- There is no such thing as rational expectations.

There is wishful thinking, or panic.Rolf Englund, many years ago

(probably in 1997)

Economics failed us before the global crisis

Analysis of macroeconomic theory suggests substantial ignorance of how economies work

Martin Wolf FT 20 March 2018

The core macroeconomic model rested on two critical assumptions: the efficient markets hypothesis and rational expectations. Neither looks convincing today.

It is questionable whether it is even possible to have “rational expectations” of a profoundly uncertain future.

Socrates might say that awareness of one’s ignorance is far better than the illusion of knowledge.

If so, macroeconomics is in good shape.

Full text

Mervyn King

Top of page

Bookstaber

As Queen ELIZABETH II famously once pointed out, most economists failed to predict the crisis of 2007-08.

In a lecture to the American Economic Association in 2003, Robert Lucas argued that macroeconomics had succeeded

in so far as the “central problem of depression prevention has been solved, for all practical purposes”.

Yet within five years the world faced its worst crisis since the 1930s.

The Economist Print 18 May 2017

The analysis is top-notch, and anyone who wants to understand the workings of the financial system will benefit from reading this book. But those looking for a quick fix will be disappointed.

The End of Theory: Financial Crises, the Failure of Economics and the Sweep of Human Interaction

By Richard Bookstaber. Princeton University Press

Full text at The Economist

A brief history of macro

How we got here

The Economist, 21 Januiary 2013

A new generation of macroeconomists, including Ed Phelps, Robert Lucas, replaced the mechanistic “empirical” models with ones that were simple and elegant — just a handful of equations in most cases.

Instead of plugging in aggregate variables like the number of hours worked or the level of retail sales,

these new “dynamic stochastic general equilibrium” (DSGE) models were based on individual households and businesses that

tried to do the best they could in a challenging world.

It is easy to mock the techniques used by these revolutionaries. No one actually makes day-to-day decisions while thinking about how to maximise the net present value of their future income.

The founders of DSGE also chose to ignore the banking system for the same reasons as their “Keynesian” forebears.

Despite these many drawbacks, DSGE models got one big thing right: they could explain “stagflation”

Full text

But anyway, in macro, most models use Rational Expectations,

so let's think of "behavioral" as just meaning "non-RE".

I'm seeing macro people taking behavioral ideas more seriously.

Noahpinion 15 January 2017

From the start of his academic career in the 1950s until 1996, when he died, Hyman Minsky laboured in relative obscurity.

His research about financial crises and their causes attracted a few devoted admirers but little mainstream attention:

this newspaper cited him only once while he was alive, and it was but a brief mention.

So it remained until 2007, when the subprime-mortgage crisis erupted in America.

Suddenly, it seemed that everyone was turning to his writings as they tried to make sense of the mayhem

The Economist 30 July 2016

In 2013 economists at the IMF rendered their verdict on these austerity programmes:

they had done far more economic damage than had been initially predicted, including by the fund itself.

What had the IMF got wrong when it made its earlier, more sanguine forecasts?

It had dramatically underestimated the fiscal multiplier.

The Economist print 13 August 2016

Highly Recommended

“I’d never believed in the efficient market hypothesis or the rational expectation hypothesis.

But I’d forgotten that banks create credit, money and purchasing power and that they can create too much.

Adair Turner, FT 16 June 2016

Adair Turner became chairman of Britain’s Financial Services Authority just as the global financial crisis struck in 2008,

and he played a leading role in redesigning global financial regulation.

Read more here

What causes asset bubbles?

Most econ models are still based on rational expectations,

the idea that people don’t systematically make errors when forecasting the future.

This idea was advanced by many star economists of the 1970s and '80s,

including the highly influential macroeconomist Robert Lucas.

Noah Smith, Bloomberg 8 December 2016

But in finance theory, economists have had more freedom to experiment.

So a small but increasing number of papers are asking how markets would behave

if investors improperly extrapolate recent trends into the future.

Full text

Asset price bubbles and Central Bank Policy

House prices

Top of page

A great critique of Rational Expectations

Charles Manski paper in 2004 in Econometrica looking at the way economists measure expectations.

Noah Smith. August 22, 2015

Full text

News

The slow march away from Rational Expectations continues.

Recently more and more people are challenging this most powerful of all ideas in modern macro.

Noahpinion, July 24, 2015

You have Woodford's 2013 survey of alternative approaches. More recently you have Woodford's bounded-rational New Keynesian model, which he used to answer the challenge of the Neo-Fisherians.

In finance you have Greenwood and Shleifer measuring expectations with surveys and you have people making models with various kinds of irrational expectations, e.g. extrapolative expectations.

It's not yet a flood, but it's an increasingly large trickle.

Full text

C+I+G+Exp = BNP. Här en nyttig och lättläst uppfriskning

Rational expectations

Romer roots the sorry state of academic macroeconomics in a battle between Robert Lucas and Thomas Sargent

Martin Sandbu, FT 17 Augusti 2015

For months, Paul Romer, the economics professor, has been on a crusade against what he calls “mathiness”,

by which he means deliberately abstruse use of mathematics to camouflage political arguments by economists.

Romer has now written a new long post on his blog that is a good way in for those interested.

Another comment on economic intellectual history and its real-world implications comes courtesy of John Cochrane.

Cochrane picks up on Paul Krugman’s seemingly serious celebration of the “MIT gang”.

It may not be known to most, but an astonishing number of economists with international policy influence were trained at MIT in the late 1970s and the early 1980s, including Ben Bernanke, Olivier Blanchard and Mario Draghi.

Full text

The sorry state of academic macroeconomics

Top of page

News

Romer: a new trend in economics is polluting the discipline, names Robert Lucas

UNDERCOVER ECONOMIST Tim Harford, FT June 5, 2015

In about 1980, there was a big change in the way academic economists did macroeconomics.

Since 2009, there has been a big debate in the economics blogosphere about whether academic econ took a wrong turn when it switched tactics

Noah Smith, Bloomberg, 12 December 2014

The old method was to write down a system of equations representing macroeconomic quantities (gross domestic product, investment, etc.).

The new way was to write down an optimization problem, representing the decision-making of one or more agents in the economy.

This approach is called DSGE (short for Dynamic Stochastic General Equilibrium).

The old approach is sometimes called IS-LM which refers to the name of two curves in a graph in a classic model; they are also referred to as Old Keynesian models.

Full text

Economic theory discredited

The field of economics is desperately in need of a paradigm shift if it wants to play a role in improving the lot of humanity.

Instead, mainstream economists keep trying to get away with tiny tweaks in their fundamentally flawed way of looking at the world.

Consider, for example, the concept that still underpins most mathematical models of the economy:

that firms and individuals have “rational expectations,”

Mark Buchanan, Bloomberg Dec 16, 2013

Consider, for example, the concept that still underpins most mathematical models of the economy: that firms and individuals have “rational expectations,” meaning that they all base their decisions on the same unbiased, probabilistic view of the future.

A person deciding to buy a chocolate bar, for example, will consider such factors as the future price of cocoa and the interest that could be earned by saving the money, and he or she will use the same forecasts as everyone else on the planet.

Given the vast heterogeneity of human psychology and behavior, it’s a preposterous assumption - one that rendered the models useless during the last financial crisis.

Full text

Economic theory discredited

Rational Expectations

Robert Lucas’s work led to what has sometimes been called the “policy ineffectiveness proposition.”

Thomas J. Sargent, econlib dot org

Fotnot:

Robert Lucas Nobel Laureate 1995

Full text

His ex-wife, Rita Lucas, upon their divorce in 1988, had a clause placed in their divorce settlement that she would receive half of any Nobel Prize won by Lucas in the next seven years.

When Lucas did win the Nobel Prize in 1995 (falling just within the time limit), she was awarded half of the prize money

Wikipedia

- There is no such thing as rational expectations.

There is wishful thinking, or panic.

Rolf Englund, many years ago (probably in 1997)

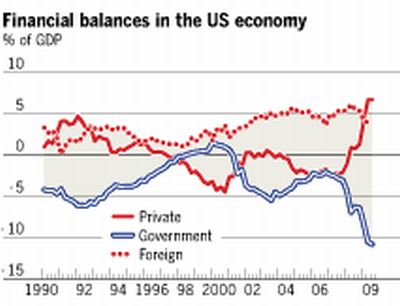

Jumps in fiscal deficits are the mirror image of retrenchment by battered private sectors.

In the US, the financial balance of the private sector (the gap between income and expenditure) shifted from minus 2.1 per cent of GDP in the fourth quarter of 2007 to plus 6.7 per cent in the third quarter of 2009, a swing of 8.8 per cent of GDP.

Martin Wolf February 16 2010

Jesper Katz och Johnny Munkhammar:

Ge inget EU-stöd till Grekland

Vanligtvis leder sänkta statliga utgifter till minskad tillväxt tillfälligt,

men om det leder till sänkta räntor

kan en budgetsanering ge högre tillväxt än vad som annars vore fallet.

Europaportalen 2010-02-04

What would happen if governments also slashed their spending? In an economy without monetary or exchange-rate offsets to austerity, any reduction in spending is likely to lead to at least an equivalent short-run reduction in output (a “multiplier” of one).

An attempt to cut a fiscal deficit by 10 per cent of GDP, via cuts in spending, would require an actual reduction of 15 per cent of GDP, once one allows for falling fiscal revenue. GDP would also shrink 15 per cent.

As Desmond Lachman of the American Enterprise Institute pointed out in FT.com’s Economists’ Forum, the decline could be even larger.

Martin Wolf, February 9 2010

The only way for eurozone countries to slash huge fiscal deficits, without their economies collapsing, is to engineer another private-sector credit bubble or a huge expansion in net exports.

The former is undesirable. The latter requires improved competitiveness and buoyant external demand.

At present, none of this is available.

It is difficult to regain competitiveness when the euro is strong, partly because Germany is so competitive,

and eurozone inflation also so low.

Full text

Multiplikatorn

Top of page

Dagens globala finanskris har utlöst en kris för ämnet nationalekonomi.

Sökandet efter bättre ekonomisk analys pågår för fullt.

Lars Jonung kolumn DN 29/4 2010

Nu var det Chicagoskolan som attackerades på konferensen, mer specifikt: antagandena i dess modeller över det finansiella systemet.

Dessa har den olyckliga egenskapen att utesluta just de företeelser som kännetecknar finansiella kriser.

Full text

Lars Jonung

Klicka här

The disappointing economic data on US activity in recent months has brought a key policy debate back into focus.

The Keynesian side of this debate has been well served, with frequent outstanding contributions from Paul Krugman, Brad DeLong and others.

But I have had more trouble finding serious economic contributions from the classical school, even though they seem to be gaining ground in political and policy circles on both sides of the Atlantic.

For that reason, I was particularly interested in the recent lecture on the US recession given by the University of Chicago’s Robert Lucas.

Lucas is universally recognised as an intellectual giant, and his lecture gives a neat synopsis of what the classical school currently thinks, straight from the horse’s mouth.

Gavin Davies FT blog 31 may 2011

In 2008, as the global financial crisis unfolded, the reputation of economics as a discipline and economists as useful policy practitioners seemed to be irredeemably sunk. Queen Elizabeth captured the mood when she asked pointedly why no one (in particular economists) had seen the crisis coming.

There was no doubt that, notwithstanding the few Cassandras who correctly prophesied gloom and doom, the profession had failed colossally.

The totemic symbols of this failure were, of course, the two most important policymakers, Alan Greenspan and his successor as chairman of the US Federal Reserve, Ben Bernanke. They, among many others, helped create a belief system that elevated markets beyond criticism.

Arvind Subramanian, FT December 27 2009

In a guest article,

Robert Lucas rebuts criticisms that

the financial crisis represents a failure of economics

The Economist print, Aug 6th 2009

One thing we are not going to have, now or ever, is a set of models that forecasts sudden falls in the value of financial assets, like the declines that followed the failure of Lehman Brothers in September. This is nothing new.

It has been known for more than 40 years and is one of the main implications of Eugene Fama’s “efficient-market hypothesis” (EMH), which states that the price of a financial asset reflects all relevant, generally available information.

If an economist had a formula that could reliably forecast crises a week in advance, say, then that formula would become part of generally available information and prices would fall a week earlier.

(The term “efficient” as used here means that individuals use information in their own private interest.

It has nothing to do with socially desirable pricing; people often confuse the two.)

Both Mr Bernanke and Mr Mishkin are in the mainstream of what one critic cited in The Economist’s briefing calls a “Dark Age of macroeconomics”.

They are exponents and creative builders of dynamic models and have taught these “spectacularly useless” tools, directly and through textbooks that have become industry standards, to generations of students.

Full text

The Keynes comeback

A trio of new books celebrate the man and declare victory for his ideas

“This present crisis is a crisis of systemic ignorance not asymmetric information.”

The Economist print Oct 1st 2009

Keynes: The Return of the Master

“Why did no one see the crisis coming?”, Queen Elizabeth asked

A seminar at the British Academy tried to answer and the FT has taken up the discussion.

Robert Skidelsky, FT, August 5 2009

Why it is still too early to start withdrawing stimulus

Two groups of thinkers reject this viewpoint.

One argues that the economy is always in equilibrium.

Both the guilty and the innocent must suffer

Martin Wolf, FT September 8 2009

Ben Bernanke, recently nominated by Barack Obama to a second term as chairman of the Federal Reserve,

made the point at this year’s Jackson Hole monetary symposium:

“Without these speedy and forceful actions, last October’s panic would likely have continued to intensify,

more major financial firms would have failed and the entire global financial system would have been at serious risk.

[W]hat we know about the effects of financial crises suggests that the resulting global downturn could have been

extraordinarily deep and protracted.”

Two groups of thinkers reject this viewpoint.

One argues that the economy is always in equilibrium.

If unemployment has exploded upwards it can only be because, after Lehman imploded, workers chose to take a holiday.

An alternative view is that depressions are the natural consequence of excess.

Both the guilty and the innocent must suffer, as past errors are purged.

Rightly, policymakers rejected such views.

Economies are not always in equilibrium and, while a correction of excesses in asset prices, financial markets and consumption had become inescapable,

a cumulative downward spiral was neither inevitable nor tolerable.

Full text

Déjà vu: echoes of pre-crisis world mount

But missing credit bubble indicates next crash is not imminent

John Plender, Financial Times June 10, 2014

An occupational hazard of observing markets is a recurring sense of déjà vu.

Even so, 2014 is proving a vintage year for echoes of the pre-crisis world.

First, we have the return of the Great Moderation, that period of eerie stability before 2007 which economists and central bankers hailed as the harbinger of a new era of non-inflationary growth.

Today market volatility has again collapsed across all asset classes.

Ten-year US Treasuries, the global bond market benchmark, have been trading in a relatively narrow range all year.

Full text

John Plender

The Great Moderation, Version 2.0

“Great Moderation” – was invented to describe the stable period from 1984-2008,

when the variability of real GDP growth and inflation both fell markedly

Gavyn Davies, FT blog April 13, 2014

Of course, none of this precludes the possibility that the current expansion and bull market will end the same way as occurred in 2008,

with a “Minsky moment” in a financial system that has reached too far into risk assets.

There are some worrying signs of this in the recent froth in the IPO market for internet and biotech stocks, which now seems set to correct quite sharply.

But overall global equity market valuations do not seem to be in bubble territory yet.

Full text

Minsky’s Financial Instability Hypothesis

The regulatory failures in the buildup to the recent crisis were induced by the same complacency that infected the financial system and economy

in the latter stages of the period economists call “the great moderation,” beginning in the early 1980s and spanning roughly two decades of relatively steady growth and low inflation,

interrupted only by recessions that were short and mild.

Martin Hellwig ”The Bankers' New Clothes: What's Wrong with Banking and What to Do About It”

Roger E. Alcaly, The York Review of Books, 5 June 2014

The world still does not fully understand how financial markets work,

according to investor George Soros speaking at the World Economic Forum in Davos

He said there was a risk of a credit bubble forming, which was "the big, unresolved issue"

BBC 26 January 2013

In a wide-ranging discussion, Mr Soros said: "The established theory has collapsed but we haven't actually got a proper understanding of how financial markets operate.

"We have introduced synthetic instruments, invented derivatives where we don't fully understand the effect they have."

Full text

Economic theory discredited

Next Bubble Is Forming: U.S. Government Bonds

Houseprices - Asset price bubbles and Central Bank Policy Alan Greenspan

Hyman Minsky

The Great Moderation, rationellt beteende, inflationsmål

Finanskrisen var ett misslyckande för ekonomprofessionen.

Vi borde ha varnat mer för de finansiella riskerna

Lars Calmfors, kolumn DN 21 augusti 2012

Efter 1970- och 1980-talens stora störningar i världsekonomin hade en ny konsensus vuxit fram. Enligt denna borde penningpolitiken vägledas av tydliga inflationsmål och ha huvudansvaret för att stabilisera konjunkturen.

Denna stabiliseringspolitiska uppläggning fungerade till en början väl. Den ekonomiska utvecklingen ansågs allmänt före finanskrisen präglas av the Great Moderation, alltså av att konjunktursvängningarna blivit mycket mindre.

Grundfelet var att man inte insåg att det gick att under lång tid uppnå låg inflation och stabilisera konjunkturen samtidigt som en alltför snabb kreditexpansion kunde göda ohållbara ökningar av fastighetspriserna.

En orsak till felbedömningarna var alltför stor tilltro till teoretiskt eleganta analysmodeller. Alltför liten vikt lades vid empiriska generaliseringar av tidigare ekonomisk-historiska erfarenheter av finansiella kriser som stod i strid med antaganden om rationellt beteende.

Större kunskaper i doktrinhistoria hade förmodligen också hjälpt ekonomkåren till mer skepsis gentemot för tillfället dominerande synsätt.

Full text

När det gäller eurokrisen förtjänar emellertid nationalekonomerna enligt min mening ett gott betyg

Lars Calmfors, kolumn DN 21 augusti 2012

"Nu har jag försökt göra mig till ovän med så många grupper av ekonomer som möjligt.

Jag tror att jag har fått med de flesta: andra makroekonomer, finansiella ekonomer, ekonomhistoriker, centralbanksekonomer, ekonometriker plus alla andra som inte vill prata om samma saker som jag själv på kafferasterna.

Jag har även varit lite kritisk mot mig själv."

Kollegorna i panelen tittade på honom. Kollegorna i publiken tittade på honom.

Vad var det Lars Calmfors, den svenska nationalekonomins enda fixstjärna, just hade sagt?

Nationalekonomiska föreningen i januari 2010

Economic theory discredited

Lars Calmfors

San Francisco Fed President John Williams on "price stability"

What objective should we seek for the rate of increase of average prices?

Should we strive for no change at all, that is, zero inflation?

Via CalculatedRisk, 13 February 2012

At first blush, that seems sensible. But, there are a number of reasons why aiming for zero inflation would be too low and inconsistent with our maximum employment mandate. Here I’ll mention two.

First, a small amount of inflation can help grease the wheels of the labor market. There is considerable evidence that nominal wages don’t easily fall even when demand is weak, something economists call downward wage rigidity.

Full text

Olivier Blanchard, the IMF’s chief economist called for several bold innovations.

Central banks should raise their inflation targets—perhaps to 4% from the standard 2% or so.

The ideas that sustained the pre-crisis policy framework have been thoroughly discredited

Among these ideas, the central and most clearly falsified are the supposed “Great Moderation” in economic volatility and the “Efficient Financial Markets Hypothesis”.

John Quiggin, FT November 29 2010

For most countries, austerity policies are likely to prove unsustainable, either because they do not deliver a sufficient improvement in the budget balance, or because they are a politically and socially costly diversion from the task of achieving long term fiscal sustainability.

John Quiggin is an ARC Federation Fellow in Economics and Political Science at the University of Queensland.

He is the author of Zombie Economics: How Dead Ideas Still Walk Among Us

Full text

Top of page

During the “Great Moderation” of the late 1990s and early 21st century,

it was not only Gordon Brown in the UK who announced the end of “boom and bust”.

Samuel Brittan, FT December 10 2009

Did inflation targeting fail?

Central banks have mostly escaped blame for the crisis.

Martin Wolf, Financial Times, May 5 2009

Just over five years ago, Ben Bernanke, now chairman of the Federal Reserve,

gave a speech on the “Great Moderation”

– the declining volatility of inflation and output over the previous two decades.

In this he emphasised the beneficial role of improved monetary policy.

Central bankers felt proud of themselves.

Pride went before a fall. Today, they are struggling with the deepest recession since the 1930s, a banking system on government life-support and the danger of deflation.

How can it have gone so wrong?

Read more here

Teorin om att marknaden "har rätt" kan tyckas ha falsifierats av krisen.

Det finns alltid bedömare som i vaga ordalag hävdar att utvecklingen kommer att gå åt skogen. Svårigheten ligger i att kunna skilja fantasterna från dem som har hittat fundamentala orosfaktorer av sådan karaktär att de borde tas på allvar.

En sådan person är den iransk-israeliske ekonomen Nouriel Roubini

Vad som skulle behövas är en utvärdering av varför Roubinis varningar inte togs på allvar. Hur såg de första varningarna i september 2006 ut?

Danne Nordling 16/3 2010

Tänkbart är naturligtvis att ekonomerna ansåg att marknadsekonomins självreglerande förmåga var så grundläggande att några åtgärder mot "bubblor" och andra svängningar inte var behövliga.

Själv vill jag peka på behovet av en genomgång av den stabiliseringspolitiska teorin som redan när krisen bröt ut efter Lehmans konkurs i september 2008 inte fanns samlad på ett auktoritativt sätt.

Full text

Stabiliseringspolitik

Nouriel Roubini

They (G-20) may hope that retrenchment now will spur on private spending.

But what is their plan if it turns out that it does not?

Martin Wolf, July 6 2010

Economics may be dismal, but it is not a science

The failures of economics in the recent crisis are most evident in two areas:

the inadequacies of the efficient market hypothesis, the bedrock of modern financial economics,

and the irrelevance of recent macroeconomic theory.

John Kay, FT April 13 2010

The macroeconomics taught in advanced economics today is largely based on analysis labelled dynamic stochastic general equilibrium.

The unappealing title gives the game away: the theorists are mostly talking to themselves.

Their theories proved virtually useless in anticipating the crisis, analysing its development and recommending measures to deal with it.

Both the efficient market hypothesis and DSGE are associated with the idea of rational expectations – which might be described as the idea that households and companies make economic decisions as if they had available to them all the information about the world that might be available. I

If you wonder why such an implausible notion has won wide acceptance, part of the explanation lies in its conservative implications. Under rational expectations, not only do firms and households know already as much as policymakers, but they also anticipate what the government itself will do, so the best thing government can do is to remain predictable. Most economic policy is futile.

Full text

Top of page

The ideas that sustained the pre-crisis policy framework have been thoroughly discredited

Among these ideas, the central and most clearly falsified are the supposed “Great Moderation” in economic volatility and the “Efficient Financial Markets Hypothesis”.

John Quiggin, FT November 29 2010

How Did Economists Get It So Wrong?

Paul Krugman, New York Times Magazine, 2/9 2009

It’s hard to believe now, but not long ago economists were congratulating themselves over the success of their field.

Those successes — or so they believed — were both theoretical and practical, leading to a golden era for the profession.

On the theoretical side, they thought that they had resolved their internal disputes.

Thus, in a 2008 paper titled “The State of Macro” (that is, macroeconomics, the study of big-picture issues like recessions),

Olivier Blanchard of M.I.T., now the chief economist at the International Monetary Fund, declared that “the state of macro is good.” The battles of yesteryear, he said, were over, and there had been a “broad convergence of vision.”

And in the real world, economists believed they had things under control:

the “central problem of depression-prevention has been solved,” declared Robert Lucas of the University of Chicago

in his 2003 presidential address to the American Economic Association.

In 2004, Ben Bernanke, a former Princeton professor who is now the chairman of the Federal Reserve Board, celebrated

the Great Moderation in economic performance over the previous two decades, which he attributed in part to improved economic policy making.

Last year, everything came apart.

Few economists saw our current crisis coming, but this predictive failure was the least of the field’s problems.

More important was the profession’s blindness to the very possibility of catastrophic failures in a market economy.

Full text

Krugman beskriver världsdepressionen i början av 30-talet som en efterfrågekris:

”Det som satte stopp för trettiotalsdepressionen i USA var ett massivt underskottfinansierat program för offentliga arbeten som kallas andra världskriget”.

Carl Johan Gardell, Understreckare SvD 13 augusti 2009

The efficient-markets hypothesis

Of all the economic bubbles that have been pricked, few have burst more spectacularly than the reputation of economics itself.

Paul Krugman argued that much of the past 30 years of macroeconomics was

“spectacularly useless at best, and positively harmful at worst.”

The Economist print July 16th 2009

Top of page

Die meisten Makroökonomen und Finanzmarktspezialisten waren zum Beispiel der festen Überzeugung, dass Finanzmärkte effizient sind, dass es keine Blasen gibt und dass wir die Marktpreise respektieren müssen als die kollektive Weisheit der Menschen, die jedermanns individuelles Wissen übersteigt. Es wäre lächerlich, den Markt in Frage zu stellen, dachten sie.

Das war einer der größten Fehler in der Geschichte des ökonomischen Denkens.

In an interview in Frankfurter Allgemeine, Robert Shiller forecasts that the next five years will be disappointing.

While the first wave of this crisis is over, he points out, there may be another wave coming with some delay, just as it happened during the 1929-1941 Great Depression.

Eurointelligence 31/8 2009

For 30 years or so Keynesianism ruled the roost of economics – and economic policy.

Harvard was queen, Chicago was nowhere.

But Chicago was merely licking its wounds. In the 1960s it counter-attacked.

The new assault was led by Milton Friedman and followed up by a galaxy of clever young disciples.

What they did was to reinstate classical theory. Their “proofs” that markets are instantaneously, or nearly instantaneously, self-adjusting to full employment were all the more impressive because now expressed in mathematics.

Adaptive Expectations, Rational Expectations, Real Business Cycle Theory, Efficient Financial Market Theory – they all poured off the Chicago assembly line, their inventors awarded Nobel Prizes.

No policymaker understood the maths, but they got the message: markets were good, governments bad. The Keynesians were in retreat. Following Ronald Reagan and Margaret Thatcher, Keynesian full employment policies were abandoned and markets deregulated.

Then along came the almost Great Depression of today and the battle is once more joined.

Robert Skidelsky, Financial Times June 9 2009

Utdrag ur Olle Wästberg: Det tomma rummet, Wahlström

och Widstrand, 1996

Kapitel 8: ”Keynes ligger död i kontrollrummet”

I recently had the pleasure of reading Justin Fox’s new book The Myth of the Rational Market.

It offers an engaging history of the research that has come to be called the “efficient market hypothesis”.

It is similar in style to the classic by the late Peter Bernstein, Against the Gods.

Richard Thaler, FT, August 4 2009

The writer is a professor of economics and behavioural science at the University of Chicago Booth School of Business and the co-author of Nudge

However, as early as 1984 Robert Shiller, the economist, correctly and boldly called this “one of the most remarkable errors in the history of economic thought”.

The reason this is an error is that prices can be unpredictable and still wrong;

the difference between the random walk fluctuations of correct asset prices and the unpredictable wanderings of a drunk are not discernable.

Full text

The Myth of the Rational Market

Against the Gods

Top of page

The efficient-markets hypothesis has underpinned many of the financial industry’s models for years.

After the crash, what remains of it?

In 1978 Michael Jensen, an American economist, boldly declared that “there is no other proposition in economics which has more solid empirical evidence supporting it than the efficient-markets hypothesis”

The Economist print July 16th 2009

The efficient-markets hypothesis

Of all the economic bubbles that have been pricked, few have burst more spectacularly than the reputation of economics itself.

Paul Krugman argued that much of the past 30 years of macroeconomics was

“spectacularly useless at best, and positively harmful at worst.”

The Economist print July 16th 2009

Barry Eichengreen, a prominent American economic historian, says the crisis has “cast into doubt much of what we thought we knew about economics.”

These important caveats, however, should not obscure the fact that two central parts of the discipline — macroeconomics and financial economics — are now, rightly, being severely re-examined (see article, article).

There are three main critiques: that macro and financial economists helped cause the crisis, that they failed to spot it, and that they have no idea how to fix it.

But economists were hardly naive believers in market efficiency. Financial academics have spent much of the past 30 years poking holes in the “efficient market hypothesis”. A recent ranking of academic economists was topped by Joseph Stiglitz and Andrei Shleifer, two prominent hole-pokers.

A newly prominent field, behavioural economics, concentrates on the consequences of irrational actions.

No economic theory suggests you should value mortgage derivatives on the basis that house prices would always rise. Finance professors are not to blame for this, but they might have shouted more loudly that their insights were being misused. Instead many cheered the party along (often from within banks).

Put that together with the complacency of the macroeconomists and there were too few voices shouting stop.

The charge that most economists failed to see the crisis coming also has merit. To be sure, some warned of trouble. The likes of Robert Shiller of Yale, Nouriel Roubini of New York University and the team at the Bank for International Settlements are now famous for their prescience.

Macroeconomists also had a blindspot: their standard models assumed that capital markets work perfectly. Their framework reflected an uneasy truce between the intellectual heirs of Keynes, who accept that economies can fall short of their potential, and purists who hold that supply must always equal demand.

Full text

Stabiliseringspolitik

Skuldfrågan/ Who is responsible?

Top of page

The chief intellectual casualty of the current crisis has been the “efficient markets” school

– the theory, associated with such erstwhile laisser faire gurus as Alan Greenspan, that market participants are governed by rational expectations and markets are self-correcting.

Lawrence H. Summers, FT July 10 2009

Att göra något i närheten av det Svenskt Näringsliv talar om är ju helt ansvarslöst.

Det skulle leda till att människor inte kände något förtroende för de offentliga finanserna.

Det privata sparandet skulle öka och i slutändan skulle den expansiva effekten utebli

Anders Borg i Fokus 28/11 2008, reporter Anders Jonson

Budgetåtstramningar i dåliga tider kan få positiva effekter

Konsumenterna låter sig inte manipuleras. Det är för kunskapen om dessa mekanismer den amerikanske ekonomen Robert Lucas fick nobelpriset i ekonomi 1995.

Teorin talar om konsumenternas "rationella förväntningar".

Det är också därför, tvärtemot alla tidigare teorier, budgetåtstramningar i dåliga tider kan få positiva effekter.

Ur Olle Wästberg: Det tomma rummet, Wahlström och Widstrand, 1996, Kapitel 8: ”Keynes ligger död i kontrollrummet”

The Myth Of the Rational Market

Stocks fell off what Irving Fisher had called a "permanently high plateau" in October 1929

and didn't return until that level until 1954.

Justin Fox, Time, June 22, 2009

Friedman had played a key part in developing the "efficient markets hypothesis," which, together with its younger sibling the "rational expectation hypothesis"—see below—provided the intellectual underpinning for more than two decades of financial deregulation. Briefly put, the efficient markets hypothesis states that prices of stocks, bonds, and other speculative assets necessarily reflect everything that is known about economic fundamentals, such as inflation, exports, and corporate profitability.

Friedman actually formulated the efficient markets hypothesis in an analysis of currencies. It was Fama, one of his students, who applied it to the stock market and pointed out an interesting corollary: if stock prices already reflect everything that is known and knowable, then investors can't hope to outperform the market using trading strategies based on publicly available information.

Lucas, the third member of the Chicago triumvirate, was arguably more influential even than Friedman. In a series of ingenious papers published in the 1960s and 1970s, he and several colleagues extended the hyperrational methodology underpinning the efficient markets hypothesis to other parts of the economy, such as the job market, the output decisions of firms, and the formulation of economic policy. By the time they were done, Lucas et al. had invented a new way of doing macroeconomics, known as the rational expectations approach, which enshrined in higher mathematics the stabilizing properties of unfettered markets.

Where, though, do these economic expectations come from? According to Lucas, they reflect a predefined, externally grounded, and commonly agreed upon reality.

In his models, the economy's equations of motion are well defined and known to all—from Ph.D. economists at the University of Chicago to nurses and cab drivers.

Utilizing this common knowledge, people form "rational expectations" of things like inflation and interest rates. They don't always get things right—a certain amount of randomness is allowed for—but they are precluded from making systematic errors. If in one period the economy gets out of sync, in the next period it jumps back to the "equilibrium" defined by the model.

Not content to create new models, Lucas also disparaged older theories that viewed financial capitalism more skeptically. Keynesianism wasn't merely wrong, he declared at one point: it was no longer intellectually respectable.

Outside the idealized world of Lucas's theory, knowledge is imperfect, people stick to wrongheaded ideas, and there is no agreed version of how the economy works.

Source: John Cassidy in The New York Review of Books, October 23, 2008, in an article about

The New Paradigm for Financial Markets: The Credit Crisis of 2008 and What It Means by George Soros

Full text

Cherished myths fall victim to economic reality

"Financial markets are efficient"

"Individuals are supremely well-informed creatures" /Rational expectations

Paul De Grauwe, Financial Times July 22 2008

The credit crisis has destroyed the idea that unregulated financial markets always efficiently channel savings to the most promising investment projects. Millions of US citizens took on unsustainable debts, pushed around by bankers and other “debt merchants” who made a quick buck by disregarding risks. While this happened, the US monetary authorities marvelled at the creativity of financial capitalism. When the bust came, a large number of Americans who had been promised a new life in their beautiful homes were told to move out. This boom and bust cycle cannot have been an example of efficient channelling of savings into the most promising investment projects.

There is a second idea that is likely to become the victim of the financial crisis. This is the idea found in macroeconomic models, that individuals are supremely well-informed creatures. In these models that are now being used in central banks and universities, individuals understand the most complex intricacies of the world in which they live and they have no disagreement about this. All these individuals understand the same “truth”.

If we have learnt one thing from the credit crisis it is that individuals did not understand the “truth” and, it must be admitted, neither did economists.

Full text

New Era

One of the surprising developments in macroeconomics is the systematic incorporation of

the paradigm of the utility maximizing forward looking and fully informed agent

Paul De Grauwe. Eurointelligence 13.06.2008

These developments are surprising for several reasons.

First, while macroeconomic theory enthusiastically embraced the view that agents fully understand the structure of the world in which they operate, other sciences like psychology and neurology increasingly uncovered the cognitive limitations of individuals.

A second source of surprise of the development of macroeconomic modeling in general and the DSGE-models in particular is that other branches of economics, like game theory and experimental economics have increasingly recognized the need to incorporate the limitations agents face in understanding the world. This has led to models that depart from the rational expectations paradigm.

The problem with this business cycle theory is that it is not a theory of the business cycle.

In DSGE-models cyclical movements are always triggered by outside shocks. They are not generated within the system. In fact they cannot be. The super-rational and fully informed creatures that populate the DSGE-models would arbitrage away any systematic cyclical movement in prices and output.

Thus, our most popular macro economic model that is now used by central bankers has no theory of why after a boom comes a bust.

Booms and busts always find their origin outside the macroeconomic landscape.

Full text

Comment by Rolf Englund:

Hear! Hear!

The Nobel Price to Robert Lucas was a big mistake.

“inflationary expectations”

William White, until recently economic adviser to the Bank for International Settlements

has resisted heroically the temptation to say: “I told you so.”

Samuel Brittan, Financial Times, August 14 2008

Robert Lucas - 1995 Nobel Laureate in Economics

for having developed and applied the hypothesis of rational expectations,

and thereby having transformed macroeconomic analysis and deepened our understanding of economic policy.

Budgetåtstramningar i dåliga tider kan få positiva effekter

Utdrag ur Olle Wästberg: Det tomma rummet, Wahlström och Widstrand, 1996

Kapitel 8: ”Keynes ligger död i kontrollrummet”

Viktigast är att konsumenterna inte låter sig manipuleras. Det är för kunskapen om dessa mekanismer den amerikanske ekonomen Robert Lucas fick nobelpriset i ekonomi 1995. Teorin talar om konsumenternas "rationella förväntningar".

Det är också därför, tvärtemot alla tidigare teorier, budgetåtstramningar i dåliga tider kan få positiva effekter.

Mer om 1992 och kronkursförsvaret

Mer om bubblor på finansmarknaderna