervakar betalningssystemet Rix, som är själva blodomloppet i finanskroppen.

Under krisen skapade Riksbanken pengar genom att i flera omgångar låna ut flera hundra miljarder kronor till de svenska bankerna. De fick lämna in värdepapper, till exempel obligationer, som säkerheter. Sedan satte Riksbanken in pengar som hamnade på bankernas konto i Rix.

Men hur går det egentligen till?

– Såhär, säger Per Kvarnström och knäpper med fingrarna i luften.

Vanliga medeklassmänniskor i Sverige har gjort mångmiljonaffärer på bostadsmarknaden med en belåning på 90 procent eller mer,

en nivå som skulle få vilken solbränd riskkapitalist som helst att skrika rätt ut av ångest.

Andreas Cervenka, SvD Näringsliv 2 okt 2011

Cantillon, en irländsk ekonom, bankir och börsspekulant på 1700-talet, var först med att poängtera att

effekten av penningpolitiken beror på de kanaler genom vilka nya pengar pumpas in i samhällsekonomin,

på vem som får pengarna och vad de används till.

Lars Jonung Kolumn DN 2009-12-17

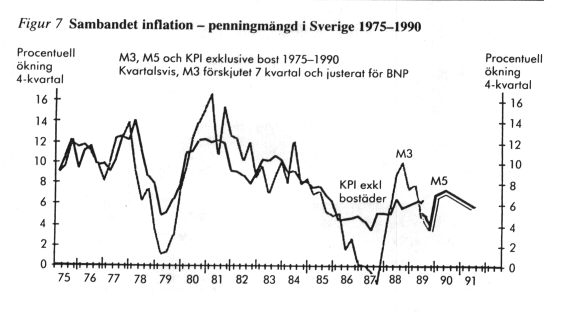

Monetarism

En del av uppgången i inflationen under 2007–2008 berodde inte bara på högre oljepriser

utan även på en monetärinflation, skapad av Riksbankens expansiva penningpolitik.

Det var därför som Riksbanken höjde räntan från 4,00 procent till 4,75 procent under 2008.

Fredrik NG Andersson, SvD Brännpunkt 2009-02-13

Doktor i Nationalekonomi vid Lunds Universitet

Vad är då problemet idag? Jo, Riksbanken fullföljde aldrig sin åtstramningspolitik och det höga underliggande monetära inflationstrycket finns därför kvar.

En av de genom historien mest pålitliga långsiktiga inflationsindikatorerna är tillväxttakten i penningmängden. Internationell forskning, och min egen forskning, visar att det finns ett tydligt samband mellan tillväxten i mängden pengar i ekonomin och inflationstakten.

Make Sure You Get This One Right

Are we facing a deflationary spiral or will the monetary

and fiscal stimulus ultimately create (hyper) inflation?

By Niels C. Jensen, at John Mauldin, 7/6 2009

Unfortunately, the answer is less straightforward. There is no question that, in a cash based economy, printing money (or 'quantitative easing' as it is named these days) is inflationary. But what actually happens when credit is destroyed at a faster rate than our central banks can print money?

The hedge fund industry is guilty of many stupid things over the years, but blaming it for the credit crisis is beyond pathetic and the suggestion that increased regulation of the hedge fund industry is going to prevent future crises is outrageously naïve.

We are effectively caught in a liquidity trap.

The Bank of England, the European Central Bank and the Federal Reserve have all flooded their banking system with enormous amounts of liquidity in recent months but what has happened?

Instead of providing liquidity to private and corporate borrowers as the central banks would like to see, banks have taken the opportunity to repair their balance sheets.

For quantitative easing to be inflationary it requires that the liquidity provided to the market by the central bank is put to work, i.e. lenders must lend and borrowers must borrow.

If one or the other is not playing along, then inflation will not happen.

This is illustrated in chart 3 which measures the growth in the US monetary base less the growth in M2. As you can see, the broader measure of money supply (M2) cannot keep up with the growth in the liquidity provided by the Fed. In Europe the situation is broadly similar.

Contrary to common belief, rising commodity prices can in fact be deflationary so long as demand for such commodities is relatively inelastic, which is usually the case for basic necessities such as heating oil, petrol, food, etc. The logic is the following: As commodity prices rise, money earmarked for other items goes towards meeting the higher commodity price and consumers are essentially forced to re-allocate their spending budget. This causes falling demand for discretionary items and can in extreme cases lead to deflation.

We only have to go back to 2008 for the latest example of a commodity price induced deflationary cycle.

Related

A repeat of the Great Depression is unlikely

Deflation is the ultimate economic calamity. This is also known as the liquidity trap.

Wolfgang Munchau, FT February 11 2008

Most rational investors accept the dual proposition that

a Fed funds rate pinned against zero and near-$800 billion of excess reserves sloshing around the banking system are not enduringly sustainable.

This is the case despite the fact that most – though a smaller most – applaud the Fed for engineering these outcomes, so as to cut off the fat tail risk of deflationary Armageddon.

Paul McCulley, June 2009

More articles by Paul McCulley at Intcom

MV=PQ

Okay, when you become a central banker, you are taken into a back room and they do a DNA change on you.

You are henceforth and forever genetically incapable of allowing deflation on your watch.

It becomes the first and foremost thought on your mind: deflation, we can't have it.

John Mauldin 24/4 2009

It's a bit misleading to talk about money supply,

because what money really is is roughly $2 trillion of cash and then $50 trillion in credit.

Because what do the banks do? They take deposits in and then they borrow money to leverage them up. I take my credit card and I spend with it.

I borrow against a house. I have an asset that rises, and I borrow against it.

John Mauldin 17/4 2009

Highly Recommended

If we all decided to settle and pay off everything, we couldn't do it because there is not enough cash. There would be massive asset deflation.

So we keep the system going. Now, where are we today? We are at the Great Deleveraging. We are seeing massive losses and destruction of assets, on a scale that is unprecedented. There was massive destruction of assets during the Great Depression, which caused a lot of problems, and we are seeing the same thing today. We are watching trillions simply being poofed (another technical economics term – which will drive my poor Chinese translator crazy!). We are watching people pay down their credit lines, which is one way of saying the supply of money and credit is shrinking.

This is not just in the US, but all over the world. Because when you start adding European cash-to-credit, and Japanese cash-to-credit, and Indonesian and Chinese cash-to-credit, it becomes multiple tens of trillions, and we are watching a goodly portion of that credit be vaporized. So we -- individuals and businesses -- are trying to find that $2 trillion in real cash and get some of it to pay down our debts. We are reducing that massive leveraged money supply down to some smaller number. We are hitting the Blue Screen of Death. We don't know what it is going to reset to, but we have permanently seared the psyche of the American consumer, and it is going to get reset to some lower number, about which I will speculate in a minute.

The main object of Alistair Darling, the British chancellor, is to inject more spending power into the British economy by a mixture of tax cuts and spending increases

The most frequent objection is to ask: “Where will the money come from?”

The short answer is: the Bank of England printing works in Debden.

Samuel Brittan, Financial Times, November 20 2008

This is not just a debating reply. In a paper currency system there is no fixed pot of money, but a total influenced by human action. The most interesting information in the Bank of England’s Inflation Report is a chart on page 11 showing that the annual growth of broad money and bank credit (excluding certain financial intermediaries) slowed from about 15 per cent early in 2007 to 5 per cent in the third quarter of 2008. In that quarter alone, real money growth (that is, adjusted for inflation) was negative for the first time since the early 1980s.

The most plausible argument against a fiscal stimulus is that by the time it takes effect, the economy will be in a boom and the effect will be destabilising. This may be valid for attempts to smooth out normal business cycles, but hardly for a possibly persistent slump.

The most plausible argument against a fiscal stimulus is that by the time it takes effect, the economy will be in a boom and the effect will be destabilising. This may be valid for attempts to smooth out normal business cycles, but hardly for a possibly persistent slump.

The last resort criticism is that increases in UK spending will leak abroad into imports. Fiscal stimuli are certainly more effective if countries act together. But countries do not have to move in lock-step; and a floating exchange rate is an invaluable safety valve for a country that is seen to move a bit further.

“But could we not avoid all these arguments by relying on monetary policy to reflate the economy?” There is a special reason for an emphasis on fiscal policy. Monetary policy works by encouraging people to borrow and spend. This must mean – barring an unlikely boom in business investment or net exports – an increase in consumer indebtedness which many observers think already too high. An increase in government debt is surely less dangerous.

More by Samuel Brittan at IntComThe Fed’s target rate is now back at 1 per cent, where it hit bottom in 2003.

As stress in the real economy intensifies, the Fed was right to use much of its remaining firepower.

Financial Times editorial 29/10 2008

Despite running at 4.9 per cent in September, inflation is no longer a major concern

Collapsing asset values may ignite a vicious cycle of depressed demand and falling prices. Policymakers have to do everything they can to avert this very effect – which exacerbated the Great Depression of the early 1930s and sunk Japan in its lost decade in the 1990s.

Who gives a damn about inflation?

Now that the age of moderation has ended, we are returning to Phillips curve-type discussion.

rising inflation is the most painless way out of a debt crisis

Wolfgang Münchau blog 31.01.2008

To put it in monetary policy terms, the Fed is boosting the supply of money to offset the decline in velocity,

which is the amount of turnover in the money stock.

Velocity has been falling like a newspaper stock amid the panic.

For our readers who recall their economic textbooks, Irving Fisher's famous equation is MV=PT.

Wall Street Journal editorial 30/10 2008

The supply of money times the velocity of money will equal the price level (inflation) times transactions, also known as economic output.

As velocity falls, the Fed is providing more dollar liquidity to prevent a steeper decline in GDP.

There is of course a danger in this, as Mr. Bernanke may recall from 2002 and 2003. That's when the Fed last worried about deflation and it's also the last time the Fed cut the fed funds rate to 1% and kept it there for a full year through June 2004.

We have since learned that this was a terrible error and helped to fuel the housing bubble and global credit mania.

Mr. Bernanke was a Fed governor (though not yet Chairman) at the time, and he and Alan Greenspan still don't admit this was a mistake.

The larger policy point is that it is a mistake to rely on the Fed and monetary policy to do too much. Mr. Bernanke's main obligation is price stability.

And if our politicians want to avoid a deep recession, they have fiscal policy -- specifically, the economy could now use a big, immediate and permanent cut in marginal tax rates. That would help to spur incentives to invest, as well as increase money velocity. We realize this policy mix isn't popular among the Democrats who expect to inherit all federal power next week. They're still proposing to raise taxes substantially amid a recession, and their only proposed stimulus is as much as $300 billion in new spending.

“inflationary expectations”

William White, until recently economic adviser to the Bank for International Settlements

has resisted heroically the temptation to say: “I told you so.”

Samuel Brittan, Financial Times, August 14 2008

Ingemar Bengtsson redogör helt korrekt i sitt inlägg på SvD Brännpunkt igår för skillnaden mellan inflation och förändringar i relativpriser. Men...

Stefan Ingves, riksbankchef, Irma Rosenberg, förste vice riksbankschef

SvD Brännpunkt 14/8 2008

Riksbanken bör skyndsamt ompröva sin räntepolitik och

noga analysera skillnaden mellan inflation och prisökningar.

Den akademiska diskussionen om inflationsbegreppet måste återupplivas

Ingemar Bengtsson, SvD Brännpunkt 13 augusti 2008

TMS: A Truer Money Supply?

TMS it stands for True Money Supply and it is a monetary measure based on Austrian economic principles.

Mish 14 July 2008

The Return of Inflation?

Robert J. Samuelson, June 24, 2008

We seem to be hostage to global forces. Economists Richard Berner and Joachim Fels of Morgan Stanley call this the "new inflation," because it's not easily squelched by domestic policies. Up to a point, that's true. Although the Fed influences interest rates, it doesn't own oil rigs or cornfields. Long-term price relief for oil involves switching to more-fuel-efficient vehicles and increasing worldwide, including American, oil production. Removing subsidies for corn-based ethanol would reduce food price pressures.

Still, all large inflations involve "too much money chasing too few goods," as economist Milton Friedman often noted, and this episode is no exception. The Fed's easy-money policies have global effects. Many countries peg their currencies to the dollar -- formally or informally -- and shadow Fed policies.

If there were a Central Bank of the World its monetary policy committee would glance at today’s inflation rates and expectations of future inflation and then raise interest rates.

There is no such bank, but there is something close: the US Federal Reserve, the monetary policy of which is mirrored by many countries in the Middle East and Asia.

low Fed interest rates are contributing to global inflation.

The Fed sets interest rates for Asian countries because, explicitly or not, they manage their exchange rates against the dollar.

If US interest rates are low, countries targeting the dollar are obliged to follow, because otherwise investors will sell dollars to buy their currency.

Financial Times editorial, June 25 2008

Barclays warns of a financial storm as Federal Reserve's credibility crumbles

US central bank accused of unleashing an inflation shock that will rock financial markets

Ambrose Evans-Pritchard, Daily Telegraph 27/6 2008

How imbalances led to credit crunch and inflation

Martin Wolf, Financial Times, June 17, 2008

Bernanke believes that the danger of a “substantial downturn” in the US economy has abated over the past month,

but that inflation risks are increasing.

FT June 10 2008

"Inflationen oroar mig eftersom ingen talar om den"

Göran Persson varnade för att Sveriges och många europeiska länders allt för "avslappnade inställning" till inflationen.

DI 2008-05-15

The measured savings rate out of disposable income fell to 2 percent

from its long-run average of 8 percent.

Just 2 percent of U.S. disposable income is $200 billion.

John H. Makin, April 30, 2008

The Inflation Solution to the Housing Mess

John Makin, Wall Street Journal April 14, 2008

via Tim Iacono

The policy alternatives in the post-housing-bubble world are painfully unpleasant. In my view, the least bad option is for the Federal Reserve to print money to help stabilize housing prices and financial markets. Yes, use reflation to soften the pain for Main Street and Wall Street. If instead we let housing prices fall another 25%-30% – as predicted by the Case-Shiller Home Price Index – it's almost certain that Washington will end up nationalizing the mortgage business.

While there is a substantial risk that inflation may rise for a time – this would be the policy goal – monetization is more easily reversible than nationalization of the mortgage market. Meanwhile, Fed officials concerned about inflation should rethink their view that it is impossible to identify an asset bubble before it bursts.

Riksbanken får beröm för att dom ljög

The International Monetary Fund last week gave central banks some wicked advice.

They should no longer ignore residential property prices when setting interest rates.

At the same time, the IMF recommends central banks should retain their inflation-targeting frameworks.

It all sounds very plausible. Unfortunately the two goals are inconsistent.

Wolfgang Münchau Financial Times April 6 2008

Who gives a damn about inflation?

Now that the age of moderation has ended, we are returning to Phillips curve-type discussion.

rising inflation is the most painless way out of a debt crisis

Wolfgang Münchau blog 31.01.2008

US headline inflation runs at over 4 per cent, and if you take the old pre-Boskin inflation measure, US inflation would be over 7 per cent.

(This is the inflation measure used during the Clinton era).

The Boskin Commission report introduced the principle of hedonic pricing, i.e. prices per utility consumed, so that technical progress at constant nominal prices enters into the index as a fall in prices. If you distrust such adjustments, as I do, you could in fact argue that reckless monetary expansion not only caused asset prices inflation, but also actual inflation.

The only argument one can make, and which the Fed is making, is that you can temporarily deviate from an inflation target to pursue other goals, as long as this deviation is temporary, and as long as you retain credibility.

One question I am asking myself - and I am not generally a conspiracy theorist - is whether the Fed reluctantly accepts the rise in inflation,

or whether a rise in inflation is actively pursued.

In a country with a negative savings rate, there is not going to be much opposition from bondholders,

and rising inflation is the most painless way out of a debt crisis

The consumer price index - CPI

Är det början till slutet på en gyllene global låginflationsperiod som vi nu bevittnar?

Ragnar Roos, signerat 18/1 2008

Sedan slutet av 1990-talet och en lång rad år framåt kunde världen njuta av ett osannolikt lågt inflationstryck. Inflationshotet var plötsligt mer avlägset än vad någon centralbankschef kunnat drömma om.

Att klara en låg inflation under de omständigheter som rått under det senaste decenniet har inte varit någon oöverstiglig uppgift för centralbankerna. Problemet har ofta varit det motsatta - att pressa upp inflationen som tidvis hotat att vändas i sin motsats - deflation.

På kort tid mer än fördubblades den globala arbetsstyrka som arbetade på en konkurrensutsatt marknad. Från Berlinmurens fall 1989 fram till 2005 ökade den från 300 till 800 miljoner. Det höll tillbaka pris- och löneökningar världen över. Kina har bidragit mest till denna desinflatoriska trend.

Vid någon tidpunkt kommer en vändning. När låglönearbetare strömmar till i en långsammare takt från risfälten, börjar också prispressen att avta.

Alan Greenspan, förre chefen för den amerikanska centralbanken, Fed, spekulerar i sina memoarer "Turbulensens tid" om när denna vändpunkt kan komma.

Krugman on monetary transmission channels

My guess remains that the US and UK will try to inflate themselves out of their troubles.

Wolfgang Munchau (Portal)

Should wealth-holders (both foreign and domestic) come to doubt the determination of the Federal Reserve to preserve the dollar’s domestic purchasing power, they might dump it, with devastating effects on its external value, long-term US interest rates and the US economy.

When wealth-holders look at the scale of indebtedness in the US, they might conclude that the Fed is indeed going to be under vast pressure to choose inflation.

Financial Times editorial 27/12 2007

The Fed has lost control of the money supply, because the banks it regulates no longer are the primary movers of debt creation.

From 1990 until the spring of this year, we saw the development of what Paul McCulley calls the shadow banking system.

Non-depository institutions and funds created massive amounts of new money based on leverage.

John Mauldin 2007-12-14

The obsession with M-2 or M-3 makes for good newsletter copy, but what do such broad aggregates mean in a world where new forms of money (SWAPs, derivatives, mortgages bonds, etc) appear every day?

The implication is that the old linear relationships between money supply (as measured by some arbitrary and outdated statistic like M-2) and inflation may no longer be valid.

John Mauldin 2007-12-14

My personal inflation expectations have gone up from something "close to, but above" 2 per cent to about 3 per cent

The first, and most important reason is that the ECB is not a true price stability advocate, but a central bank whose first priority is financial stability.

Wolfgang Münchau, Eurointelligence 5/12 2007

Financial companies' losses due to the US sub-prime crisis could be as much as $400bn

Goldman's chief economist Jan Hatzius predicts leveraged investors may have to reduce their lending by $2 trillion as a result.

"The macroeconomic consequences could be quite dramatic,"

Mr Hatzius said.

BBC 16/11 2007

Central banks should prick asset bubbles

Paul De Grauwe, FT November 1 2007

Deflation – not a monetary phenomenon

Unlike most economists, we at Cornerstone do not view deflation from a monetary standpoint.

This, we believe, is the mistake both Wall Street and the Fed are making.

Instead, we look at it from a businessman’s perspective.

John Riley, 03/12 2007

The US subprime lending fiasco and its repercussions on Northern Rock have brought back questions about the banking system

- questions such as “What is a bank?” and “What is money?”

Samuel Brittan, FT October 25 2007

The wolf packs are circling. Hedge funds target currency pegs

Fifteen years after George Soros smashed the sterling and lira pegs of Europe's Exchange Rate Mechanism, central banks have invited hedge funds to pounce again. This time on a global scale.

Ambrose Evans-Pritchard, Daily Telegraph 15/10/2007

The global M3 money supply is growing at 10.6pc as stimulus from America, Europe – and Japan, through the carry trade – leaks out to the vibrant parts of the world economy... With the usual lag, inflation has at last hit.

The easiest prey are in the Baltics and Balkans, where EU newcomers have let rip by importing an ECB monetary policy designed for the slow barges on the Rhine. All are overheating.

Inflation is now 11pc in Latvia, and 7pc in Estonia and Lithuania. Property prices in the capitals of all three are more expensive than Berlin. Inflation is 12pc in Bulgaria and 6pc in Romania.

The ECB has now invited the wolves to kill...... more

Tim Iacono: Good afternoon.

Alan Greenspan: Good afternoon. My assistant tells me you've been writing about me.

Iacono: A little. Let's get right to the point. Are you responsible for the housing bubble?

Greenspan: No.

Iacono: Would you care to elaborate on that?

Tim Iacono 4/10 2007

The advocates of inflation targeting have never faced

any really difficult choices - until now.

Wolfgang Münchau 03.10.2007

Over the last fifteen years, many soft-money advocates were able to jump on the inflation targeting bandwaggon. No longer did they need to declare: I’d rather have 10% inflation than 10% unemployment. They could have their cake and eat at the same time. Inflation targeting allowed them to pretend that they really did care about inflation.

Another 100bp in rate cuts, to be spread over six months, is not going to be enough to stop the recession, but it may be just enough to shift long-term inflationary expectations upwards.

The shadow banking system of hedge funds and CDOs, CLOs, PIPES, etc.

I'm sure that Bernanke, Paulson, and their cohorts understand this, but...

Bill Gross 1/10 2007

No president tried harder, with good reason, to influence the business cycle than Franklin Roosevelt.

When he took office in 1933, unemployment was roughly 25 percent. By executive order and congressional legislation, FDR effectively abandoned the gold standard, adopted deposit insurance, tried to prop up falling farm and factory prices, rescued many defaulting homeowners, regulated the stock market, and embarked on massive public works.

With what result? Well, leaving the gold standard aided recovery. But some economic research suggests that other New Deal measures may have frustrated revival. In any case, all of them together didn't end the Great Depression.

World War II did that. In 1939 unemployment was still 17 percent.

We have a $14 trillion economy. The idea that presidents can control it lies between an exaggeration and an illusion.

Robert J. Samuelson, Washington Post, February 6, 2008

Do Not Forget About Changes in Velocity

As we never tire of pointing out, there are three things that a central bank can control:

the growth rate of its money supply, its interest rate, or the value of its currency.

Unfortunately, as the Chinese central bankers are now discovering,

it cannot control all three at the same time.

Louis-Vincent Gave, Charles Gave, Anatole Kaletsky, and company

John Mauldin, 24/9 2007

This week in Outside the Box, Louis-Vincent Gave, Charles Gave, Anatole Kaletsky, and company of GaveKal Research delve into the underlying misconceptions that presumes money velocity is and will remain constant, in the equation that says MV = PQ (Money*Velocity = Prices*Quantity) when M is increased.

It has been said that smart people learn from their mistakes (and do not repeat them) and that very smart people learn from other people's mistakes.

In 2001, when the Fed, the BoJ, the BoE and even the ECB started to dump money into the system, we gleefully assumed that either prices or activity would start to pick up over the coming quarters.

After all, hadn't Irving Fisher taught us that MV=PQ (Money*Velocity=Prices*Quantity)?

And hadn't the monetarist school shown that, over the life of a cycle, velocity was a constant? So couldn't we assume that an increase in M would invariably lead to a rise in either P or Q?

As highlighted on the previous page, the $100bn question for investors now has to be whether the world's commercial banks will actively multiply the money

that the Fed (and other central banks) have been injecting into their economies over the past few weeks.

If they do, then the world should witness a roaring boom of unprecedented magnitude.

If they do not, then the investment environment will have changed.

Three reasons why velocity is unlikely to accelerate

1. OECD banks' balance sheets are already stretched

2. Ratings agencies have lost investors' trust

3. Regulators and lawmakers will fall on the back of banks like a ton bricks

In 1933, Mellon famously advised Roosevelt to "liquidate labour, liquidate capital, liquidate the financial markets. It will lead to a much more moral society."

This, better than any other statement, encompasses the "perma-bear" philosophy:

Sinners have to pay for their sins; and when the central banks step in to give sinners a helping hand, this can only ensure eternal damnation for the rest of us

(either in the fires of an inflationary bust, or those of a deflationary bust, depending on the perma-bear to whom you speak).

As we never tire of pointing out,

There are three things that a central bank can control:

the growth rate of its money supply,

its interest rate,

or the value of its currency.

Unfortunately, as the Chinese central bankers are now discovering, it cannot control all three at the same time.

Kommentar av Rolf Englund:

Det förstod inte Bunkergänget - därav katastrofen och

därför är det bra att ha en egen valuta.

Nils-Eric Sandberg förstod det och skrev om det för längde sedan i en elegant text (DN 18/9 1987):

"Både teori och erfarenhet säger att staten kan styra bara en av de tre variablerna, ränta, inflationstakt och växelkurs.

Staten kan fritt välja ut vilken av de tre ska fixeras, men bara en.

Ty två av dessa variabler blir i längden alltid en funktion av den tredje.