Skuldfrĺgan/Who is responsible?

News Home

Home - Index -

News - Krisen 1992 - EMU - Economics - Cataclysm -

Wall Street Bubbles

US Dollar - Subprime - Houseprices

The Experiment

Monetary policy works by creating the environment for a renewed borrowing and lending cycle.

This cycle would require that the debt to GDP ratio, which is already at a record level, grow even higher.

Would such an outcome really be that desirable?

Hoisington Investment Management Company, Quarterly Review and Outlook Q4 2008

Hoisington Investment Management Company (www.hoisingtonmgt.com) is a registered investment advisor specializing in fixed income portfolios for large institutional clients.

Located in Austin, Texas, the firm has over $4-billion under management

The late Nobel Laureate, Milton Friedman, noted in his 1963 book, Monetary History of the United States (coauthored with Anna Swartz), that the money stock decreased by a massive 31% in the Great Depression. The turnover of that money, called velocity, fell 21%. Nominal GDP equals money multiplied by velocity. Consequently, from 1929 to 1933 the breakdown of both measures resulted in a contraction in nominal GDP of approximately 50%. However, Friedman postulated that if the Fed had not let money shrink, velocity would have been steady and the Great Depression would have been averted, i.e., nominal GDP would not have collapsed.

Our current Fed Chairman, Ben Bernanke, is an expert on the Great Depression, and he has, in fact, adopted Friedman's strategy to greatly expand the money supply.

Whether this prescription for economic stability will work in a period of over indebtedness, such as now exists in the U.S., is most uncertain.

Indeed, this could be called the "great experiment" since this economic theory has yet to be thoroughly tested in the real world.

Irving Fisher developed that concept by examining the 1929-33 depressionary period, as well as the depressions of 1837 and 1873, as examples of when excessive debt and subsequent price declines controlled "all or nearly all" other economic variables.

This theory of excessive debt and its pernicious and unrelenting deflationary impulse to the economy has been best chronicled by other notable economists: Charles P. Kindleberger (1910-2003), Hyman Minsky (1919-1996), Nikolai Kondratieff (1892-1938) and Joseph A. Schumpeter (1883-1950).

Fisher contends that once extreme over indebtedness occurs, fiscal and monetary policy become impotent in spurring economic growth because money velocity will decline -- something that is currently happening. Individuals and businesses struggle to repay debt with harder dollars, and saving begins to rise as caution prevails.

Our judgment is that the power of monetary policy revolves around the ability to initiate a new borrowing and lending cycle. This can only happen if lenders are willing to lend and borrowers are wanting and able to borrow. Presently, neither are so inclined (Chart 2). If price declines in assets continue, then Shakespeare's admonition of "neither a borrower nor a lender be" will become the economic mantra, meaning that a period of very low nominal growth will likely extend for a decade.

Numerous studies had shown that consumers have a very limited tendency to spend transitory income, and that prior efforts to stimulate the economy through tax rebates had failed.

Nevertheless, the political process barreled through with a program with no reasonable expectation that it would work. Now the economy is even deeper in recession and the country has an addition al $177 billion in debt on which the taxpayers will pay interest in perpetuity.

About 17% of the rebates were spent, a tad less than during the rebate program of 2001.

The minimal spending response was exactly in line with the consumption functions under Friedman's permanent income hypothesis, as well as the equivalent Modigliani's life cycle hypothesis.

These pioneering works demonstrated conclusively that consumers have a far greater tendency to spend permanent rather than transitory income.

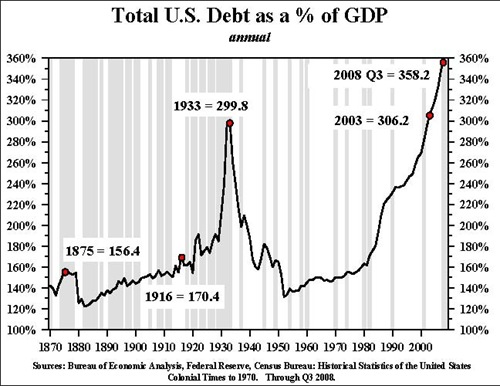

The debt level of the U.S. has reached unprecedented proportions (Chart 1)

Monetary policy works by creating the environment for a renewed borrowing and lending cycle.

This cycle would require that the debt to GDP ratio, which is already at a record level, grow even higher.

Would such an outcome really be that desirable when the controlling problem of the U.S. economy is too much improperly financed debt? If the Fed were able to engender an increase in the debt to GDP ratio, this might merely serve to postpone the reckoning of the current debt levels while laying the foundation for an even more vicious unwinding down the road.